Homework Answers

Solution is as follows:

Add Answer to:

(8-3) Black-Scholes Model INTERMEDIATE PROBLEMS 3-4 Assume that you have been given the following information on...

Check My Work еВook Problem Walk-Through Black-Scholes Model Assume that you have been given the following...

Check My Work еВook Problem Walk-Through Black-Scholes Model Assume that you have been given the following information on Purcell Industries call options: Strike price of option $12 Current stock price $13 Time to maturity of option 6 months Risk-free rate 6% Variance of stock return = 0.14 1 0.54821 N(di) 0.70823 d2 0.28363 N(d2) 0.61165 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use...

Check My Work еВook Problem Walk-Through Black-Scholes Model Assume that you have been given the following information on Purcell Industries call options: Strike price of option $12 Current stock price $13 Time to maturity of option 6 months Risk-free rate 6% Variance of stock return = 0.14 1 0.54821 N(di) 0.70823 d2 0.28363 N(d2) 0.61165 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use...

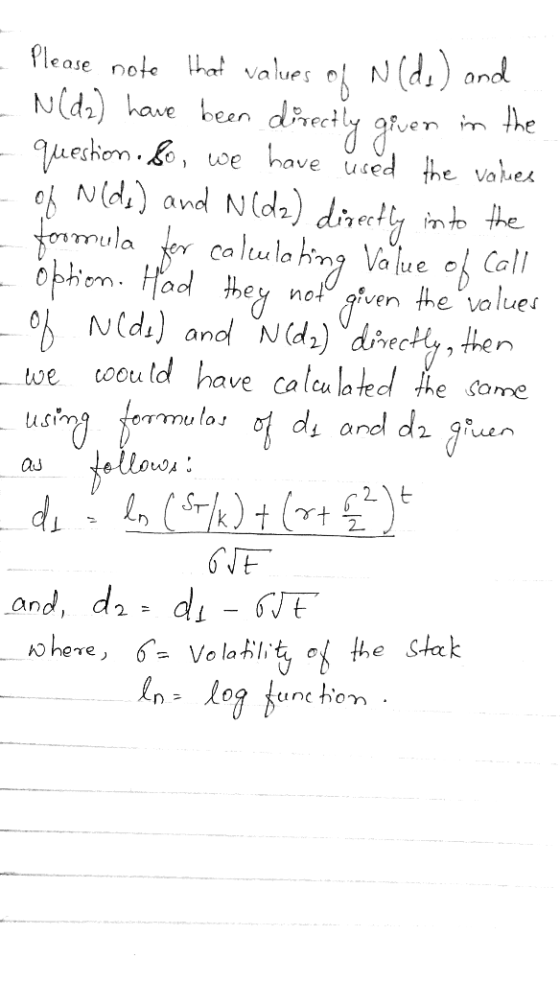

Assume that you have been given the following information on Purcell Industries' call options: Current stock...

Assume that you have been given the following information on Purcell Industries' call options: Current stock price = $15 Strike price of option = $14 Time to maturity of option = 9 months Risk-free rate = 8% Variance of stock return = 0.13 d1 = 0.56923 N(d1) = 0.71540 d2 = 0.25698 N(d2) = 0.60140 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use...

1. What is the value of the following call option according to the Black Scholes Option...

1. What is the value of the following call option according to the Black Scholes Option Pricing Model? What is the value of the put options? Stock Price = $42.50 Strike Price = $45.00 Time to Expiration = 3 Months = 0.25 years. Risk-Free Rate = 3.0%. Stock Return Standard Deviation = 0.45.

Please show every math step. An analyst is interested in using the Black-Scholes model to value...

Please show every math step.

An analyst is interested in using the Black-Scholes model to value call options on the stock of Ledbetter Inc. The analyst has accumulated the following information: . The price of the stock is $40 The strike price is $40. . The option matures in 3 months (t 0.25) The standard deviation of the stock's returns is 0.40 and the variance is 0.16. The risk-free rate is 12 percent. Using the Black-Scholes model, what is the...

Please show every math step.

An analyst is interested in using the Black-Scholes model to value call options on the stock of Ledbetter Inc. The analyst has accumulated the following information: . The price of the stock is $40 The strike price is $40. . The option matures in 3 months (t 0.25) The standard deviation of the stock's returns is 0.40 and the variance is 0.16. The risk-free rate is 12 percent. Using the Black-Scholes model, what is the...

Black Scholes Option Pricing Model Stock Price = 75 Strike price = 70 Risk Free rate...

Black Scholes Option Pricing Model Stock Price = 75 Strike price = 70 Risk Free rate - 4% Standard deviation = 15% 5 months remaining Calculate call & Put and show work please

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Use the Black-Scholes model to find the price for a call option with the following inputs:...

Use the Black-Scholes model to find the price for a call option with the following inputs: (1) current stock price is $30, (2) strike price is $37, (3) time to expiration is 6 months, (4) annualized risk-free rate is 6%, and (5) variance of stock return is 0.36. Do not round intermediate calculations. Round your answer to the nearest cent.

Use the Black-Scholes model to find the price for a call option with the following inputs:...

Use the Black-Scholes model to find the price for a call option with the following inputs: (1) current stock price is $31, (2) strike price is $34, (3) time to expiration is 8 months, (4) annualized risk-free rate is 5%, and (5) variance of stock return is 0.36. Do not round intermediate calculations. Round your answer to the nearest cent.

Problem 21-12 Black–Scholes model Use the Black–Scholes formula to value the following options: a. A call...

Problem 21-12 Black–Scholes model Use the Black–Scholes formula to value the following options: a. A call option written on a stock selling for $68 per share with a $68 exercise price. The stock's standard deviation is 6% per month. The option matures in three months. The risk-free interest rate is 1.75% per month. (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. A put option written on the same stock at the same time, with the...

To compute the value of a put using the Black-Scholes option pricing model, you: A) subtract...

To compute the value of a put using the Black-Scholes option pricing model, you: A) subtract the value of an equivalent call from 1.0. B) have to compute the value of the put as if it is a call and then apply the put-call parity formula. C) subtract the value of an equivalent call from the market price of the stock. D) assume the equivalent call is worthless and then apply the put-call parity formula. E) multiply the value of...

To compute the value of a put using the Black-Scholes option pricing model, you: A) subtract the value of an equivalent call from 1.0. B) have to compute the value of the put as if it is a call and then apply the put-call parity formula. C) subtract the value of an equivalent call from the market price of the stock. D) assume the equivalent call is worthless and then apply the put-call parity formula. E) multiply the value of...

Check My Work еВook Problem Walk-Through Black-Scholes Model Assume that you have been given the following information on Purcell Industries call options: Strike price of option $12 Current stock price $13 Time to maturity of option 6 months Risk-free rate 6% Variance of stock return = 0.14 1 0.54821 N(di) 0.70823 d2 0.28363 N(d2) 0.61165 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use...

Check My Work еВook Problem Walk-Through Black-Scholes Model Assume that you have been given the following information on Purcell Industries call options: Strike price of option $12 Current stock price $13 Time to maturity of option 6 months Risk-free rate 6% Variance of stock return = 0.14 1 0.54821 N(di) 0.70823 d2 0.28363 N(d2) 0.61165 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use...

Please show every math step.

An analyst is interested in using the Black-Scholes model to value call options on the stock of Ledbetter Inc. The analyst has accumulated the following information: . The price of the stock is $40 The strike price is $40. . The option matures in 3 months (t 0.25) The standard deviation of the stock's returns is 0.40 and the variance is 0.16. The risk-free rate is 12 percent. Using the Black-Scholes model, what is the...

Please show every math step.

An analyst is interested in using the Black-Scholes model to value call options on the stock of Ledbetter Inc. The analyst has accumulated the following information: . The price of the stock is $40 The strike price is $40. . The option matures in 3 months (t 0.25) The standard deviation of the stock's returns is 0.40 and the variance is 0.16. The risk-free rate is 12 percent. Using the Black-Scholes model, what is the...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

To compute the value of a put using the Black-Scholes option pricing model, you: A) subtract the value of an equivalent call from 1.0. B) have to compute the value of the put as if it is a call and then apply the put-call parity formula. C) subtract the value of an equivalent call from the market price of the stock. D) assume the equivalent call is worthless and then apply the put-call parity formula. E) multiply the value of...

To compute the value of a put using the Black-Scholes option pricing model, you: A) subtract the value of an equivalent call from 1.0. B) have to compute the value of the put as if it is a call and then apply the put-call parity formula. C) subtract the value of an equivalent call from the market price of the stock. D) assume the equivalent call is worthless and then apply the put-call parity formula. E) multiply the value of...

Most questions answered within 3 hours.

-

Given input { 66, 28, 43, 29, 44, 69, 19 } and a hash function

h(x)...

asked 9 minutes ago -

A pebble with mass m is thrown straight up with an initial speed

v0 so that...

asked 13 minutes ago -

Let X be a discrete random variable that follows a

binomial distribution with n = 11...

asked 21 minutes ago -

The equilibrium constant, K, for the following reaction is

1.29×10-2 at 600

K.

COCl2(g) --->

CO(g)...

asked 34 minutes ago -

It is known that 72% of people have a favorable opinion of their

local police force....

asked 37 minutes ago -

A vertical straight wire carrying an upward 26-A current exerts

an attractive force per unit length...

asked 50 minutes ago -

For the purposes of this assignment, you are to choose an

adaptive trait common to more...

asked 58 minutes ago -

Two identical flutes can play middle C (262 Hz) at 20◦C. How

many beats per second...

asked 1 hour ago -

Potassium phosphate and calcium chloride react in a double

replacement reaction. To produce 1.0 moles of...

asked 1 hour ago -

Sparky, Co. purchased land as a factory site for $600,000.

Sparky paid $42,000 to tear down...

asked 1 hour ago -

A Chi-square distribution with 14 degrees of freedom is a

correct model for

Question 8 options:...

asked 1 hour ago -

In a group of 45 mice, there are 10 that have a certain genetic

character. suppose...

asked 1 hour ago