Creaston Limited’s most recent monthly contribution format income statement is given below:

| CREASTON LIMITED Income Statement For the Month Ended May 31 |

||

| Sales | $900,000 | 100.0% |

| Variable expenses | 408,000 | 45.3 |

| Contribution margin | 492,000 | 54.7 |

| Fixed expenses | 465,000 | 51.7 |

| Operating income | $ 27,000 | 3.0% |

-

Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following:

-

The company is divided into two sales territories—Central and Eastern. Central Territory recorded $400,000 in sales and $208,000 in variable expenses during May. The remaining sales and variable expenses were recorded in Eastern Territory. Fixed expenses of $160,000 and $130,000 are traceable to Central and Eastern Territories, respectively. The rest of the fixed expenses are common to the two territories.

-

The company is the exclusive distributor for two products—Kiks and Dows. Sales of Kiks and Dows totalled $100,000 and $300,000, respectively, in Central Territory during May. Variable expenses are 25% of the selling price for Kiks and 61% for Dows. Cost records show that $60,000 of Central Territory’s fixed expenses are traceable to Kiks and $54,000 to Dows, with the remainder common to the two products.

-

Required:

-

-

Prepare contribution format segmented income statements, first showing the total company broken down between sales territories and then showing Central Territory broken down by product line. Show both Amount and Percentage columns for the company in total and for each segment. Round percentage computations to one decimal place.

-

Look at the statement you have prepared showing the total company segmented by sales territory. Which points revealed by this statement should be brought to management’s attention?

-

Look at the statement you have prepared showing Central Territory segmented by product lines. Which points revealed by this statement should be brought to management’s attention?

-

Homework Answers

1.

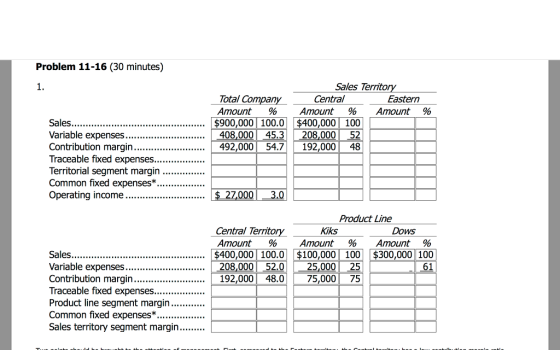

|

Sales Territory |

|||||||||

|

Total Company |

Central |

Eastern |

|||||||

|

Amount |

% |

Amount |

% |

Amount |

% |

||||

|

Sales..................................................................... |

$900,000 |

100.0 |

$400,000 |

100 |

$500,000 |

100 |

|||

|

Variable expenses................................................. |

408,000 |

45.3 |

208,000 |

52 |

200,000 |

40 |

|||

|

Contribution margin............................................ |

492,000 |

54.7 |

192,000 |

48 |

300,000 |

60 |

|||

|

Traceable fixed expenses..................................... |

290,000 |

32.2 |

160,000 |

40 |

130,000 |

26 |

|||

|

Territorial segment margin................................... |

202,000 |

22.4 |

$ 32,000 |

8 |

$170,000 |

34 |

|||

|

Common fixed expenses*................................... |

175,000 |

19.4 |

|||||||

|

Operating income................................................ |

$ 27,000 |

3.0 |

|||||||

|

*465,000 – $290,000 = $175,000. |

|

Product Line |

|||||||||

|

Central Territory |

Kiks |

Dows |

|||||||

|

Amount |

% |

Amount |

% |

Amount |

% |

||||

|

Sales..................................................................... |

$400,000 |

100.0 |

$100,000 |

100 |

$300,000 |

100 |

|||

|

Variable expenses................................................. |

208,000 |

52.0 |

25,000 |

25 |

183,000 |

61 |

|||

|

Contribution margin............................................ |

192,000 |

48.0 |

75,000 |

75 |

117,000 |

39 |

|||

|

Traceable fixed expenses..................................... |

114,000 |

28.5 |

60,000 |

60 |

54,000 |

18 |

|||

|

Product line segment margin............................... |

78,000 |

19.5 |

$ 15,000 |

15 |

$ 63,000 |

21 |

|||

|

Common fixed expenses*................................... |

46,000 |

11.5 |

|||||||

|

Sales territory segment margin............................ |

$ 32,000 |

8.0 |

|||||||

|

*$160,000 – $114,000 = $46,000. |

2.

Two points should be brought to the attention of management. First, compared to the Eastern territory, the Central territory has a low contribution margin ratio. Second, the Central territory has high traceable fixed expenses. Overall, compared to the Eastern territory, the Central territory is very weak.

3.

Again, two points should be brought to the attention of management. First, the Central territory has a poor sales mix. Note that the territory sells very little of the Kiks product, which has a high contribution margin ratio. It is this poor sales mix that accounts for the low overall contribution margin ratio in the Central territory mentioned in part (2) above. Second, the traceable fixed expenses of the Kiks product seem very high in relation to sales. These high fixed expenses may simply mean that the Kiks product is highly leveraged; if so, then an increase in sales of this product line would greatly enhance profits in the Central territory and in the company as a whole.

Add Answer to:

Creaston Limited’s most recent monthly contribution format

income statement is given below:

CREASTON LIMITED

Income Statement...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 455,000 Net operating income $ 37,000 Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: The company is divided into two sales territories—Northern and Southern. The Northern Territory recorded...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 465,000 Net operating income $ 27,000 Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: The company is divided into two sales territories—Northern and Southern. The Northern Territory recorded...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales Variable expenses Contribution margin Fixed expenses $ 800,000 300,000 500,000 460,000 $ 40,000 Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales Variable expenses Contribution margin Fixed expenses $ 800,000 300,000 500,000 460,000 $ 40,000 Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 455,000 Net operating income $ 37,000 Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: The company is divided into two sales territories—Northern and Southern. The Northern Territory recorded...

Vulcan Company's contribution format income statement for June is given below: Vulcan Company Income Statement For...

Vulcan Company's contribution format income statement for June is given below: Vulcan Company Income Statement For the Month Ended June 30 $800,000 308,000 492,000 465,000 $ 27,000 Sales Variable expenses Contribution margin Fixed expenses Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded...

Vulcan Company's contribution format income statement for June is given below: Vulcan Company Income Statement For the Month Ended June 30 $800,000 308,000 492,000 465,000 $ 27,000 Sales Variable expenses Contribution margin Fixed expenses Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded...

Problem 7-21 Segment Reporting and Decision-Making [LO7-4] Vulcan Company’s contribution format income statement for June is...

Problem 7-21 Segment Reporting and Decision-Making [LO7-4] Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 455,000 Net operating income $ 37,000 Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: The company is divided into two sales...

Problem 7-21 Segment Reporting and Decision-Making [LO7-4] Vulcan Company’s contribution format income statement for June is...

Problem 7-21 Segment Reporting and Decision-Making [LO7-4] Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 450,000 Net operating income $ 50,000 Management is disappointed with the company’s performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: The company is divided into two sales...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 485,000 Net operating income $ 15,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories–Northern and Southern. The Northern Territory...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 485,000 Net operating income $ 15,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories–Northern and Southern. The Northern Territory...

Problem 7-21 Segment Reporting and Decision-Making (L07-4] Vulcan Company's contribution format income statement for June is...

Problem 7-21 Segment Reporting and Decision-Making (L07-4] Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 480,000 Net operating income $ 12,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two...

Problem 7-21 Segment Reporting and Decision-Making (L07-4] Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 480,000 Net operating income $ 12,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two...

Vulcan Company’s contribution format income statement for June is as follows: Vulcan Company Income Statement For...

Vulcan Company’s contribution format income statement for June

is as follows:

Vulcan Company

Income Statement

For the Month Ended June 30

Sales $750,000

Variable expenses 336,000

Contribution margin 414,000

Fixed expenses 378,000

Net operating income $36,000

Management is disappointed with the company’s performance and

is wondering what can be done to improve profits. By examining

sales and cost records, you have determined the following:

The company is divided into two sales territories—Northern and

Southern. The Northern territory recorded $300,000 in...

Vulcan Company’s contribution format income statement for June

is as follows:

Vulcan Company

Income Statement

For the Month Ended June 30

Sales $750,000

Variable expenses 336,000

Contribution margin 414,000

Fixed expenses 378,000

Net operating income $36,000

Management is disappointed with the company’s performance and

is wondering what can be done to improve profits. By examining

sales and cost records, you have determined the following:

The company is divided into two sales territories—Northern and

Southern. The Northern territory recorded $300,000 in...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales Variable expenses Contribution margin Fixed expenses $ 800,000 300,000 500,000 460,000 $ 40,000 Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales Variable expenses Contribution margin Fixed expenses $ 800,000 300,000 500,000 460,000 $ 40,000 Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory...

Vulcan Company's contribution format income statement for June is given below: Vulcan Company Income Statement For the Month Ended June 30 $800,000 308,000 492,000 465,000 $ 27,000 Sales Variable expenses Contribution margin Fixed expenses Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded...

Vulcan Company's contribution format income statement for June is given below: Vulcan Company Income Statement For the Month Ended June 30 $800,000 308,000 492,000 465,000 $ 27,000 Sales Variable expenses Contribution margin Fixed expenses Net operating income Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 485,000 Net operating income $ 15,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories–Northern and Southern. The Northern Territory...

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 485,000 Net operating income $ 15,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories–Northern and Southern. The Northern Territory...

Problem 7-21 Segment Reporting and Decision-Making (L07-4] Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 480,000 Net operating income $ 12,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two...

Problem 7-21 Segment Reporting and Decision-Making (L07-4] Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $ 900,000 Variable expenses 408,000 Contribution margin 492,000 Fixed expenses 480,000 Net operating income $ 12,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two...

Vulcan Company’s contribution format income statement for June

is as follows:

Vulcan Company

Income Statement

For the Month Ended June 30

Sales $750,000

Variable expenses 336,000

Contribution margin 414,000

Fixed expenses 378,000

Net operating income $36,000

Management is disappointed with the company’s performance and

is wondering what can be done to improve profits. By examining

sales and cost records, you have determined the following:

The company is divided into two sales territories—Northern and

Southern. The Northern territory recorded $300,000 in...

Vulcan Company’s contribution format income statement for June

is as follows:

Vulcan Company

Income Statement

For the Month Ended June 30

Sales $750,000

Variable expenses 336,000

Contribution margin 414,000

Fixed expenses 378,000

Net operating income $36,000

Management is disappointed with the company’s performance and

is wondering what can be done to improve profits. By examining

sales and cost records, you have determined the following:

The company is divided into two sales territories—Northern and

Southern. The Northern territory recorded $300,000 in...

Most questions answered within 3 hours.

-

Given the line notation, identify the anodic and

cathodic reactions and overall reaction:

Ag(s)| AgCl(s) |...

asked 13 minutes ago -

The money raised and spent (both in millions of dollars) by

all congressional campaigns for 8...

asked 16 minutes ago -

Annual salaries for employees in a large company are

approximately normally distributed with a mean of...

asked 25 minutes ago -

1. Lifetimes of a certain brand of lightbulbs is known to follow

a right-skewed distribution with...

asked 25 minutes ago -

The gravitational field

F(x,y,z) =cx /(x2 + y2 + z2)3/2 e1+ cy /(x2 + y2 +...

asked 23 minutes ago -

Below is an abstract from the following paper published in

Frontiers in Cell and Developmental Biology....

asked 26 minutes ago -

Company A is assigned $200,000 of goodwill arising from a recent

business combination. The current carrying...

asked 32 minutes ago -

Write any individual Class A IP address below. It cannot be

non-routable address. Include the subnet...

asked 33 minutes ago -

Coronado Industries had January 1 inventory of $301000 when it

adopted dollar-value LIFO. During the year,...

asked 43 minutes ago -

The cable supporting a 2145-kg elevator has a maximum strength

of 2.18×104 N.

a) What maximum...

asked 52 minutes ago -

Find the critical value(s) and rejection region(s) for a

two-tailed chi-square test with a sample size...

asked 56 minutes ago -

One of your experts gave me an answer of $7.36 but there are

many different answers...

asked 1 hour ago