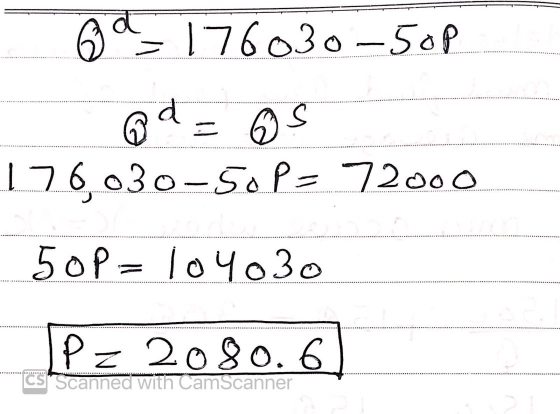

There are 7,200 identical firms in the widget industry each of which has a fixed cost...

There are 7,200 identical firms in the widget industry each of

which has a fixed cost that is avoidable in the long run, F=1,500,

and their technology is given by q=K^(1/5)L^(3/10). Initially the

input prices are w=9 and v=6. The market demand they face is

QD(P)=176,030−50 P. Find the long run equilibrium.

Homework Answers

![Dote 0 = * (2140 © = (_)** (13% [= 02] K= 02 C = Wht rk C = 9 @²+682 C= 15 9² Total cost = Fixed cast & Vanable cast T.C 3.15](http://img.homeworklib.com/questions/2ebe92b0-d5f8-11ea-bfb0-97fd64fae1f1.png?x-oss-process=image/resize,w_560)

Add Answer to:

There are 7,200 identical firms in the widget industry each of

which has a fixed cost...

2. A competitive industry has 12 identical firms, each one has a total variable cost function...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

21. The widget industry is a constant-cost industry, so that all firms are identical. The following...

21. The widget industry is a constant-cost industry, so that all firms are identical. The following chart shows the industry-wide demand curve and the marginal cost curve of a typical firm: Industry-Wide Demand Price ($) Quantity Firm's Marginal Cost Curve Quantity Marginal Cost ($) 500 oooooow 400 300 200 100 + LOCO cocoon The industry is in long-run equilibrium and there are 100 fims. a. What are the fixed costs at each firm? b. What is the price of a...

21. The widget industry is a constant-cost industry, so that all firms are identical. The following chart shows the industry-wide demand curve and the marginal cost curve of a typical firm: Industry-Wide Demand Price ($) Quantity Firm's Marginal Cost Curve Quantity Marginal Cost ($) 500 oooooow 400 300 200 100 + LOCO cocoon The industry is in long-run equilibrium and there are 100 fims. a. What are the fixed costs at each firm? b. What is the price of a...

For a constant cost industry in which all firms the same cost functions, their long-run average...

For a constant cost industry in which all firms the same cost functions, their long-run average cost is minimized at $10 per unit output and 20 units (i.e. q = 20). Market demand is given by QD=DP=1,500-50P. Find the long-run market supply function Find the long-run equilibrium price (P*), market quantity (Q*), firm output (q*), number of firms (n), and each firm’s profit. The short-run total cost function associated with each firm’s long-run costs is SCq=0.5q2-10q+200. Calculate the short-run average...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i.Calculate the equilibrium price and quantity. ii.Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose the demand for cotton T-shirts is...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q)...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

Need as much details as possible. Microeconomics. A competitive industry consists of identical firms. Each firm...

Need as much details as possible. Microeconomics. A competitive industry consists of identical firms. Each firm has the long run total cost function TC(q)=18+½q2. If the market demand is Q(p)= 420 - p, what is the equilibrium quantity produced by each firm in the long run? a. 12 b. 18 c. 9 d. 6

please answer ASAP please help A perfectly competitive industry is composed of 100 identical firms with...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

21. The widget industry is a constant-cost industry, so that all firms are identical. The following chart shows the industry-wide demand curve and the marginal cost curve of a typical firm: Industry-Wide Demand Price ($) Quantity Firm's Marginal Cost Curve Quantity Marginal Cost ($) 500 oooooow 400 300 200 100 + LOCO cocoon The industry is in long-run equilibrium and there are 100 fims. a. What are the fixed costs at each firm? b. What is the price of a...

21. The widget industry is a constant-cost industry, so that all firms are identical. The following chart shows the industry-wide demand curve and the marginal cost curve of a typical firm: Industry-Wide Demand Price ($) Quantity Firm's Marginal Cost Curve Quantity Marginal Cost ($) 500 oooooow 400 300 200 100 + LOCO cocoon The industry is in long-run equilibrium and there are 100 fims. a. What are the fixed costs at each firm? b. What is the price of a...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

Most questions answered within 3 hours.

-

•Let’s say someone claims the average population size is

600 feet squared and the housing authority...

asked 1 minute ago -

Cynaide is a deadly poison that blocks the last step in the

electron transport chain of...

asked 5 minutes ago -

Your friend tells you that there is a vending machine on campus

that dispenses M&M packs...

asked 20 minutes ago -

What advantages are there to using piperidine rather than

hydroxide as a base?

asked 19 minutes ago -

7. The life of a Freeze Breeze electric fan is normally

distributed with a mean 4...

asked 22 minutes ago -

1. A 751 mL NaCl solution is diluted to a volume of 1.06 L and a...

asked 27 minutes ago -

8

A $20,000 face value STRIPS is currently quoted at 38.642 and

has 8 years to...

asked 27 minutes ago -

The current exchange rate between the Japanese yen and

the US dollar is 120 yen per...

asked 29 minutes ago -

Marla’s Massages and More bought a special massage table two

years ago for $9,300. At the...

asked 36 minutes ago -

Suppose you require a peak output voltage of 15.0 V and have

available an AC source...

asked 36 minutes ago -

We

conduct A study to estimate the mean age of the population of women

at the...

asked 48 minutes ago -

.13 : Assume that we make an enhancement to a computer that

improves some mode of...

asked 49 minutes ago