Mona Inc. makes and distributes bicycle accessories. To streamline its operations and to become leaner, it...

Mona Inc. makes and distributes bicycle accessories. To streamline its operations and to become leaner, it had the following transactions: It sold a machine that made some accessories for $54,600 cash. The machine originally cost $38,400 three years ago and has accumulated depreciation of $16,000. Mona Inc., owned stock of XYZ Corporation worth $24,000 at the beginning of the year and $30,460 at the end of the year. Mona sold some inventory for $14,000 with a cost of $10,000 during the year. Mona disposed of an office building with a fair market value of $150,000 for another office building of $110,000 and received $40,000 in cash. The sold building was purchased seven years ago for $124,000 and has been depreciated for $30,000. Land held for investment was sold for $56,000 with an original basis of $64,000 and no depreciation. Mona Inc. sold another machine on account in four installments notes of $24,000; the first payment was received in 2018. It purchased the machine two years earlier for $64,000 and has claimed $18,000 in depreciation on the machine. Stock originally purchased eight years ago for $4,200, was sold in 2018 for $5,500. Mona Inc. sold another machine for $14,600. The machine was purchased six months earlier for $18,000 and at the date of the sale had accumulated depreciation of $1,660. Requirements: Explain the character of gain/loss realized and recognized for each of the events in the 2018 tax year. Define Section 1231 of the Internal Revenue Code (IRC), capital gain/loss, and ordinary gain/loss. Classify each event as section1231, capital gain/loss, or ordinary income. Use provisions of the most recent tax law. From the determination made in part A, determine the net Section 1231 gain/loss and the net ordinary gain/loss to be included in its tax return. Note that Mona Inc. had a $4,000 non-recaptured net Section 1231 net losses from previous years. Using ProConnect or fillable forms, complete Mona Inc.’s Form 4797. Use the most recent and most current form available. Convert it to a Word document from a PDF or embed your PDF into Word.

Homework Answers

Below is the solution, please comment if any further explanation needed

Do like if helpful :)

Transaction 1 Section 1231 asset (with Section 1245 recapture component); total gain of $32,200, with $16,000 being a Section 1245 gain and $16,200 being a Section 1231 gain; reported in Part III of Form 4797

Transaction 2 No gain or loss

Transaction 3 Ordinary income of $4,000; not Form 4797 reportable

Transaction 4 Section 1231 asset, with portion of gain deferred under like-kind exchange rules; total gain of $40,000, with $30,000 being characterized as an unrecaptured Section 1250 gain; reported in Part I line 5 of Form 4797

Transaction 5 Capital loss of ($8,000)

Transaction 6 Section 1231 asset (with Section 1245 recapture component); total gain of $26,000 recognized in 2018, with $18,000 being ordinary under Section 1245 and $8,000 being a Section 1231 gain; note that $24,000 of gain is deferred to future tax years

Transaction 7 Long-term capital gain of $1,300

Transaction 8 Ordinary loss of ($1,740)

Total ordinary gain: $36,260 (Note that this excludes the $4,000 inventory income; inventory revenue and costs are supposed to be reported as gross receipts and cost of goods sold, not as a gain/loss transaction)

Total Section 1231 gain: $60,200

Net capital loss before limitations: ($6,700)

Explanation:

Before looking at individual transactions, it's helpful to go ahead and explain the types of gains/losses, as requested by the problem.

Broadly speaking, gains and losses can fall into one of three kinds: ordinary, capital, and Section 1231. Ordinary gains and losses typically arise in the context of disposals of true "ordinary assets" (such as receivables) or disposals of trade or business assets that were held for 1 year or less and that would otherwise qualify for Section 1231 treatment. Capital gains and losses relate to disposals of "capital assets", as defined in Section 1221. Broadly speaking, capital assets are generally thought of as things like stocks, bonds, or assets held as an investment. In actuality, capital assets include essentially any asset other than those that qualify as a true "ordinary asset" or as a Section 1231 asset. Finally, a Section 1231 asset is generally the disposal of an asset held for more than one year and used in a trade or business, subject to special rules for recapture and "look back" that will re-characterize a portion of gains as "ordinary". These classifications matter because of income characterization rules. Ordinary gains and losses are includible in or deductible against ordinary income, and in the case of gains, they are subject to the individual's regular marginal tax bracket. Capital losses face deduction limits against ordinary income ($3,000 per year for individuals, $0 for corporations). Capital gains are subject to either normal marginal tax bracket rates (for short-term capital gains) or special long-term capital gains rates (for long-term capital gains). Section 1231 gains and losses get the best of both worlds: losses are treated as ordinary losses and deductible against ordinary income; gains (except to the extent of repapture or re-characterization) are treated as long-term capital gains and use the special long-term capital gains rates. As noted, two special rules come into play for Section 1231. For machinery and equipment, any gains that would otherwise qualify under Section 1231 are subject to re-characterization as ordinary gains in an amount equal to the lesser of the actual gain or the accumulated depreciation. Also, when a business incurs a net Section 1231 loss, then for the next 5 years (look-back rule), any gains that would otherwise be Section 1231 gains are re-characterized as ordinary gains. It's also worth noting that, under Section 1250, disposals of buildings follow a similar rule to Section 1245 except that the lesser of the gain or accumulated depreciation is treated as an "unrecaptured 1250" gain. For individual taxpayers, unrecaptured 1250 gains are subject to a special maximum 25% tax rate.

With this in mind, we can analyze each type of gain/loss transaction (if any).

Transaction 1 This asset was held for more than one year and was used in a trade or business. Therefore, it will generally be a Section 1231 asset, subject to potential recapture rules. The net tax value at the time of the disposal is $22,400 ($38,400 cost less $16,000 accumulated depreciation). The net gain is $32,200 ($54,600 proceeds minus net tax value $22,400). Since this is a gain on disposal of a machinery or equipment asset with accumulated depreciation, the next step is to compute the Section 1245 recapture. This is the lesser of the gain ($32,200) or depreciation ($16,000). In this case, the Section 1245 recapture is $16,000; and the remaining $16,200 gain retains its character as a Section 1231 gain.

Transaction 2 There is no gain/loss transaction present. A mere change in the value of an asset is generally not a taxable event. While an exception does exist for a "mark to market" election, it is available only to taxpayer's whose business is trading securities. This is not Mona's primary business.

Transaction 3 The sale of inventory results in $4,000 ($14,000 sale price minus $10,000 cost) of ordinary income. Note that sales of inventory are not reportable on Form 4797.

Transaction 4 The office building is subject to a special rule for like-kind exchanges of real property. Generally, such exchanges are treated under Section 1031 and are not taxable. However, to the extent of the lesser of the gain or "boot" (i.e., not like-kind property) received, that portion is taxable. In this case, the amount realized is $150,000 ($110,000 for the like-kind building received; $40,000 in cash). The adjusted basis of the property given up is $94,000 ($124,000 cost minus $30,000 accumulated depreciation). The grand total "realized" gain is $56,000 ($150,000 minus $94,000). The recognized gain is equal to the lesser of the realized gain of $56,000 or the $40,000 cash "boot" received. In this case, the recognized gain is $40,000. This is a $40,000 Section 1231 gain (of which $30,000 would be an unrecaptured Section 1250 gain)

Transaction 5 Since this land was held for investment, it is treated as a capital asset. The ($8,000) loss ($56,000 proceeds minus $64,000 cost) is treated as a capital loss.

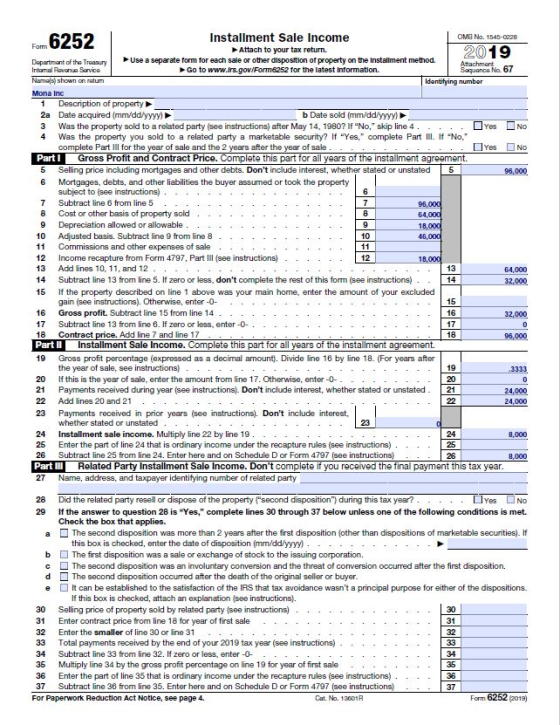

Transaction 6 This transaction requires two special rules: ordinary income recapture and an installment method sale. Broadly speaking, income from the sale of assets under the installment method is computed by first calculating the grand total expected gain on the sale of the asset, and then recognizing that gain proportionally each year as payments are received. However, to the extent of Section 1245 recapture, this portion of the gain must be recognized in the current year, even if no payments are received in the first year. The adjusted basis is $46,000 ($64,000 cost minus $18,000 accumulated depreciation). The total expected proceeds are $96,000 ($24,000 times 4 installments). The total gain is $50,000. Of this, the lesser of the $50,000 gain or $18,000 depreciation is subject to Section 1245 recapture. In this case, the recapture is $18,000, which is immediately includible in income. The remaining $32,000 gain is subject to the installment method rules. For this step, it is helpful to fill out Form 6252. But simply speaking, $8,000 of this gain is recognized in 2018. The Form 6252 computes this based on the installment gain gross profit percentage of 33.3% ($32,000 installment gain divided by $96,000 total proceeds), times the 2018 payments of $24,000, resulting in $8,000 installment gain recognized in 2018. This installment gain retains its Section 1231 character.

Transaction 7 This is a simple long-term capital gain of $1,300 ($5,500 minus $4,200).

Transaction 8 This will be an ordinary gain/loss asset because it was held for 1 year or less before disposal. The ordinary loss is ($1,740), equal to the $14,600 proceeds minus the $16,340 net tax value ($18,000 cost basis minus $1,660 accumulated depreciation). No test for Section 1245 recapture is required because (1) it's a short-term asset, and (2) the net result is a loss.

For answering the total gain and loss, it's helpful to go ahead and complete Form 4797 in order to accurately account for the various components. Note that, to more easily facilitate reporting of the Sec 1245 recapture portion of the installment sale asset, my solution includes only the $18,000 Section 1245 gain as the proceeds, cost, and accumulated depreciation on the Form 4797.

The $36,260 ordinary gain is equal to the $16,000 Section 1245 recapture in Transaction 1 + the $18,000 Section 1245 recapture in Transaction 6 + the ($1,740) ordinary loss in Transaction 8 + the $4,000 re-characterized look-back unrecaptured Section 1231 losses. Note that I am excluding the $4,000 net income from the sale of inventory. Per the Form 4797 instructions, sales of inventory are not supposed to be included. Instead, revenues and costs related to inventory are reported as gross receipts and cost of goods sold.

The $60,200 Section 1231 gain is equal to the $16,200 Section 1231 gain in Transaction 1 + the $40,000 Section 1231 gain in Transaction 4 + the $8,000 Section 1231 gain in Transaction 6 (installment method) + the ($4,000) re-characterized look-back unrecaptured Section 1231 losses.

The ($6,700) capital loss is equal to the ($8,000) capital loss in Transaction 5 + the $1,300 gain in Transaction 7.

Add Answer to:

Mona Inc. makes and distributes bicycle accessories. To

streamline its operations and to become leaner, it...

RobR manufactures and distributes high-tech hiking gadgets. It has decided to streamline some of ...

RobR manufactures and distributes high-tech hiking gadgets. It has decided to streamline some of its operations so that it will be able to be more productive and efficient. Because of this decision it has entered into several transactions during the year. Part 1 Determine the gain/loss realized and recognized in the current year for each of these events. Also determine whether the gain/loss recognized is §1231, capital, or ordinary. RobR sold a machine that it used to make computerized gadgets...

Moab Inc. manufactures and distributes high-tech biking gadgets. It has decided to streamline some of its...

Moab Inc. manufactures and distributes high-tech biking gadgets. It has decided to streamline some of its operations so that it will be able to be more productive and efficient. Because of this decision it has entered into several transactions during the year. (Do not round intermediate computations.) Moab Inc. sold a machine that it used to make computerized gadgets for $27,300 cash. It originally bought the machine for $19,200 three years ago and has taken $8,000 in depreciation. Moab...

explain pls! _6. Gary sold business equipment in the current year for a $50,000 net gain...

explain pls!

_6. Gary sold business equipment in the current year for a $50,000 net gain (after taking into account any depreciation recapture). The equipment was originally purchased two years ago and was classified as a Section 1231 asset. This was the only asset sale for the year. Five years ago, Gary had a $60,000 net Section 1231 loss but he has not had any Section 1231 transactions since then. For the current year, Gary's net Section 1231 gain is...

explain pls!

_6. Gary sold business equipment in the current year for a $50,000 net gain (after taking into account any depreciation recapture). The equipment was originally purchased two years ago and was classified as a Section 1231 asset. This was the only asset sale for the year. Five years ago, Gary had a $60,000 net Section 1231 loss but he has not had any Section 1231 transactions since then. For the current year, Gary's net Section 1231 gain is...

Bateman Corporation sold an office building that it used in its business for $800,800. Bateman bought...

Bateman Corporation sold an office building that it used in its business for $800,800. Bateman bought the building 10 years ago for $599,600 and has claimed $201,200 of depreciation expense. What is the amount and character of Bateman's gain or loss? Multiple Choice $40,240 ordinary and $362,160 §1231 gain. $201,200 ordinary and $201,200 §1231 gain. $402,400 ordinary gain. $402,400 capital gain. None of the choices are correct.

Please provide a detail step by step explanation of how you broke down the depreciation recapture...

Please provide a detail step by step explanation of how you

broke down the depreciation recapture and solved for the section

1231 gain.

7) Brandon, an individual, began business four years ago and has sold $1231 assets with $5,000 of losses within the last five years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Asset Original Cost Accumulated Depreciation Gain/loss Machinery $30,000 $7,000 $10,000 Land 40,000 20,000 Building 90,000...

Please provide a detail step by step explanation of how you

broke down the depreciation recapture and solved for the section

1231 gain.

7) Brandon, an individual, began business four years ago and has sold $1231 assets with $5,000 of losses within the last five years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Asset Original Cost Accumulated Depreciation Gain/loss Machinery $30,000 $7,000 $10,000 Land 40,000 20,000 Building 90,000...

1. Lanai, LP sold a reatal apartment complex for $950,000. Lanai purchased the building in 1991...

1. Lanai, LP sold a reatal apartment complex for $950,000. Lanai purchased the building in 1991 for 2 cast of $700,000 and had dedacted $100,000 in Section 1250 depreciation through date of sale. Lanai should characterize the $350,000 gain recognized on sale as: A. All Section 1231 gain subject to the capital gains tax rate. B. $100,000 as unrecaptured Section 1250 gain and a $250,000 Section 1231 loss. C. All unrecaptured Section 1250 gain. D. $100,000 as unrecaptured Section 1250...

1. Lanai, LP sold a reatal apartment complex for $950,000. Lanai purchased the building in 1991 for 2 cast of $700,000 and had dedacted $100,000 in Section 1250 depreciation through date of sale. Lanai should characterize the $350,000 gain recognized on sale as: A. All Section 1231 gain subject to the capital gains tax rate. B. $100,000 as unrecaptured Section 1250 gain and a $250,000 Section 1231 loss. C. All unrecaptured Section 1250 gain. D. $100,000 as unrecaptured Section 1250...

Ken sold a rental property for $860,000. He received $128,000 in the current year and $183,000...

Ken sold a rental property for $860,000. He received $128,000 in the current year and $183,000 each year for the next four years. Of the sales price, $582,500 was allocated to the building and the remaining $277,500 was allocated to the land. Ken purchased the property several years ago for $660,000. When he initially purchased the property, he allocated $570,000 of the purchase price to the building and $90,000 to the land. Ken has claimed $15,000 of depreciation deductions over...

Multiple Choice: I could use a little help. I need some guidance if possible. Brandon, an...

Multiple Choice:

I could use a little help. I need some guidance if possible.

Brandon, an individual, began business four years ago and has sold $1231 assets with $5,750 of losses within the last 5 years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Original Cost $ 31,500 55,000 120,000 Accumulated Depreciation $ 8,500 Asset Machinery Land Building Gain/Loss $ 10,750 27,500 (20,000) 35,000 Assuming Brandon's marginal ordinary income...

Multiple Choice:

I could use a little help. I need some guidance if possible.

Brandon, an individual, began business four years ago and has sold $1231 assets with $5,750 of losses within the last 5 years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Original Cost $ 31,500 55,000 120,000 Accumulated Depreciation $ 8,500 Asset Machinery Land Building Gain/Loss $ 10,750 27,500 (20,000) 35,000 Assuming Brandon's marginal ordinary income...

Ken sold a rental property for $640,000. He received $152,000 in the current year and $122,000...

Ken sold a rental property for $640,000. He received $152,000 in the current year and $122,000 each year for the next four years. Of the sales price, $535,000 was allocated to the building and the remaining $105,000 was allocated to the land. Ken purchased the property several years ago for $438,000. When he initially purchased the property, he allocated $340,000 of the purchase price to the building and $98,000 to the land. Ken has claimed $22,000 of depreciation deductions over...

Ken sold a rental property for $640,000. He received $152,000 in the current year and $122,000 each year for the next four years. Of the sales price, $535,000 was allocated to the building and the remaining $105,000 was allocated to the land. Ken purchased the property several years ago for $438,000. When he initially purchased the property, he allocated $340,000 of the purchase price to the building and $98,000 to the land. Ken has claimed $22,000 of depreciation deductions over...

A taxpayer purchased used business equipment on November 20, 2016, for $100,000. The equipment was sold...

A taxpayer purchased used business equipment on November 20, 2016, for $100,000. The equipment was sold for $60,000 on August 25, 2018. Depreciation information is as follows: Accelerated depreciation taken $47,500 Straight-line depreciation (7-year life) would have been 28,500 How will the gain or loss on the sale of this equipment be treated for tax purposes? Question 18 options: 1) $7,500 ordinary income 2) $7,500 long-term capital gain 3) $7,500 short-term capital gain 4) $7,500 Section 1231 gain 5) None...

explain pls!

_6. Gary sold business equipment in the current year for a $50,000 net gain (after taking into account any depreciation recapture). The equipment was originally purchased two years ago and was classified as a Section 1231 asset. This was the only asset sale for the year. Five years ago, Gary had a $60,000 net Section 1231 loss but he has not had any Section 1231 transactions since then. For the current year, Gary's net Section 1231 gain is...

explain pls!

_6. Gary sold business equipment in the current year for a $50,000 net gain (after taking into account any depreciation recapture). The equipment was originally purchased two years ago and was classified as a Section 1231 asset. This was the only asset sale for the year. Five years ago, Gary had a $60,000 net Section 1231 loss but he has not had any Section 1231 transactions since then. For the current year, Gary's net Section 1231 gain is...

Please provide a detail step by step explanation of how you

broke down the depreciation recapture and solved for the section

1231 gain.

7) Brandon, an individual, began business four years ago and has sold $1231 assets with $5,000 of losses within the last five years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Asset Original Cost Accumulated Depreciation Gain/loss Machinery $30,000 $7,000 $10,000 Land 40,000 20,000 Building 90,000...

Please provide a detail step by step explanation of how you

broke down the depreciation recapture and solved for the section

1231 gain.

7) Brandon, an individual, began business four years ago and has sold $1231 assets with $5,000 of losses within the last five years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Asset Original Cost Accumulated Depreciation Gain/loss Machinery $30,000 $7,000 $10,000 Land 40,000 20,000 Building 90,000...

1. Lanai, LP sold a reatal apartment complex for $950,000. Lanai purchased the building in 1991 for 2 cast of $700,000 and had dedacted $100,000 in Section 1250 depreciation through date of sale. Lanai should characterize the $350,000 gain recognized on sale as: A. All Section 1231 gain subject to the capital gains tax rate. B. $100,000 as unrecaptured Section 1250 gain and a $250,000 Section 1231 loss. C. All unrecaptured Section 1250 gain. D. $100,000 as unrecaptured Section 1250...

1. Lanai, LP sold a reatal apartment complex for $950,000. Lanai purchased the building in 1991 for 2 cast of $700,000 and had dedacted $100,000 in Section 1250 depreciation through date of sale. Lanai should characterize the $350,000 gain recognized on sale as: A. All Section 1231 gain subject to the capital gains tax rate. B. $100,000 as unrecaptured Section 1250 gain and a $250,000 Section 1231 loss. C. All unrecaptured Section 1250 gain. D. $100,000 as unrecaptured Section 1250...

Multiple Choice:

I could use a little help. I need some guidance if possible.

Brandon, an individual, began business four years ago and has sold $1231 assets with $5,750 of losses within the last 5 years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Original Cost $ 31,500 55,000 120,000 Accumulated Depreciation $ 8,500 Asset Machinery Land Building Gain/Loss $ 10,750 27,500 (20,000) 35,000 Assuming Brandon's marginal ordinary income...

Multiple Choice:

I could use a little help. I need some guidance if possible.

Brandon, an individual, began business four years ago and has sold $1231 assets with $5,750 of losses within the last 5 years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Original Cost $ 31,500 55,000 120,000 Accumulated Depreciation $ 8,500 Asset Machinery Land Building Gain/Loss $ 10,750 27,500 (20,000) 35,000 Assuming Brandon's marginal ordinary income...

Ken sold a rental property for $640,000. He received $152,000 in the current year and $122,000 each year for the next four years. Of the sales price, $535,000 was allocated to the building and the remaining $105,000 was allocated to the land. Ken purchased the property several years ago for $438,000. When he initially purchased the property, he allocated $340,000 of the purchase price to the building and $98,000 to the land. Ken has claimed $22,000 of depreciation deductions over...

Ken sold a rental property for $640,000. He received $152,000 in the current year and $122,000 each year for the next four years. Of the sales price, $535,000 was allocated to the building and the remaining $105,000 was allocated to the land. Ken purchased the property several years ago for $438,000. When he initially purchased the property, he allocated $340,000 of the purchase price to the building and $98,000 to the land. Ken has claimed $22,000 of depreciation deductions over...

Most questions answered within 3 hours.

-

Two small plastic spheres are given positive electrical charges.

When they are a distance of 15.4...

asked 40 minutes ago -

how

does gravity affect the trajectory of projectile? what would be the

shape of the trajactory...

asked 33 minutes ago -

An acidic solution containing gold ions is

electrolyzed, producing gaseous oxygen (from water) at the anode...

asked 56 minutes ago -

Assume that the population of Mexico is 128

million and that the population increases 1.01

percentannually....

asked 1 hour ago -

Can someone please help me add appropriate descriptive

comments to each line of code in the...

asked 2 hours ago -

Romeo wishes to throw a bouquet of flowers to Juliet, who is on

a second-story balcony,...

asked 2 hours ago -

Why is QE a controversial monetary policy tool.

A. It may lead to excessive inflation.B. By...

asked 3 hours ago -

Principles of Programming midterm study guide help!

1.)

______ Which of the following would reference the...

asked 2 hours ago -

A finite potential well has depth U0 = 2.78 eV . What is the

penetration distance...

asked 3 hours ago -

1. The bus bars of a power station are in two sections A and B

separated...

asked 3 hours ago -

Fiscal policy is the deliberate manipulation of taxes and

government spending to alter GDP, employment, inflation...

asked 4 hours ago -

evaluating an expression using only one digit and + and - as

operators ....3+5-1+7-5+8

-----------------------

stack...

asked 4 hours ago