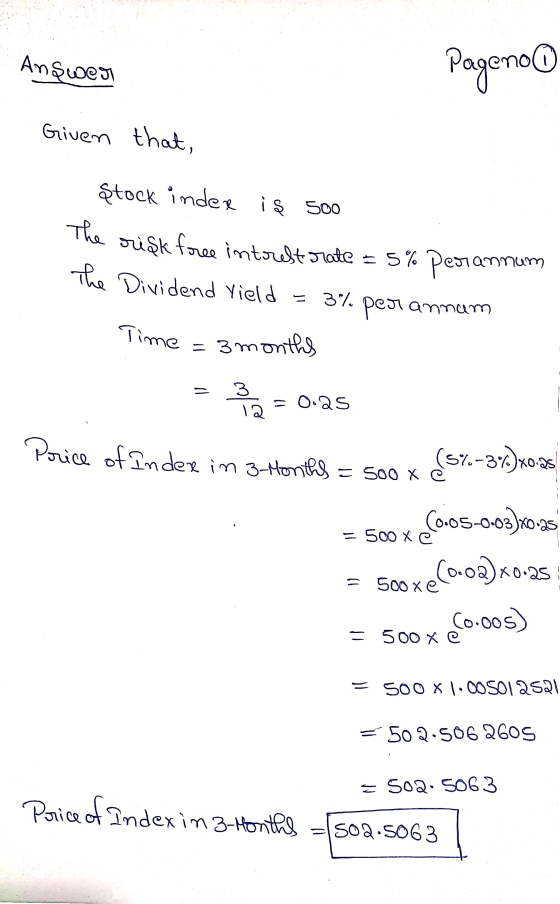

A stock index currently stands at 500. The risk-free interest rate is 5 percent per annum...

A stock index currently stands at 500. The risk-free interest rate is 5 percent per annum (with continuous compounding) and the dividend yield is 3 percent per annum. What should the futures price for a 3-month contract be?

Homework Answers

Add Answer to:

A stock index currently stands at 500. The risk-free interest

rate is 5 percent per annum...

3. Suppose that the risk-free interest rate is 6% per annum dividend yield on a stock...

3. Suppose that the risk-free interest rate is 6% per annum dividend yield on a stock index is 4% per annum. The index is standing at 400, and the futures price for a contract deliverable in four months is 405. What arbitroge opportunities does this create? with continuous compounding and that the

3. Suppose that the risk-free interest rate is 6% per annum dividend yield on a stock index is 4% per annum. The index is standing at 400, and the futures price for a contract deliverable in four months is 405. What arbitroge opportunities does this create? with continuous compounding and that the

Suppose that the risk-free interest rate is 8% per annum with continuous compounding and that the dividend yield on a st...

Suppose that the risk-free interest rate is 8% per annum with continuous compounding and that the dividend yield on a stock index is 3% per annum with continuous compounding. The index is standing at 350 and the futures price for a contract deliverable in 6months is 360. #1) What should be the theoretical futures price for the stock index? #2) What arbitrage opportunities does this create? #1) theoretical futures price = $366.38 #1) theoretical futures price = $358.86 #1) theoretical...

A stock index is currently 990, the risk free rate is 5%, and the dividend yield...

A stock index is currently 990, the risk free rate is 5%, and the dividend yield on the index is 2%. Use a three step to value and 18-month American put option with a strike price of 1000 when the volatility is 20% per annum. What position in the stock is initially necessary to hedge the risk of the put option?

50.The oil price is currently $95 per barrel. The risk-free interest rate is 3% per annum,...

50.The oil price is currently $95 per barrel. The risk-free interest rate is 3% per annum, and the convenience yield of oil is 4% per annum. Consider an oil futures contract with a maturity of 6 months. Assuming the 6 months storage cost is equal to $1.50 per barrel, the no-arbitrage futures price is closest to: (a) 95.02 (b) 95.55 (c) 96.02 (d)96.55

50.The oil price is currently $95 per barrel. The risk-free interest rate is 3% per annum, and the convenience yield of oil is 4% per annum. Consider an oil futures contract with a maturity of 6 months. Assuming the 6 months storage cost is equal to $1.50 per barrel, the no-arbitrage futures price is closest to: (a) 95.02 (b) 95.55 (c) 96.02 (d)96.55

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4%...

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

A stock is currently priced at $52.00. The risk free rate is 4.6% per annum with...

A stock is currently priced at $52.00. The risk free rate is 4.6% per annum with continuous compounding. In 5 months, its price will be $60.84 with probability 0.57 or $44.72 with probability 0.43. Using the binomial tree model, compute the present value of your expected profit if you buy a 5 month European call with strike price $57.00. Recall that profit can be negative.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7% per year w...

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7% per year with continuous compounding. The dividend yield of S&P 500 is 1.92% per year. The volatility of S&P 500 is 21%. Compute the prices of 6-month at-the-money European call and put options in the Black-Scholes-Merton model. (Keep 6 digits after the decimal point in your calculations) I.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7%...

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7% per year with continuous compounding. The dividend yield of S&P 500 is 1.92% per year. The volatility of S&P 500 is 21%. Compute the prices of 6-month at-the-money European call and put options in the Black-Scholes-Merton model. (Keep 6 digits after the decimal point in your calculations) I.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7%...

A stock is currently priced at $47.00 and pays a dividend yield of 3.7% per annum....

A stock is currently priced at $47.00 and pays a dividend yield of 3.7% per annum. The risk-free rate is 5.3% per annum with continuous compounding. In 18 months, the stock price will be either $40.89 or $52.64. Using the binomial tree model, compute the price of a 18 month European call with strike price $48.74.

A stock is currently priced at $51.00 and pays a dividend yield of 4.3% per annum....

A stock is currently priced at $51.00 and pays a dividend yield of 4.3% per annum. The risk-free rate is 5.7% per annum with continuous compounding. In 12 months, the stock price will be either $41.31 or $57.12. Using the binomial tree model, compute the price of a 12 month European call with strike price $50.32.

A stock is currently priced at $75.00. The risk free rate is 4.5% per annum with continuous compounding. Use a one-time...

A stock is currently priced at $75.00. The risk free rate is 4.5% per annum with continuous compounding. Use a one-time step Cox-Ross-Rubenstein model for the price of the stock in 13 months assuming the stock has annual volatility of 24.9%. Compute the price of a 13 month call option on the stock with strike $80.00.

3. Suppose that the risk-free interest rate is 6% per annum dividend yield on a stock index is 4% per annum. The index is standing at 400, and the futures price for a contract deliverable in four months is 405. What arbitroge opportunities does this create? with continuous compounding and that the

3. Suppose that the risk-free interest rate is 6% per annum dividend yield on a stock index is 4% per annum. The index is standing at 400, and the futures price for a contract deliverable in four months is 405. What arbitroge opportunities does this create? with continuous compounding and that the

50.The oil price is currently $95 per barrel. The risk-free interest rate is 3% per annum, and the convenience yield of oil is 4% per annum. Consider an oil futures contract with a maturity of 6 months. Assuming the 6 months storage cost is equal to $1.50 per barrel, the no-arbitrage futures price is closest to: (a) 95.02 (b) 95.55 (c) 96.02 (d)96.55

50.The oil price is currently $95 per barrel. The risk-free interest rate is 3% per annum, and the convenience yield of oil is 4% per annum. Consider an oil futures contract with a maturity of 6 months. Assuming the 6 months storage cost is equal to $1.50 per barrel, the no-arbitrage futures price is closest to: (a) 95.02 (b) 95.55 (c) 96.02 (d)96.55

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7% per year with continuous compounding. The dividend yield of S&P 500 is 1.92% per year. The volatility of S&P 500 is 21%. Compute the prices of 6-month at-the-money European call and put options in the Black-Scholes-Merton model. (Keep 6 digits after the decimal point in your calculations) I.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7%...

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7% per year with continuous compounding. The dividend yield of S&P 500 is 1.92% per year. The volatility of S&P 500 is 21%. Compute the prices of 6-month at-the-money European call and put options in the Black-Scholes-Merton model. (Keep 6 digits after the decimal point in your calculations) I.

(5 points) The value of S&P 500 is currently 2800. The risk-free interest rate is 2.7%...

Most questions answered within 3 hours.

-

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 39 minutes ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 38 minutes ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 43 minutes ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 53 minutes ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 1 hour ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 1 hour ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 1 hour ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 1 hour ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 1 hour ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 1 hour ago -

Imagine that a chemist puts 6.40 mol each of

C3H8 and O2 in a 1.00-L container...

asked 1 hour ago -

How much money should be invested today in order to have $8340

at the end of...

asked 1 hour ago