Joint cost allocation

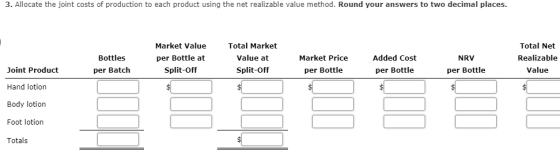

Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions are produced jointly in a mixing process that costs a total of $250 per batch. At the split-off point, one batch produces 80, 40, and 25 bottles of hand, body, and foot lotion, respectively. After the split-off point, hand lotion is sold immediately for $2.50 per bottle. Body lotion is processed further at an additional cost of $0.25 per bottle and then sold for $5.75 per bottle. Foot lotion is processed further at an additional cost of $0.85 per bottle and then sold for $4.00 per bottle. Assume that body and foot lotion could be sold at the split-off point for $3.00 and $3.20 per bottle, respectively.

1. Using the market value at split-off method, allocate the joint costs of production to each product. Round your answers to two decimal places.

| Joint Product | Bottles per Batch |

Market

Value per Bottle at Split-Off |

Total

Market Value at Split-Off |

Percent

of Total MV at Split-Off |

Joint Costs | Allocation |

| Hand lotion | $ | $ | % | $ | $ | |

| Body lotion | % | |||||

| Foot lotion | % | |||||

| Totals | $ | $ |

2. A lotion manufacturing company produces three types of lotions. After the split-off point the company continues to sell the body lotion and makes $0.25 profit per bottle. The foot lotion generates $0.05 loss per bottle if it continues after the split-off point. Which lotion should be continued after the split-off point?

a. Hand lotion

b. Body lotion

Homework Answers

1) Allocation of joint costs by split-off method (Amounts in $)

| Joint Product | Bottles per Batch (A) |

Market Value per Bottle at Split-Off (B) |

Total Market Value at Split-Off (C = A*B) |

Percent of Total MV at Split-Off (D) |

Joint Costs (E) | Allocation (D*E) |

| Hand lotion | 80 | 2.50 | 200 | 50% [(200/400)*100] | 250 | 125 |

| Body lotion | 40 | 3.00 | 120 | 30% [(120/400)*100] | 75 | |

| Foot lotion | 25 | 3.20 | 80 | 20% [(80/400)*100] | 50 | |

| Totals | 400 | $250 |

2) The body lotion generates $0.25 profit per bottle if it continues after the split-off point whereas the foot lotion generates $0.05 loss per bottle if it continues after the split-off point. Hence the company should continue body lotion after the split off point. The correct option is b) Body lotion.

3) Allocation of Joint Cost by Net Realizable Value Method

| Joint Product | Bottles per Batch (A) |

Market Value per Bottle at Split-Off (B) |

Total Market Value at Split-Off (C = A*B) |

Market Price per Bottle (C) | Added Cost per Bottle (D) | NRV per bottle (E = C-D) | Total Net Realizable value (E*A) | Greater of Total NRV and Total Market Value at Split-off | Proportion (F) | Joint Costs (G) | Allocation (F*G) |

| Hand lotion | 80 | 2.50 | 200 | $2.50 | $0 | $2.50 | $200 | 200 | 40% [(200/500)*100] | $250 | $100 |

| Body lotion | 40 | 3.00 | 120 | $5.75 | $0.25 | $5.50 | $220 | 220 | 44% [(220/500)*100] | $110 | |

| Foot lotion | 25 | 3.20 | 80 | $4.00 | $0.85 | $3.15 | $78.75 | 80 | 16% [(80/500)*100] | $40 | |

| Totals | $400 | $498.75 | $500 | $250 |

Add Answer to:

Joint cost allocation

Lovely Lotion Inc. produces three different lotions: hand, body,

and foot. The lotions...

Joint cost allocation Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions...

Joint cost allocation Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions are produced jointly in a mixing process that costs a total of $250 per batch. At the split-off point, one batch produces 80, 40, and 25 bottles of hand, body, and foot lotion, respectively. After the split-off point, hand lotion is sold immediately for $2.50 per bottle. Body lotion is processed further at an additional cost of $0.25 per bottle and then sold for...

Joint cost allocation Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions are produced jointly in a mixing process that costs a total of $250 per batch. At the split-off point, one batch produces 80, 40, and 25 bottles of hand, body, and foot lotion, respectively. After the split-off point, hand lotion is sold immediately for $2.50 per bottle. Body lotion is processed further at an additional cost of $0.25 per bottle and then sold for...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch....

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

5. Joint Cost Allocation—Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and...

5. Joint Cost Allocation—Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch....

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation—Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch....

Joint Cost Allocation—Net Realizable Value Method

Nature's Garden Inc. produces wood chips, wood pulp, and mulch.

These products are produced through harvesting trees and sending

the logs through a wood chipper machine. One batch of logs produces

20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and

9,024 cubic yards of wood pulp. The joint production process costs

a total of $32,000 per batch. After the split-off point, wood chips

are immediately sold for $25 per cubic yard...

Joint Cost Allocation—Net Realizable Value Method

Nature's Garden Inc. produces wood chips, wood pulp, and mulch.

These products are produced through harvesting trees and sending

the logs through a wood chipper machine. One batch of logs produces

20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and

9,024 cubic yards of wood pulp. The joint production process costs

a total of $32,000 per batch. After the split-off point, wood chips

are immediately sold for $25 per cubic yard...

Joint Cost Allocation—Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar,...

Joint Cost Allocation—Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation—Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar,...

Joint Cost Allocation—Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation-Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar,...

Joint Cost Allocation-Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation-Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation—Net Realizable Value Method Lily’s Lemonade Stand makes three types of lemonade: pure, raspberry,...

Joint Cost Allocation—Net Realizable Value Method Lily’s Lemonade Stand makes three types of lemonade: pure, raspberry, and strawberry. The lemonade is produced through a joint mixing process that costs a total of $30 per batch. One batch produces 32 cups of pure lemonade, 21 cups of strawberry lemonade, and 21 cups of raspberry lemonade. After the split-off point, all three lemonades can be sold for $0.80 per cup, but strawberry and raspberry lemonade can be processed further by adding artificial...

Joint Cost Allocation—Net Realizable Value Method Lily’s Lemonade Stand makes three types of lemonade: pure, raspberry,...

Joint Cost Allocation—Net Realizable Value Method

Lily’s Lemonade Stand makes three types of lemonade: pure,

raspberry, and strawberry. The lemonade is produced through a joint

mixing process that costs a total of $30 per batch. One batch

produces 32 cups of pure lemonade, 21 cups of strawberry lemonade,

and 21 cups of raspberry lemonade. After the split-off point, all

three lemonades can be sold for $0.80 per cup, but strawberry and

raspberry lemonade can be processed further by adding artificial...

Joint Cost Allocation—Net Realizable Value Method

Lily’s Lemonade Stand makes three types of lemonade: pure,

raspberry, and strawberry. The lemonade is produced through a joint

mixing process that costs a total of $30 per batch. One batch

produces 32 cups of pure lemonade, 21 cups of strawberry lemonade,

and 21 cups of raspberry lemonade. After the split-off point, all

three lemonades can be sold for $0.80 per cup, but strawberry and

raspberry lemonade can be processed further by adding artificial...

Joint cost allocation Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions are produced jointly in a mixing process that costs a total of $250 per batch. At the split-off point, one batch produces 80, 40, and 25 bottles of hand, body, and foot lotion, respectively. After the split-off point, hand lotion is sold immediately for $2.50 per bottle. Body lotion is processed further at an additional cost of $0.25 per bottle and then sold for...

Joint cost allocation Lovely Lotion Inc. produces three different lotions: hand, body, and foot. The lotions are produced jointly in a mixing process that costs a total of $250 per batch. At the split-off point, one batch produces 80, 40, and 25 bottles of hand, body, and foot lotion, respectively. After the split-off point, hand lotion is sold immediately for $2.50 per bottle. Body lotion is processed further at an additional cost of $0.25 per bottle and then sold for...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Net Realizable Value Method Nature's Garden Inc. produces wood chips, wood pulp, and mulch. These products are produced through harvesting trees and sending the logs through a wood chipper machine. One batch of logs produces 20,304 cubic yards of wood chips, 14,100 cubic yards of mulch, and 9,024 cubic yards of wood pulp. The joint production process costs a total of $32,000 per batch. After the split-off point, wood chips are immediately sold for $25 per cubic yard...

Joint Cost Allocation-Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation-Market Value at Split-off Method Sugar Sweetheart, Inc., jointly produces raw sugar, granulated sugar, and caster sugar. After the split-off point, raw sugar is immediately sold for $0.20 per pound, while granulated and caster sugar are processed further. The market value of the granulated sugar and caster sugar is estimated to both be $0.25 at the split-off point. One batch of joint production costs $1,640 and yields 3,000 pounds of raw sugar, 3,600 pounds of granulated sugar, and...

Joint Cost Allocation—Net Realizable Value Method

Lily’s Lemonade Stand makes three types of lemonade: pure,

raspberry, and strawberry. The lemonade is produced through a joint

mixing process that costs a total of $30 per batch. One batch

produces 32 cups of pure lemonade, 21 cups of strawberry lemonade,

and 21 cups of raspberry lemonade. After the split-off point, all

three lemonades can be sold for $0.80 per cup, but strawberry and

raspberry lemonade can be processed further by adding artificial...

Joint Cost Allocation—Net Realizable Value Method

Lily’s Lemonade Stand makes three types of lemonade: pure,

raspberry, and strawberry. The lemonade is produced through a joint

mixing process that costs a total of $30 per batch. One batch

produces 32 cups of pure lemonade, 21 cups of strawberry lemonade,

and 21 cups of raspberry lemonade. After the split-off point, all

three lemonades can be sold for $0.80 per cup, but strawberry and

raspberry lemonade can be processed further by adding artificial...

Most questions answered within 3 hours.

-

A χ2-curve, looking at the relationship between age and hours

spent working at an office per...

asked 11 minutes ago -

The pH of a sample of water from a river is 5.0. A

sample of effluent from...

asked 56 minutes ago -

At the beginning of the period, the Fabricating Department

budgeted direct labor of $136,500 and equipment...

asked 1 hour ago -

Please answer all

____ 28. Rent control is usually

justified on the grounds that it protects...

asked 1 hour ago -

PARTS A-D HAVE BEEN ANSWERED. WAS TOLD TO REPOST. ONLY ANSWER

PARTS E and F.

A...

asked 1 hour ago -

2) You are given the task of finding a representation for a

circle in a drawing...

asked 2 hours ago -

STUDY QUESTION: Does use of diet drug fen-phen

(fenfluramine-phentermine) cause valvular heart disease?

HINT: Valvular heart...

asked 2 hours ago -

1. An object weighing 40 N rests on a surface. The coefficient

of friction is 0.35....

asked 3 hours ago -

Investor company owns 35% of investee company voting stock and

accounts for the investment under the...

asked 5 hours ago -

The number of major faults on a randomly chosen 1 km stretch of

highway has a...

asked 5 hours ago -

Consider the competitive environment of Starbuck's, Progressive

Insurance, a manufacturing firm with low turnover, or a...

asked 6 hours ago -

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 8 hours ago