STEP 1: Create the following Journal Entries:

- The raw materials were purchased for use in production, $205,000 on account.

- The raw materials used in production (all direct materials), $190,000.

- The utility bills were incurred on account, $60,000 (90% related to factory operations, and the remainder related to selling and administrative activities).

- The salary and wage costs accrued were $235,000 (Direct labor), $91,000 (Indirect labor), $115,000 (Selling and administrative salaries).

- The maintenance costs were incurred on account in the factory, $55,000.

- The advertising costs were incurred on account, $137,000.

- The depreciation was recorded for the year, $85,000 (70% related to factory equipment, and the remainder related to selling and administrative equipment).

- The entry for rental cost incurred on account on buildings, $110,000 (75% related to factory facilities, and the remainder related to selling and administrative facilities).

- The entry for manufacturing overhead cost applied to jobs.

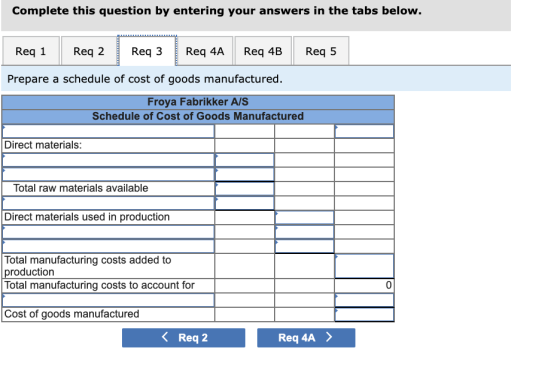

- The cost of goods manufactured for the year, $780,000.

- The sales for the year (all on account) totaled $1,250,000.

- The goods cost $810,000 according to their job cost sheets.

STEP 2: Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.)

STEP 3: Prepare a schedule of cost of goods manufactured.

STEP 4-A: Prepare a journal entry to close any balance

in the Manufacturing Overhead account to Cost of Goods

Sold.

STEP 4-B: Prepare a schedule of cost of goods sold.

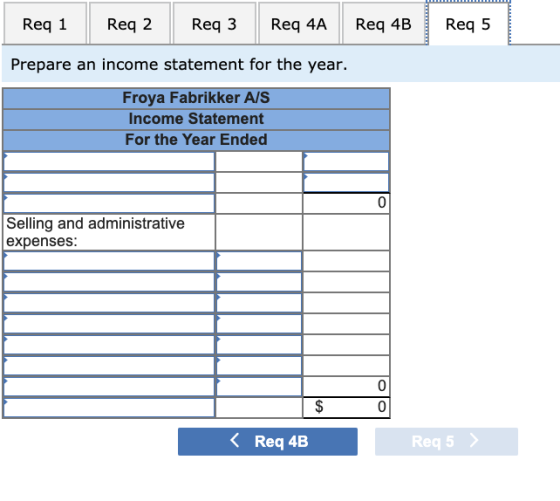

STEP 5: Prepare an income statement for the year.

Sorry, it's a long question, I greatly appreciate your time!

Homework Answers

Add Answer to:

STEP 1: Create the following Journal

Entries:

The raw materials were purchased for use in production,...

1. Prepare journal entries to record the preceding transactions. 2. Post your entries to T-accounts. (Don’t...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Problem 3-15 Journal Entries; T-Accounts;...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

a. Raw materials purchased on account, $290,000. . Raw materials used in production (all direct materials)....

a. Raw materials purchased on account, $290,000. . Raw materials used in production (all direct materials). $275,000. . Utility bills incurred on account, $77,000 (90% related to factory operations, and the remainder related to selling and administrative activities). . Accrued salary and wage costs: Direct labor (970 hours) Indirect labor Selling and administrative salaries $320,000 $ 108,000 $200,000 2. Maintenance costs incurred on account in the factory, $72,000 f. Advertising costs incurred on account, $154,000. ). Depreciation was recorded for...

a. Raw materials purchased on account, $290,000. . Raw materials used in production (all direct materials). $275,000. . Utility bills incurred on account, $77,000 (90% related to factory operations, and the remainder related to selling and administrative activities). . Accrued salary and wage costs: Direct labor (970 hours) Indirect labor Selling and administrative salaries $320,000 $ 108,000 $200,000 2. Maintenance costs incurred on account in the factory, $72,000 f. Advertising costs incurred on account, $154,000. ). Depreciation was recorded for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

a. Raw materials purchased on account, $290,000. . Raw materials used in production (all direct materials). $275,000. . Utility bills incurred on account, $77,000 (90% related to factory operations, and the remainder related to selling and administrative activities). . Accrued salary and wage costs: Direct labor (970 hours) Indirect labor Selling and administrative salaries $320,000 $ 108,000 $200,000 2. Maintenance costs incurred on account in the factory, $72,000 f. Advertising costs incurred on account, $154,000. ). Depreciation was recorded for...

a. Raw materials purchased on account, $290,000. . Raw materials used in production (all direct materials). $275,000. . Utility bills incurred on account, $77,000 (90% related to factory operations, and the remainder related to selling and administrative activities). . Accrued salary and wage costs: Direct labor (970 hours) Indirect labor Selling and administrative salaries $320,000 $ 108,000 $200,000 2. Maintenance costs incurred on account in the factory, $72,000 f. Advertising costs incurred on account, $154,000. ). Depreciation was recorded for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Most questions answered within 3 hours.

-

A pipe is open on both ends. The diameter of the pipe is 5.0 cm

and...

asked 5 minutes ago -

How many times more light does a 16-inch diameter telescope

mirror gather than your 2-inch telescope?

asked 7 minutes ago -

11.At present, the cost of the clean air and water regulations

is

A) higher then the...

asked 7 minutes ago -

2. How long would it take for 1.50 mol of water at 100.0 ∘C to

be...

asked 23 minutes ago -

According to the February 2008 Federal Trade Commission report

on consumer fraud and identity theft, 23%...

asked 36 minutes ago -

Data is only as good as its completeness. And we have all dealt

with incomplete data....

asked 31 minutes ago -

Design a Class Diagram for a game of Dots and Boxes

that can do the

following:...

asked 37 minutes ago -

Describe the Christian Anfinsen’s experimentS AND explain how

they have resulted in our current understanding of...

asked 46 minutes ago -

Do a research and write about the below areas of

SPAIN country business activities (GLOBAL

BUSINESS)...

asked 49 minutes ago -

Production and operations management involves three main types

of decisions that are made at three different...

asked 50 minutes ago -

When parked, your car is 6.4 m long. Unfortunately, your garage

is only 3.9 m long....

asked 1 hour ago -

Use Python 3 in Jupyter

Write a function called countUnique that has one parameter which

is...

asked 58 minutes ago