IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation.

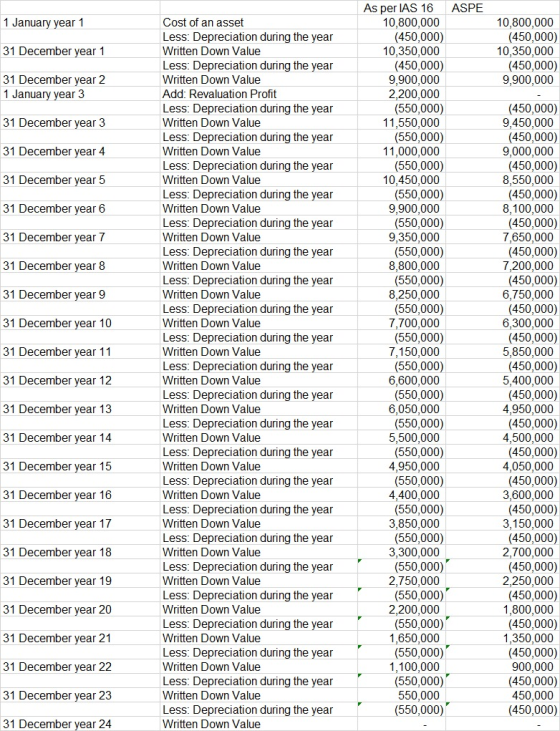

ABC Ltd., a private company, can report in accordance with either ASPE or IFRS. On January 1, Year 1, it acquired an asset at a cost of $10.8 million, which will be amortized on a straight-line basis over an estimated useful life of 24 years. On January 1, Year 3, the company hired an appraiser, who determined the fair value of the asset (net of accumulated depreciation) to be $12.1 million. The estimated useful life of the asset did not change. (Leave no cells blank - be certain to enter "0" wherever required. Enter your answers in dollars and not in millions of dollars. Answers must be numerical. Round your intermediate computations and final answers to nearest whole dollar value.)

Required:

(a) Determine the depreciation expense recognized in Year 2, Year 3, and Year 4 under

(i) the revaluation treatment allowed under IAS 16, and

| IAS 16 | |

| Year 2 | $ |

| Year 3 | $ |

| Year 4 | $ |

(ii) ASPE.

| ASPE | |

| Year 2 | $ |

| Year 3 | $ |

| Year 4 | $ |

(b) Determine the carrying amount of the asset under the two different sets of accounting requirements at January 2, Year 3; December 31, Year 3; and December 31, Year 4.

| Jan 2/Yr3 | Dec31/Yr3 | Dec31/Yr4 | |

| IAS 16 | $ | $ | $ |

| ASPE | $ | $ | $ |

(c) Determine the differences in profit and shareholders’ equity over the 24-year life of the asset using the two different sets of accounting requirements. Assume that future appraisals indicated that the fair value of the asset was equal to carrying amount.

| Difference in profit | $ |

| Difference in shareholders’ equity | $ |

*Please provide the exact answers and include the calculations. Part a,b, c.*

Homework Answers

Working Note:

Add Answer to:

IAS 16, Property, Plant, and Equipment, requires assets to be

initially measured at cost. Subsequently, assets...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation. ABC Ltd.,...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation. ABC Ltd.,...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation. ABC Ltd.,...

3-IAS 16 Property, Plant and Equipment sets out the requirements for the recognition of the asset...

3-IAS 16 Property, Plant and Equipment sets out the requirements for the recognition of the assets, the determination of their carrying amounts, and the depreciation charges and impairment losses in relation to them. Discuss the importance of two models under IAS 16 PPE and Identify the depreciation methods

Please explain Part C) summarize the difference in net income and in stockholders' equity over the...

Please explain Part C) summarize the difference in net income and in stockholders' equity over the 20 year life of the building using the 2 different sets of accounting rules. Abacab Company's shares are listed on the New Market Stock Exchange, which allows the use of either international financial reporting standards (IFRS) or U.S. GAAP. On Jan 1, Year 1, Abacab Company acquired a building at a cost of $10 million. The building has a 20-yr. useful life and no...

ACC206: Financial Reporting MCQ please help 1. According to FRS 16 Property, Plant and Equipment, gains...

ACC206: Financial Reporting MCQ please help 1. According to FRS 16 Property, Plant and Equipment, gains when selling property, plant and equipment for cash: a. are the excess of the cash proceeds over the fair value of the assets. b. are the excess of the book value of the assets over the cash proceeds. c. are part of cash flows from operations. d. None of the listed options. 2. At the end of its fiscal year, an adverse economic condition...

1) Which statement relating to revaluations of non-current assets is not true? Select one: a. A...

1) Which statement relating to revaluations of non-current assets is not true? Select one: a. A revaluation increase is regarded as income to be added to the firm's profit for the year. b. A revaluation decrease should be included as a reduction in profit. c. Before assets are revalued any existing accumulated depreciation must be written off against the asset account. d. Future depreciation charges will be based on the revalued carrying amount of the asset. 2) Which is the...

Question Three: IAS 76 Property, Plant and Equipment requires that where has been a permanent diminution...

Question Three: IAS 76 Property, Plant and Equipment requires that where has been a permanent diminution in the value of property, plant and equipment, the carrying value should be written down to the recoverable amount. 1. Describe three circumstances which indicate that an impairment loss relating to an asset may have occurred. Please explain your answer. (3 marks)

Question Three: IAS 76 Property, Plant and Equipment requires that where has been a permanent diminution in the value of property, plant and equipment, the carrying value should be written down to the recoverable amount. 1. Describe three circumstances which indicate that an impairment loss relating to an asset may have occurred. Please explain your answer. (3 marks)

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

Sunland Sdn. Bhd. has land, buildings and machineries as its Plant, Property and Equipment as at 31 December 2015.

Sunland Sdn. Bhd. has land, buildings, and machinery as its Plant, Property, and Equipment as of 31 December 2015. The company uses the straight-line depreciation method for all depreciable assets (unless otherwise stated). The company adopts the revaluation model for land and buildings and the cost model for motor vehicles and machinery. It is the policy of the company to revalue its lands and buildings annually. The following information is given in the year 2016: 1. Sunland Sdn. Bhd. has 2 machines - Coal...

(15) QUESTION 3 (IAS 16) Fire Ltd commenced in 2019 with the manufacturing of wood products...

(15) QUESTION 3 (IAS 16) Fire Ltd commenced in 2019 with the manufacturing of wood products at a new plant. The plant was purchased on 1 January 2019 for $700 000. During January 2019, some equipment was installed and other equipment was modified. Installation and modification cost amounted to $130 000. For security reasons a fence was erected at the plant at a cost of $20 000. The plant was ready for use on 1 February 2019. An opening function...

(15) QUESTION 3 (IAS 16) Fire Ltd commenced in 2019 with the manufacturing of wood products at a new plant. The plant was purchased on 1 January 2019 for $700 000. During January 2019, some equipment was installed and other equipment was modified. Installation and modification cost amounted to $130 000. For security reasons a fence was erected at the plant at a cost of $20 000. The plant was ready for use on 1 February 2019. An opening function...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation. ABC Ltd.,...

IAS 16, Property, Plant, and Equipment, requires assets to be initially measured at cost. Subsequently, assets may be carried at cost less accumulated depreciation, or they can be periodically revalued upward to current value and carried at the revalued amount less accumulated depreciation. If revalued, the adjustment is reported in other comprehensive income. Subsequent depreciation is based on the revalued amount. ASPE does not allow assets to be revalued at an amount exceeding historical cost less accumulated depreciation. ABC Ltd.,...

Question Three: IAS 76 Property, Plant and Equipment requires that where has been a permanent diminution in the value of property, plant and equipment, the carrying value should be written down to the recoverable amount. 1. Describe three circumstances which indicate that an impairment loss relating to an asset may have occurred. Please explain your answer. (3 marks)

Question Three: IAS 76 Property, Plant and Equipment requires that where has been a permanent diminution in the value of property, plant and equipment, the carrying value should be written down to the recoverable amount. 1. Describe three circumstances which indicate that an impairment loss relating to an asset may have occurred. Please explain your answer. (3 marks)

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

d. Polycarp Ltd adopts revaluation model for subsequent measurement of its intangible assets in accordance with IAS 38: Intangible assets. The policy of Polycarp is to revalue its intangible asset at the end of each year. An intangible asset with an estimated useful life of 9 years was acquired on 1 January 2018 for GH€45,000. It was revalued to GH¢54,400 on 31 December 2018 and the revaluation surplus was correctly recognized on that date. As at 31 December 2019, the...

(15) QUESTION 3 (IAS 16) Fire Ltd commenced in 2019 with the manufacturing of wood products at a new plant. The plant was purchased on 1 January 2019 for $700 000. During January 2019, some equipment was installed and other equipment was modified. Installation and modification cost amounted to $130 000. For security reasons a fence was erected at the plant at a cost of $20 000. The plant was ready for use on 1 February 2019. An opening function...

(15) QUESTION 3 (IAS 16) Fire Ltd commenced in 2019 with the manufacturing of wood products at a new plant. The plant was purchased on 1 January 2019 for $700 000. During January 2019, some equipment was installed and other equipment was modified. Installation and modification cost amounted to $130 000. For security reasons a fence was erected at the plant at a cost of $20 000. The plant was ready for use on 1 February 2019. An opening function...

Most questions answered within 3 hours.

-

Problem 2: The Problem of Social Cost. A Rancher and Farmer live

side-by-side to each other....

asked 19 seconds from now -

Define Diet counceling? What are the

responsibilities of a counselor?

asked 1 hour ago -

Hey im just confused about how to put the ' A angle n' and ' S...

asked 1 hour ago -

A short essay about the WSJ article on Oreo versus Hydrox.

asked 1 hour ago -

##8. A program contains the following function definition:

##def cube(num):

##return num * num * num...

asked 1 hour ago -

find the value z of a standard Normal variable that satisfies

each of the given conditions....

asked 2 hours ago -

"banana".find('z')

Out[22]: -1

why is this -1

python 3.7

asked 1 hour ago -

Ilegal Consideration Marna Balin was involved in two automobile

accidents in which she suffered severe injures.She...

asked 1 hour ago -

Walk through the operation of QuickSort when n = 7 and the input

array is A...

asked 1 hour ago -

Answer with True or False. Argue the answers

7) The circulation of field B on any...

asked 1 hour ago -

Chase Co. uses the perpetual inventory method. The inventory

records for Chase reflected the following

Jan...

asked 1 hour ago -

what are is the correct compression for these two ipv6 ips.. i

keep getting them wrong...

asked 1 hour ago