DQ 1: The following are various management assertions related to sales and account receivable. Required: For...

DQ 1:

The following are various management assertions related to sales and account receivable.

Required:

- For each assertion, indicate whether it is an assertion about classes of transactions and events or an assertion about account balances.

- Indicate the name of the assertion made by management.

|

|

CATEGORY OF |

|

|

a. Recorded accounts receivable exist. |

||

|

b. Disclosures related to sales are relevant and understandable. |

||

|

c. Recorded sales transactions have occurred. |

||

|

d. There are no liens or other restrictions on accounts receivable. |

||

|

e. All sales transactions

have |

||

|

f. Receivables are appropriately classified as to trade and other receivables in the financial statements and are clearly described. |

||

|

g. Sales transactions have been recorded in the proper period. |

||

|

h. Accounts receivable

are |

||

|

i. Sales transactions have been recorded in the appropriate accounts. |

||

|

j. All required

disclosures about accounts receivables have |

||

|

k. All accounts receivable have been recorded. |

||

|

l. Disclosures related to receivables are at the correct amounts. |

||

|

m. Sales transactions have been recorded at the correct amounts. |

DQ 2:

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence: (1) physical examination, (2) confirmation, (3) inspection, (4) observation, (5) inquiry of the client, (6) recalculation, (7) reperformance, and (8) analytical procedure.

|

Type of Evidence |

Audit Procedures |

|

1. Watch client employees count inventory to determine whether company procedures are being followed. |

|

|

2. Count inventory items and record the amount in the audit files. |

|

|

3. Trace postings from the sales journal to the general ledger accounts. |

|

|

4. Calculate the ratio of cost of goods sold to sales as a test of overall reasonableness of gross margin relative to the preceding year. |

|

|

5. Obtain information about the client's internal controls by asking questions of client personnel. |

|

|

6. Trace column totals from the cash disbursements journal to the general ledger. |

|

|

7. Examine a piece of equipment to make sure a recent purchase of equipment was actually received and is in operation. |

|

|

8. Review the total of repairs and maintenance for each month to determine whether any month's total was unusually large. |

|

|

9. Compare vendor names and amounts on purchase invoices with entries in the purchases journal. |

|

|

10. Foot entries in the sales journal to determine whether they were correctly totaled by the client. |

|

|

11. Make a surprise count of petty cash to verify that the amount of the petty cash fund is intact. |

|

|

12. Obtain a written statement from the client's bank stating the client's year-end balance on deposit. |

DQ 3:

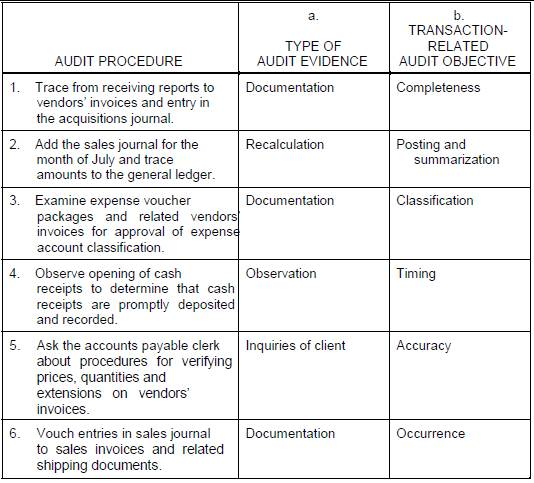

The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6.

Required:

- Identify the type of audit evidence used for each audit procedure.

- Identify the general transaction-related audit objective or objectives satisfied by each audit procedure.

|

AUDIT PROCEDURE |

|

TRANSACTION- |

|

1. Trace from receiving reports to vendors’ invoices and entry in the acquisitions journal. |

||

|

2. Add the sales journal for the month of July and trace amounts to the general ledger. |

||

|

3. Examine expense voucher packages and related vendors’ invoices for approval of expense account classification. |

||

|

4. Observe opening of cash receipts to determine that cash receipts are promptly deposited and recorded. |

||

|

5. Ask the accounts payable clerk about procedures for verifying prices, quantities, and extensions on vendors’ invoices. |

||

|

6. Vouch entries in

sales journal |

||

|

7. Examine the footnotes about the company’s policies for recording revenue transactions to determine whether the disclosures are reasonable. |

Homework Answers

Q 1:

Q 2:

ANSWER:- Each procedure according to the following types of audit evidence are as:-

1)Watch client employees count inventory to determine whether company procedures are been followed:- Observation audit evidence.

2)Calculate the ratio of cost of goods sold to sales as a test of overall reasonableness of gross margin relative to the preceding year:-Analytical procedure audit evidence.

3)Obtain information about the client’s internal controls by asking questions of client personnel:- Inquiry of client audit evidence.

4)Examine a piece of equipment to make sure a recent purchase of equipment was actually received and is in operation:-Physical examination audit evidence.

5)Compare vendor names customer and amounts on purchases invoices with entries in the purchases journal:-Documentation audit evidence.

6)Obtained a written statement from the client’s bank stating the client’s year-end balance on deposit:-Confirmation audit evidence.

7) Reposting from the sales journal to the general ledger account:- Reperformance type audit evidence.

Q 3:

Add Answer to:

DQ 1:

The following are various management assertions related to sales

and account receivable.

Required:

For...

The following are various management assertions (a. through m.) related to sales and accounts receivable. Management...

The following are various management assertions (a. through m.) related to sales and accounts receivable. Management Assertion Receivables are appropriately classified as to trade and other receivables in the financial statements and are clearly described. Sales transactions have been recorded in the proper period. Accounts receivable are recorded at the correct amounts. Sales transactions have been recorded in the appropriate accounts. All required disclosures about sales and receivables have been made. All accounts receivable have been recorded. Disclosures related to...

6-30 (Objective 6-8) The following are various management assertions (a. through m.) related to sales and...

6-30 (Objective 6-8) The following are various management assertions (a. through m.) related to sales and accounts receivable. Management Assertion Receivables are appropriately classified as to trade and other receivables in the financial statements and are clearly described. Sales transactions have been recorded in the proper period. Accounts receivable are recorded at the correct amounts. Sales transactions have been recorded in the appropriate accounts. All required disclosures about sales and receivables have been made. All accounts receivable have been recorded....

7-30 (OBJECTIVE 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives...

7-30 (OBJECTIVE 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the sales journal for the month of July and trace amounts to the general ledger. 3. Examine expense voucher packages and related vendors' invoices for approval of expense account classification....

7-30 (OBJECTIVE 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the sales journal for the month of July and trace amounts to the general ledger. 3. Examine expense voucher packages and related vendors' invoices for approval of expense account classification....

Auditing The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed...

Auditing

The following are various audit procedures performed to satisfy

specific transaction-related audit objectives as discussed in

Chapter 6. The general transaction-related audit objectives from

Chapter 6 are also included.

(Objective 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the...

Auditing

The following are various audit procedures performed to satisfy

specific transaction-related audit objectives as discussed in

Chapter 6. The general transaction-related audit objectives from

Chapter 6 are also included.

(Objective 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the...

14-26 (Objective 14-3) The following are selected transaction-related audit objectives and audit procedures for sales transactions:...

14-26 (Objective 14-3) The following are selected transaction-related audit objectives and audit procedures for sales transactions: Transaction-Related Audit Objectives 1. Recorded sales exist. 2. Existing sales are recorded. 3. Sales transactions are correctly included in the accounts receivable master file and are correctly summarized. Procedures 1. Trace a sample of shipping documents to related duplicate sales invoices and the sales journal to make sure that the shipment was billed. 2. Examine a sample of duplicate sales invoices to determine whether...

Situation No. 1: Management assertions Listed below are various management assertions related to inventory and cost...

Situation No. 1: Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. 2. All inventory have been recorded. 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. 5. Recorded cost of sales transactions have...

Situation No. 1: Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. 2. All inventory have been recorded. 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. 5. Recorded cost of sales transactions have...

Audit and Investigation work. Can you please assist me.Thank you B- ASSERTIONS AND AUDIT OBJECTIVES: The...

Audit and Investigation work. Can you please assist me.Thank you B- ASSERTIONS AND AUDIT OBJECTIVES: The following are specific balance related audit objective applied to the audit of accounts receivable (a thu h) and management assertions about account balances (1 thu 4) The list referred to in the specific balance related audit objectives is the list of the accounts receivable from each customer at the balance sheet date. Specific Balance Related Audit Objective a) There are no unrecorded receivables b)...

Stenton to Management assertions Listed below are various management assertions related to inventory and cost of...

Stenton to Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. _2. All inventory have been recorded 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. _5. Recorded cost of sales transactions have occurred....

Stenton to Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. _2. All inventory have been recorded 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. _5. Recorded cost of sales transactions have occurred....

18 The following (1 through 16) are the balance-related and transaction-related audit objectives. 1 2 3...

18 The following (1 through 16) are the balance-related and transaction-related audit objectives. 1 2 3 Balance-related objectives Existence Completeness Accuracy Cutoff Detail tie-in Realizable value Classification Rights & obligations Presentation 4 5 6 7 8 9 Transaction-related objectives Occurrence Completeness Accuracy Classification Timing Posting & summarization Presentation 10 11 12 13 14 15 16 Identify and write the number of the specific audit objective (1 through 16) that each of the following specific audit procedures satisfies in the audit...

18 The following (1 through 16) are the balance-related and transaction-related audit objectives. 1 2 3 Balance-related objectives Existence Completeness Accuracy Cutoff Detail tie-in Realizable value Classification Rights & obligations Presentation 4 5 6 7 8 9 Transaction-related objectives Occurrence Completeness Accuracy Classification Timing Posting & summarization Presentation 10 11 12 13 14 15 16 Identify and write the number of the specific audit objective (1 through 16) that each of the following specific audit procedures satisfies in the audit...

Learning objectives addressed by this exercise: Chapter 3-Learning Objectives 4 1. The following are ten various...

Learning objectives addressed by this exercise: Chapter 3-Learning Objectives 4 1. The following are ten various audit procedures performed to satisfy specific audit objectives related to management assertions. 1. Read the footnote in the most recent interim financial statements for information regarding the monetary losses from resolution of a lawsuit that was still pending at year-end. The footnote in the year-end financials indicates that the likelihood of a loss is remote. 2. Totaling to ensure that the current and long-term...

7-30 (OBJECTIVE 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the sales journal for the month of July and trace amounts to the general ledger. 3. Examine expense voucher packages and related vendors' invoices for approval of expense account classification....

7-30 (OBJECTIVE 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the sales journal for the month of July and trace amounts to the general ledger. 3. Examine expense voucher packages and related vendors' invoices for approval of expense account classification....

Auditing

The following are various audit procedures performed to satisfy

specific transaction-related audit objectives as discussed in

Chapter 6. The general transaction-related audit objectives from

Chapter 6 are also included.

(Objective 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the...

Auditing

The following are various audit procedures performed to satisfy

specific transaction-related audit objectives as discussed in

Chapter 6. The general transaction-related audit objectives from

Chapter 6 are also included.

(Objective 7-4) The following are various audit procedures performed to satisfy specific transaction-related audit objectives as discussed in Chapter 6. The general transaction-related audit objectives from Chapter 6 are also included. Audit Procedures 1. Trace from receiving reports to vendors' invoices and entries in the acquisitions journal. 2. Add the...

Situation No. 1: Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. 2. All inventory have been recorded. 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. 5. Recorded cost of sales transactions have...

Situation No. 1: Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. 2. All inventory have been recorded. 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. 5. Recorded cost of sales transactions have...

Stenton to Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. _2. All inventory have been recorded 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. _5. Recorded cost of sales transactions have occurred....

Stenton to Management assertions Listed below are various management assertions related to inventory and cost of sales. Match the management assertion that is most likely being tested. A. Existence and Occurrence B. Rights and Obligations C. Completeness D. Valuation or Allocation E. Presentation and Disclosure 1. Recorded inventory exist. _2. All inventory have been recorded 3. Inventory are recorded at the correct amounts. 4. All cost of sales transactions have been recorded. _5. Recorded cost of sales transactions have occurred....

18 The following (1 through 16) are the balance-related and transaction-related audit objectives. 1 2 3 Balance-related objectives Existence Completeness Accuracy Cutoff Detail tie-in Realizable value Classification Rights & obligations Presentation 4 5 6 7 8 9 Transaction-related objectives Occurrence Completeness Accuracy Classification Timing Posting & summarization Presentation 10 11 12 13 14 15 16 Identify and write the number of the specific audit objective (1 through 16) that each of the following specific audit procedures satisfies in the audit...

18 The following (1 through 16) are the balance-related and transaction-related audit objectives. 1 2 3 Balance-related objectives Existence Completeness Accuracy Cutoff Detail tie-in Realizable value Classification Rights & obligations Presentation 4 5 6 7 8 9 Transaction-related objectives Occurrence Completeness Accuracy Classification Timing Posting & summarization Presentation 10 11 12 13 14 15 16 Identify and write the number of the specific audit objective (1 through 16) that each of the following specific audit procedures satisfies in the audit...

Most questions answered within 3 hours.

-

A sine wave signal is displayed on the screen of an

oscilloscope. 6 peak-to-peak divisions are...

asked 1 hour ago -

a

1500 kg car accelerates from 0 to 25 m / s in 21.0s. How much...

asked 2 hours ago -

Calculate the molarity of each of the following solutions:

(a) 30.5 g of ethanol (C2H5OH) in...

asked 2 hours ago -

1 Refer to the build-borrow-or-buy framework as a decision tree

for the Adidas company. Identify a...

asked 2 hours ago -

Problem 2: The Problem of Social Cost. A Rancher and Farmer live

side-by-side to each other....

asked 3 hours ago -

a uniform bar of weight 40N is 4 meter long. weights

on 60N and 100N are...

asked 3 hours ago -

Define Diet counceling? What are the

responsibilities of a counselor?

asked 5 hours ago -

Hey im just confused about how to put the ' A angle n' and ' S...

asked 5 hours ago -

A short essay about the WSJ article on Oreo versus Hydrox.

asked 5 hours ago -

##8. A program contains the following function definition:

##def cube(num):

##return num * num * num...

asked 5 hours ago -

find the value z of a standard Normal variable that satisfies

each of the given conditions....

asked 5 hours ago -

"banana".find('z')

Out[22]: -1

why is this -1

python 3.7

asked 5 hours ago