variable cost per unit produced and sold

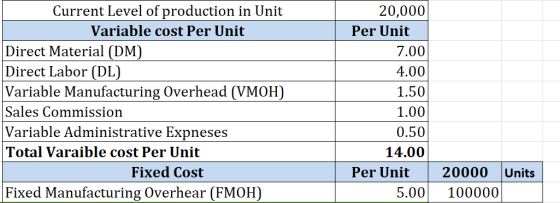

Kubin Company’s relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows:

| Amount per Unit | ||

| Direct materials | $ | 7.00 |

| Direct labor | $ | 4.00 |

| Variable manufacturing overhead | $ | 1.50 |

| Fixed manufacturing overhead | $ | 5.00 |

| Fixed selling expense | $ | 3.50 |

| Fixed administrative expense | $ | 2.50 |

| Sales commissions | $ | 1.00 |

| Variable administrative expense | $ | 0.50 |

Required:

1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold?

2. If 22,000 units are produced and sold, what is the variable cost per unit produced and sold?

3. If 18,000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold?

4. If 22,000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold?

5. If 18,000 units are produced, what is the average fixed manufacturing cost per unit produced?

6. If 22,000 units are produced, what is the average fixed manufacturing cost per unit produced?

7. If 18,000 units are produced, what is the total amount of fixed manufacturing overhead incurred to support this level of production?

8. If 22,000 units are produced, what is the total amount of fixed manufacturing overhead incurred to support this level of production?

Homework Answers

Product Cost: Product cost can be defined as the total cost incurred during the manufacturing of a product that includes direct labor, direct material and manufacturing overheads.

Absorption Costing: It refers to one of the methods to compute the cost of the manufacturing product. While computing the product cost, this method takes total cost of the product that includes variable overhead manufacturing cost as well as fixed overhead manufacturing cost.

Period Cost: It is the cost that is neither an essential part of the manufacturing process nor directly associated with the manufacturing cost.

Direct Material: It can be defined as those supplies and materials that are used for manufacturing the product and can be directly associated with the product.

Direct Labor: Direct labor can be defined as the personnel that are engaged directly in the manufacturing of products rather than its maintenance, administration, or other support services.

Variable overhead: It can be defined as a manufacturing cost that varies as per the level of production. This is used to determine future costs and expenditure of a manufacturing company. It is also used to determine the lowest possible price at which the company’s product can be sold. Example: electricity consumed by machinery.

Fixed Overhead: It refers to the cost that is to be incurred, irrespective of the level of production. They do not vary due to the change in the level of an organization’s activities. These costs are required to operate the business. Example: rent of a building, insurance, etc.

Variable Administrative Expenses: These are operating expenses other than the manufacturing costs. Some of the examples of variable administrative expenses are a commission, freight, salaries, etc.

Fixed Administrative Expenses: These refer to the operating expenses that do not change, irrespective of the level of goods manufactured. Some of the examples are rent and insurance.

Sales Commission: It can be defined as an additional income received by an employee if he meets as well as exceeds the minimum level of threshold set by the employer.

Selling expenses: These can be defined as the costs associated with selling and distribution, marketing, advertising, website maintenance, and social media expenses.

(1)

Compute the product cost incurred to make 20,000 units by K Company as shown below:

Therefore, the product cost is .

Working Notes:

Compute the direct material as shown below:

Hence, the direct material is .

Compute the direct labor as shown below:

Hence, direct labor is .

Compute the variable manufacturing overhead as shown below:

Hence, variable manufacturing overhead is .

Compute the fixed manufacturing overhead as shown below:

Hence, the fixed manufacturing overhead is .

(2)

The period cost incurred to make 20,000 units by K Company is computed as shown below:

Therefore, the period cost incurred to produce 20,000 units is $150,000.

Working Notes:

The fixed selling expenses for 20,000 units is computed as follows:

Hence, the fixed selling expenses for 20,000 units is .

The fixed administrative expenses for 20,000 units is computed as follows:

Hence, the fixed administrative expenses for 20,000 units is .

The variable administrative expenses for 20,000 units is computed as follows:

Hence, the variable administrative expenses for 20,000 units is .

The sales commission expenses for 20,000 units is computed as follows:

Hence, the sales commission for 20,000 units is .

(3)

Compute the product cost incurred to make 22,000 units by K Company:

Therefore, the product cost incurred to produce 22,000 units is .

Working Notes:

The cost of direct materials is computed as shown below:

Hence, the direct materials are worth .

The cost of direct labor is computed as shown below:

Hence, direct labor costs .

Compute the variable manufacturing overhead as shown below:

Hence, the variable manufacturing overhead is .

Compute the fixed manufacturing overhead as shown below:

Hence, the fixed manufacturing overhead is .

(4)

Compute the period cost incurred to make 18,000 units by K Company:

Therefore, the period cost is .

Working Notes

The fixed selling expenses are computed as follows:

Hence, the fixed selling expenses are .

The fixed administrative expenses are computed as follows:

Hence, the fixed administrative expenses are .

The variable administrative expenses are computed as follows:

Hence, the variable administrative expenses are .

The sales commission is computed as follows:

Hence, the sales commission amounts to .

Ans: Part 1The total product cost for producing 20,000 units is $350,000.

Part 2The total period cost for producing 20,000 units is $150,000.

Part 3The total product cost for producing 22,000 units is $375,000.

Part 4The total period cost for producing 18,000 units is $147,000.

Total Fixed Manufacturing overhead = Current levels ofUnits * FMOH per unit

= $5.00* 20,000 = 100,000

how to solve 5678? Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling...

how to solve 5678?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and...

how to solve 5678?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and...

Kubin Company’s relevant range of production is 18,000to 22,000 units. When it produces and sells...

Kubin Company’s relevant range of production is 18,000

to 22,000 units. When it produces and sells 20,000 units, its

average costs per unit are as follows:Amount per UnitDirect materials$7.00Direct labor$4.00Variable manufacturing overhead$1.50Fixed manufacturing overhead$5.00Fixed selling expense$3.50Fixed administrative expense$2.50Sales commissions$1.00Variable administrative expense$0.501. If 18,000 units are produced and sold, what is the variable

cost per unit produced and sold?2. If 22,000 units are produced and sold, what is the variable

cost per unit produced and sold?3. If 18,000 units are produced...

Kubin Company’s relevant range of production is 18,000

to 22,000 units. When it produces and sells 20,000 units, its

average costs per unit are as follows:Amount per UnitDirect materials$7.00Direct labor$4.00Variable manufacturing overhead$1.50Fixed manufacturing overhead$5.00Fixed selling expense$3.50Fixed administrative expense$2.50Sales commissions$1.00Variable administrative expense$0.501. If 18,000 units are produced and sold, what is the variable

cost per unit produced and sold?2. If 22,000 units are produced and sold, what is the variable

cost per unit produced and sold?3. If 18,000 units are produced...

EXERCISE 1-7 Direct and Indirect Costs LO1-1 Kubin Company's relevant range of production is 18,000 to...

EXERCISE 1-7 Direct and Indirect Costs LO1-1 Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Average Cost per Unit Direct materials ..... Direct labor... Variable manufacturing overhead .. Fixed manufacturing overhead........ Fixed selling expense............... Fixed administrative expense ........ Sales commissions ....... Variable administrative expense..... $7.00 $4.00 $1.50 $5.00 $3.50 $2.50 $1.00 $0.50 ut ur p o costs incurred to sell 18,000 units?...

EXERCISE 1-7 Direct and Indirect Costs LO1-1 Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Average Cost per Unit Direct materials ..... Direct labor... Variable manufacturing overhead .. Fixed manufacturing overhead........ Fixed selling expense............... Fixed administrative expense ........ Sales commissions ....... Variable administrative expense..... $7.00 $4.00 $1.50 $5.00 $3.50 $2.50 $1.00 $0.50 ut ur p o costs incurred to sell 18,000 units?...

how to solve? Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense...

how to solve?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and sold?...

how to solve?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and sold?...

Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells...

Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Direct naterials Direct labor Variable manufacturing overhead Pixed manufacturing overhead Pixed selling expense Fixed administrative expense Sales commissions Variable adninistrative expense Anount per Unit 7.00 4.00 1.50 S 5.00 3.50 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and s...

Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Direct naterials Direct labor Variable manufacturing overhead Pixed manufacturing overhead Pixed selling expense Fixed administrative expense Sales commissions Variable adninistrative expense Anount per Unit 7.00 4.00 1.50 S 5.00 3.50 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and s...

Exercise 1-9 (Algo) Fixed, Variable, and Mixed Costs [LO1-4) Required: 1. If 24.000 units are produced...

Exercise 1-9 (Algo) Fixed, Variable, and Mixed Costs [LO1-4) Required: 1. If 24.000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 31,000 units are produced and sold, what is the variable cost per unit produced and sold? 3. If 24.000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold? 4. If 31,000 units are produced and sold, what is the...

Exercise 1-9 (Algo) Fixed, Variable, and Mixed Costs [LO1-4) Required: 1. If 24.000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 31,000 units are produced and sold, what is the variable cost per unit produced and sold? 3. If 24.000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold? 4. If 31,000 units are produced and sold, what is the...

8) If 12,500 units are produced, what is the average fixed manufacturing cost per unit produced?...

8) If 12,500 units are produced, what is the average fixed

manufacturing cost per unit produced?

9) If 8,000 units are produced, what is the

total amount of fixed manufacturing cost incurred to support this

level of production?

10) If 12,500 units are produced, what is the total

amount of fixed manufacturing cost incurred to support this level

of production?

11) If 8,000 units are produced, what is the total

amount of manufacturing overhead cost incurred to support this

level of production? What...

8) If 12,500 units are produced, what is the average fixed

manufacturing cost per unit produced?

9) If 8,000 units are produced, what is the

total amount of fixed manufacturing cost incurred to support this

level of production?

10) If 12,500 units are produced, what is the total

amount of fixed manufacturing cost incurred to support this level

of production?

11) If 8,000 units are produced, what is the total

amount of manufacturing overhead cost incurred to support this

level of production? What...

Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells...

Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 8.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.70 $ 2.20 $ 1.70 Required: 1. If 22,000 units are produced and sold, what is the variable cost...

Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 8.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.70 $ 2.20 $ 1.70 Required: 1. If 22,000 units are produced and sold, what is the variable cost...

need help Exercise 1-9 Fixed, Variable, and Mixed Costs (L01-4) Kubin Company's relevant range of production...

need help

Exercise 1-9 Fixed, Variable, and Mixed Costs (L01-4) Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 3.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.79 $ 2.20 $ 1.70 Required: 1. If 22.000...

need help

Exercise 1-9 Fixed, Variable, and Mixed Costs (L01-4) Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 3.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.79 $ 2.20 $ 1.70 Required: 1. If 22.000...

Kubin Company’s relevant range of production is 29,000 to 33,000 units. When it produces and sells...

Kubin Company’s relevant range of production is 29,000 to 33,000 units. When it produces and sells 31,000 units, its average costs per unit are as follows: Amount per Unit Direct materials $ 8.90 Direct labor $ 5.90 Variable manufacturing overhead $ 3.40 Fixed manufacturing overhead $ 6.90 Fixed selling expense $ 5.40 Fixed administrative expense $ 4.40 Sales commissions $ 2.90 Variable administrative expense $ 2.40 Required: 1. If 29,000 units are produced and sold, what is the variable cost...

how to solve 5678?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and...

how to solve 5678?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and...

Kubin Company’s relevant range of production is 18,000

to 22,000 units. When it produces and sells 20,000 units, its

average costs per unit are as follows:Amount per UnitDirect materials$7.00Direct labor$4.00Variable manufacturing overhead$1.50Fixed manufacturing overhead$5.00Fixed selling expense$3.50Fixed administrative expense$2.50Sales commissions$1.00Variable administrative expense$0.501. If 18,000 units are produced and sold, what is the variable

cost per unit produced and sold?2. If 22,000 units are produced and sold, what is the variable

cost per unit produced and sold?3. If 18,000 units are produced...

Kubin Company’s relevant range of production is 18,000

to 22,000 units. When it produces and sells 20,000 units, its

average costs per unit are as follows:Amount per UnitDirect materials$7.00Direct labor$4.00Variable manufacturing overhead$1.50Fixed manufacturing overhead$5.00Fixed selling expense$3.50Fixed administrative expense$2.50Sales commissions$1.00Variable administrative expense$0.501. If 18,000 units are produced and sold, what is the variable

cost per unit produced and sold?2. If 22,000 units are produced and sold, what is the variable

cost per unit produced and sold?3. If 18,000 units are produced...

EXERCISE 1-7 Direct and Indirect Costs LO1-1 Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Average Cost per Unit Direct materials ..... Direct labor... Variable manufacturing overhead .. Fixed manufacturing overhead........ Fixed selling expense............... Fixed administrative expense ........ Sales commissions ....... Variable administrative expense..... $7.00 $4.00 $1.50 $5.00 $3.50 $2.50 $1.00 $0.50 ut ur p o costs incurred to sell 18,000 units?...

EXERCISE 1-7 Direct and Indirect Costs LO1-1 Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Average Cost per Unit Direct materials ..... Direct labor... Variable manufacturing overhead .. Fixed manufacturing overhead........ Fixed selling expense............... Fixed administrative expense ........ Sales commissions ....... Variable administrative expense..... $7.00 $4.00 $1.50 $5.00 $3.50 $2.50 $1.00 $0.50 ut ur p o costs incurred to sell 18,000 units?...

how to solve?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and sold?...

how to solve?

Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense A-ount per Unit $ 7.00 $ 4.00 $ 1.50 $ 5.00 $ 3.50 $ 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 22,000 units are produced and sold, what is the variable cost per unit produced and sold?...

Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Direct naterials Direct labor Variable manufacturing overhead Pixed manufacturing overhead Pixed selling expense Fixed administrative expense Sales commissions Variable adninistrative expense Anount per Unit 7.00 4.00 1.50 S 5.00 3.50 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and s...

Kubin Company's relevant range of production is 18,000 to 22,000 units. When it produces and sells 20,000 units, its average costs per unit are as follows: Direct naterials Direct labor Variable manufacturing overhead Pixed manufacturing overhead Pixed selling expense Fixed administrative expense Sales commissions Variable adninistrative expense Anount per Unit 7.00 4.00 1.50 S 5.00 3.50 2.50 $ 1.00 $ 0.50 Required: 1. If 18,000 units are produced and sold, what is the variable cost per unit produced and s...

Exercise 1-9 (Algo) Fixed, Variable, and Mixed Costs [LO1-4) Required: 1. If 24.000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 31,000 units are produced and sold, what is the variable cost per unit produced and sold? 3. If 24.000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold? 4. If 31,000 units are produced and sold, what is the...

Exercise 1-9 (Algo) Fixed, Variable, and Mixed Costs [LO1-4) Required: 1. If 24.000 units are produced and sold, what is the variable cost per unit produced and sold? 2. If 31,000 units are produced and sold, what is the variable cost per unit produced and sold? 3. If 24.000 units are produced and sold, what is the total amount of variable cost related to the units produced and sold? 4. If 31,000 units are produced and sold, what is the...

8) If 12,500 units are produced, what is the average fixed

manufacturing cost per unit produced?

9) If 8,000 units are produced, what is the

total amount of fixed manufacturing cost incurred to support this

level of production?

10) If 12,500 units are produced, what is the total

amount of fixed manufacturing cost incurred to support this level

of production?

11) If 8,000 units are produced, what is the total

amount of manufacturing overhead cost incurred to support this

level of production? What...

8) If 12,500 units are produced, what is the average fixed

manufacturing cost per unit produced?

9) If 8,000 units are produced, what is the

total amount of fixed manufacturing cost incurred to support this

level of production?

10) If 12,500 units are produced, what is the total

amount of fixed manufacturing cost incurred to support this level

of production?

11) If 8,000 units are produced, what is the total

amount of manufacturing overhead cost incurred to support this

level of production? What...

Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 8.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.70 $ 2.20 $ 1.70 Required: 1. If 22,000 units are produced and sold, what is the variable cost...

Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 8.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.70 $ 2.20 $ 1.70 Required: 1. If 22,000 units are produced and sold, what is the variable cost...

need help

Exercise 1-9 Fixed, Variable, and Mixed Costs (L01-4) Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 3.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.79 $ 2.20 $ 1.70 Required: 1. If 22.000...

need help

Exercise 1-9 Fixed, Variable, and Mixed Costs (L01-4) Kubin Company's relevant range of production is 22,000 to 27,000 units. When it produces and sells 24,500 units, its average costs per unit are as follows: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Fixed selling expense Fixed administrative expense Sales commissions Variable administrative expense Amount per Unit $ 3.20 $ 5.20 $ 2.70 $ 6.20 $ 4.70 $ 3.79 $ 2.20 $ 1.70 Required: 1. If 22.000...

Most questions answered within 3 hours.

-

(63

#14)

which of the following statments best describes how chamging

the concentration of the substances...

asked 3 hours ago -

In the following reaction, which element is undergoing

oxidation: Na2SO3 + N2O --> N2 + Na2SO4...

asked 3 hours ago -

Which of the following pairs of ions have the same electron

configuration?

I: Br− and Se2−...

asked 6 hours ago -

The Foremost Composite Materials Company is planning a two-day

sales conference for October 19-20. The conference...

asked 6 hours ago -

3) Illustrate the observed pattern of relatedness of organisms

versus adaptations to specific conditions. This means...

asked 7 hours ago -

In winter a lake has a 0.35 m thick ice layer over 1.10 m of

water....

asked 8 hours ago -

Assuming the following has been encrypted with a Vigenere cipher

below, use the method(s) and assumptions...

asked 8 hours ago -

How would I use switch statements to write a program that will

take an input of...

asked 8 hours ago -

Imagine a reaction in which methane gas combusts at a constant

pressure of 1 atm and...

asked 8 hours ago -

Two parallel wires (each 12 m in length) are separated by a

distance of 0.065 m...

asked 8 hours ago -

Suppose there were three masses at the corner of uniform

equilateral triangle. The masses are m1...

asked 8 hours ago -

Situation: A building that is 618 m above the ground floor. How

many times would a...

asked 8 hours ago