Debt & Bonds

1. The table below presents the spot rates an investor faces.

| Year | Spot Rate |

|---|---|

| 1 | 2% |

| 2 | 3% |

| 3 | 4% |

| 4 | 5% |

Assume that, for each maturity, there is a zero-coupon bond traded in the market. These zeros pay $1,000 at their respective maturity.

a. Is the term structure positive, inverted, or flat?

b. What is the forward rate from t=1 to t=2?

c. Suppose that the investor is expecting to receive $1 million at t=1. This is a future cash inflow. He is planning to do the following investment strategy for this future cash inflow. He will borrow $980392.16 (this is $1 million / (1+2%)) now, and use this borrowing to buy a two-year zero. At t=1, the one-year zero matures, and he will make the payment to the one-year zero lenders. At t=2, the two-year zero matures, and he will receive the payment from the two-year zero. Fill the below cash flow table (the unit is $1 million).

| t=0 | t=1 | t=2 | |

|---|---|---|---|

| One-year zero |

|

||

| Two-year zero |

|

||

|

Others (The $1 million that the investor is expecting to receive at t=1) |

0 | 1 | 0 |

| Total | 0 |

d. What is the net return that this investor will get from his $1 million future cash flow from t=1 to t=2? Compare it with the forward and comment on what you find.

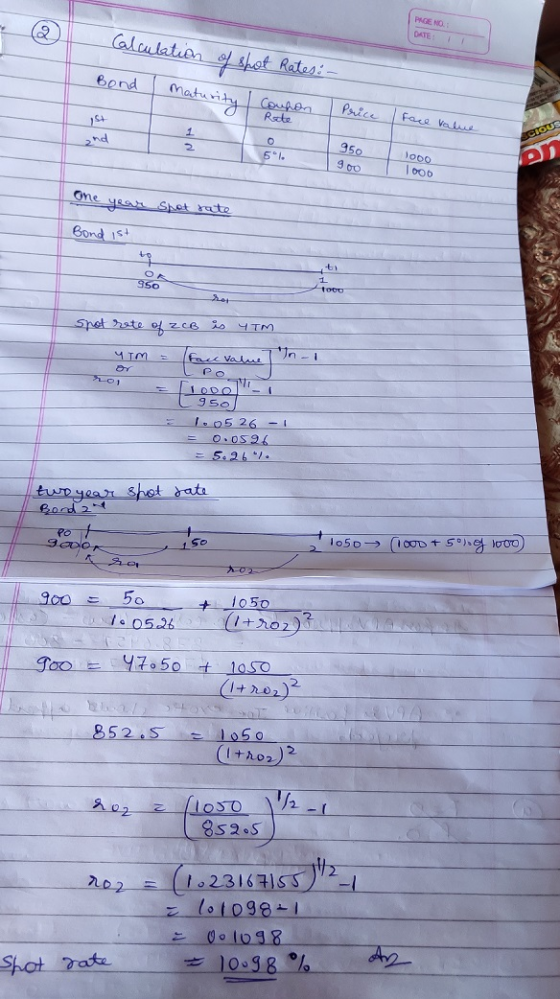

2. Suppose that we have two Treasury securities traded in the market, and we need to use them to calculate the theoretical spot rates. The first Treasury is a one-year zero, which pays $1,000 at t=1, and the current price is $950. The second Treasury is a two-year maturity, 5% coupon bond, and its current price is $900. The par value of the second Treasury is $1,000. Calculate the one-year spot rate and two-year spot rate, assuming that coupon payments are annual.

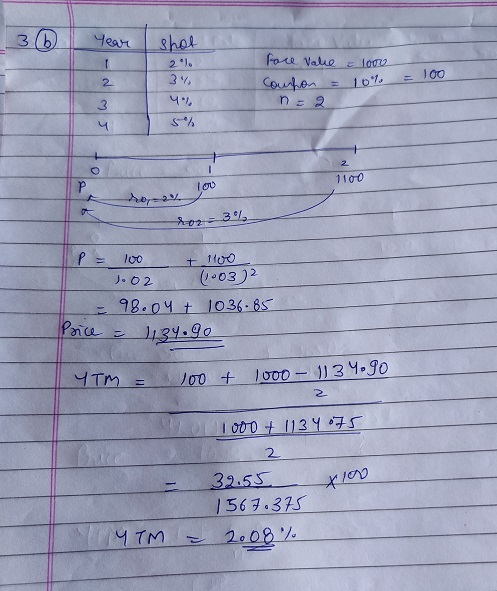

3. The table below presents the spot rates an investor faces.

| Year | Spot Rate |

|---|---|

| 1 | 2% |

| 2 | 3% |

| 3 | 4% |

| 4 | 5% |

a. What is the price of a two-year maturity 5% annual coupon bond? Par value is $1,000. What is its YTM?

b. What is the price of a two-year maturity 10% annual coupon bond? Par value is $1,000. What is its YTM?

Homework Answers

1 (a)

1 (b)

1(c)

2

3(a)

3(b)

Add Answer to:

Debt & Bonds

1. The table below presents the spot rates an investor

faces.

Year

Spot...

A. An investor purchased the following five bonds. Each bond had a par value of $1,000...

A. An investor purchased the following five bonds. Each bond had a par value of $1,000 and a 9% yield to maturity on the purchase day. Immediately after the investor purchased them, interest rates fell, and each then had a new YTM of 5%. What is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Enter all amounts as positive numbers. Do not round intermediate calculations. Round your monetary answers...

1-Concordant Inc. wants to raise $50 million by issuing 10-year zero-coupon bonds with a yield to...

1-Concordant Inc. wants to raise $50 million by issuing 10-year zero-coupon bonds with a yield to maturity (EAR) of 7.6%. What should be the total face value of the bonds (in $ million)? 2- Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate (EAR) 2.1% 2.8% 3% 4.5% What is the price of a risk-free zero-coupon bond with 3 years to maturity and a face value of $1,000 (in $)?

Given the following zero-coupon yield curve, what would a rational investor pay for an 8% coupon, $1,000 par security p...

Given the following zero-coupon yield curve, what would a rational investor pay for an 8% coupon, $1,000 par security paying coupons annually that matures in 5 years? What is this bond's YTM? Spot rate 00 ori of 2 Rate 9% 8% 6.50% 6% 4% or3 015 These rates are annualized rates for the period now (t=0) to the right subscript. Note I almost always put one of these on the exam. Do not be surprised.

Given the following zero-coupon yield curve, what would a rational investor pay for an 8% coupon, $1,000 par security paying coupons annually that matures in 5 years? What is this bond's YTM? Spot rate 00 ori of 2 Rate 9% 8% 6.50% 6% 4% or3 015 These rates are annualized rates for the period now (t=0) to the right subscript. Note I almost always put one of these on the exam. Do not be surprised.

Intro Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate...

Intro Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate (EAR) 2% 2.8% 3.1% 4.5% Part 1 To Attempt 1/10 for 10 pts. What is the price of a risk-free zero-coupon bond with 3 years to maturity and a face value of $1,000 (in $)? b+ decimals Submit

Intro Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate (EAR) 2% 2.8% 3.1% 4.5% Part 1 To Attempt 1/10 for 10 pts. What is the price of a risk-free zero-coupon bond with 3 years to maturity and a face value of $1,000 (in $)? b+ decimals Submit

5. The following are current prices of zero coupon bonds: (assume par values are all $1,000)...

5. The following are current prices of zero coupon bonds: (assume par values are all $1,000) Maturity (years) | Price 943.40$ 881.60$ 824.10$ 767.77$ 3 4 What is the YTM of the 3-year zero-coupon bond? a. b. What is the zero yield curve out to 4 years? (i.e. spot rates for 1, 2, 3 and 4 years) What is the 1-year forward rate in the third year (i.e. in two years' time)? C. d. According to the Expectations Hypothesis, what...

5. The following are current prices of zero coupon bonds: (assume par values are all $1,000) Maturity (years) | Price 943.40$ 881.60$ 824.10$ 767.77$ 3 4 What is the YTM of the 3-year zero-coupon bond? a. b. What is the zero yield curve out to 4 years? (i.e. spot rates for 1, 2, 3 and 4 years) What is the 1-year forward rate in the third year (i.e. in two years' time)? C. d. According to the Expectations Hypothesis, what...

Question 9. [19 points) PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year...

Question 9. [19 points) PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 8.0% 8.5% 9.0% 9.5% 4 a. What is the equilibrium price of a 4-year, 9% coupon bond paying a principal of $100 at maturity and coupons annually? Question 9. [19 points] PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 4 8.0% 8.5%...

Question 9. [19 points) PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 8.0% 8.5% 9.0% 9.5% 4 a. What is the equilibrium price of a 4-year, 9% coupon bond paying a principal of $100 at maturity and coupons annually? Question 9. [19 points] PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 4 8.0% 8.5%...

6. Spot rates of interest for zero-coupon Government of Canada bonds are observed for different terms...

6. Spot rates of interest for zero-coupon Government of Canada bonds are observed for different terms to maturity as follows: 1-year spot rate 4% 2-year spot rate 4.5% 3-year spot rate 5% A 3-year bond has a face value of $1,000 and a coupon rate of 7%. It pays coupons annually. What is its value today? (3 marks)

You are given the following benchmark spot rates: Maturity Spot Rate 1 2.90% 2 3.20% 3...

You are given the following benchmark spot rates: Maturity Spot Rate 1 2.90% 2 3.20% 3 3.60% 4 4.20% a) Compute the forward rate between years 1 and 2. b) Compute the forward rate between years 1 and 3. c) What is the zero price today of a five-year zero-coupon bond if the forward price for a one-year zero-coupon bond beginning in four years is known to be 0.9461 d) Calculate the price of a 4% annual coupon corporate bond...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 10% yield to maturity on the purchase day. Immediately after the investor purchased them, interest rates fell, and each then had a new YTM of 7%. What is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Round your answers to the nearest cent or to two decimal places. Enter...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 10% yield to maturity on the purchase day. Immediately after the investor purchased them interest rates fell and each then had a new YTM of 7%, what is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Round your answers to the nearest cent or to two decimal places. Enter...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 10% yield to maturity on the purchase day. Immediately after the investor purchased them interest rates fell and each then had a new YTM of 7%, what is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Round your answers to the nearest cent or to two decimal places. Enter...

Given the following zero-coupon yield curve, what would a rational investor pay for an 8% coupon, $1,000 par security paying coupons annually that matures in 5 years? What is this bond's YTM? Spot rate 00 ori of 2 Rate 9% 8% 6.50% 6% 4% or3 015 These rates are annualized rates for the period now (t=0) to the right subscript. Note I almost always put one of these on the exam. Do not be surprised.

Given the following zero-coupon yield curve, what would a rational investor pay for an 8% coupon, $1,000 par security paying coupons annually that matures in 5 years? What is this bond's YTM? Spot rate 00 ori of 2 Rate 9% 8% 6.50% 6% 4% or3 015 These rates are annualized rates for the period now (t=0) to the right subscript. Note I almost always put one of these on the exam. Do not be surprised.

Intro Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate (EAR) 2% 2.8% 3.1% 4.5% Part 1 To Attempt 1/10 for 10 pts. What is the price of a risk-free zero-coupon bond with 3 years to maturity and a face value of $1,000 (in $)? b+ decimals Submit

Intro Treasury spot interest rates are as follows: Maturity (years) 1 2 3 4 Spot rate (EAR) 2% 2.8% 3.1% 4.5% Part 1 To Attempt 1/10 for 10 pts. What is the price of a risk-free zero-coupon bond with 3 years to maturity and a face value of $1,000 (in $)? b+ decimals Submit

5. The following are current prices of zero coupon bonds: (assume par values are all $1,000) Maturity (years) | Price 943.40$ 881.60$ 824.10$ 767.77$ 3 4 What is the YTM of the 3-year zero-coupon bond? a. b. What is the zero yield curve out to 4 years? (i.e. spot rates for 1, 2, 3 and 4 years) What is the 1-year forward rate in the third year (i.e. in two years' time)? C. d. According to the Expectations Hypothesis, what...

5. The following are current prices of zero coupon bonds: (assume par values are all $1,000) Maturity (years) | Price 943.40$ 881.60$ 824.10$ 767.77$ 3 4 What is the YTM of the 3-year zero-coupon bond? a. b. What is the zero yield curve out to 4 years? (i.e. spot rates for 1, 2, 3 and 4 years) What is the 1-year forward rate in the third year (i.e. in two years' time)? C. d. According to the Expectations Hypothesis, what...

Question 9. [19 points) PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 8.0% 8.5% 9.0% 9.5% 4 a. What is the equilibrium price of a 4-year, 9% coupon bond paying a principal of $100 at maturity and coupons annually? Question 9. [19 points] PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 4 8.0% 8.5%...

Question 9. [19 points) PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 8.0% 8.5% 9.0% 9.5% 4 a. What is the equilibrium price of a 4-year, 9% coupon bond paying a principal of $100 at maturity and coupons annually? Question 9. [19 points] PART A. Consider the following spot rates on 1-year zero-coupon bonds: Year Spot Rates (or Yields to Maturity) 1 2 3 4 8.0% 8.5%...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 10% yield to maturity on the purchase day. Immediately after the investor purchased them interest rates fell and each then had a new YTM of 7%, what is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Round your answers to the nearest cent or to two decimal places. Enter...

INTEREST RATE SENSITIVITY An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 10% yield to maturity on the purchase day. Immediately after the investor purchased them interest rates fell and each then had a new YTM of 7%, what is the percentage change in price for each bond after the decline in interest rates? Fill in the following table. Round your answers to the nearest cent or to two decimal places. Enter...

Most questions answered within 3 hours.

-

One question on a survey asked whether people believe in hell.

Of the possible responses, 484...

asked 18 minutes ago -

An electromagnetic wave can pass through which one of these:

a. Glass b.Iron c.

Water d....

asked 34 minutes ago -

pls review carefully and help pls

In perfect competition in long-run equilibrium, can consumer

surplus or...

asked 33 minutes ago -

What information can be presented as evidence during arbitration

proceedings?

asked 27 minutes ago -

Calculate the ratio of the resistance of 15.0 m m of aluminum

wire 2.4 mm m...

asked 36 minutes ago -

The US Census Bureau needs to estimate the median income of

females in the US, so...

asked 37 minutes ago -

in a region where a constant electric field is maintained, a

proton and an electron are...

asked 47 minutes ago -

Simple Advice to a Chief Executive

This activity requires you to advise a business’s Chief

Executive...

asked 52 minutes ago -

Calculate the mass of camphor C10H16O that contains a billion

(1.000x10^9) carbon atoms.

.

asked 55 minutes ago -

In a poll of 504 human resource professionals, 46.4% said that

body piercings and tattoos were...

asked 1 hour ago -

4. what is group think? does group think bring positive or

negative result? please justify your...

asked 1 hour ago -

describe conditions and outcomes of boiling

pasteurization and surfacing. which of these treatment can be

considered...

asked 1 hour ago