suppose that 0 interest rates with continuous compounding are as follows. calculate forward interest rates for...

suppose that 0 interest rates with continuous compounding are as follows. calculate forward interest rates for the second third and fourth quarters.

month zero rate for an n month investment(%per year)

3 3.0

6 3.2

9 3.4

12 3.5

Homework Answers

Detailed solution is shown below ask if any doubt

Add Answer to:

suppose that 0 interest rates with continuous compounding are as

follows. calculate forward interest rates for...

Suppose that zero interest rates are per annum with continuous compounding are as follows: Maturity (years)...

Suppose that zero interest rates are per annum with continuous compounding are as follows: Maturity (years) Rate (% per annum) (1, 2.5) (2, 3.0) (3, 3.5) (4, 4.2) (5, 4.7) Calculate 1-year forward interest rates for the second (f1,2), third (f2,3), fourth (f3,4), and fifth (f4,5) years. Use the rates in the previous part to value an FRA today as the borrower with 5% per annum for the third year on $1 million. (FRA is for the year starting at...

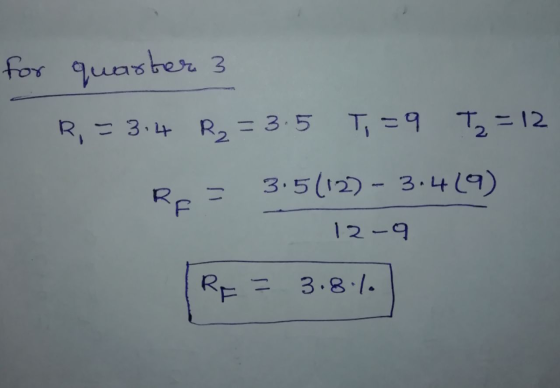

Suppose that zero interest rates with continuous compounding are as follows: Maturity (months) 34 62 94...

Suppose that zero interest rates with continuous compounding are as follows: Maturity (months) 34 62 94 Rate % per annum) 3.02 3.22 3.42 3.5e 3.62 3.72 12e 152 18 Calculate forward interest rates for the second, third, fourth, fifth, and sixth quarters.

Suppose that zero interest rates with continuous compounding are as follows: Maturity (months) 34 62 94 Rate % per annum) 3.02 3.22 3.42 3.5e 3.62 3.72 12e 152 18 Calculate forward interest rates for the second, third, fourth, fifth, and sixth quarters.

2. Suppose that zero interest rates with quarterly compounding are as follows: Maturity (months) Rate(%) 3...

2. Suppose that zero interest rates with quarterly compounding are as follows: Maturity (months) Rate(%) 3 8.0 6 8.4 9 8.8 12 9.0 i. Calculate the forward interest rates for the second, third, and fourth quarters. ii. You should have found that the forward rate over the fourth quarter is 9.6006%. Carefully explain the available arbitrage strategy and calculate your profit) if you found a bank willing to lend to you forward at 9.0000% over the fourth quarter.

2. Suppose that zero interest rates with quarterly compounding are as follows: Maturity (months) Rate(%) 3 8.0 6 8.4 9 8.8 12 9.0 i. Calculate the forward interest rates for the second, third, and fourth quarters. ii. You should have found that the forward rate over the fourth quarter is 9.6006%. Carefully explain the available arbitrage strategy and calculate your profit) if you found a bank willing to lend to you forward at 9.0000% over the fourth quarter.

Exercise 2. The 6-month, 12-month. I 8-month, and 24-month zero rates are 4%, 4.5%, 4.75% and 5%, with continuous compounding (a) What are the rates with semi-annual compounding? (c) Forward rates ar...

Exercise 2. The 6-month, 12-month. I 8-month, and 24-month zero rates are 4%, 4.5%, 4.75% and 5%, with continuous compounding (a) What are the rates with semi-annual compounding? (c) Forward rates are rates of interest implied by current zero rates for periods of time in the future. Calculate the forward rate for year 2, i.e. the rate for the period of time between the end of 12-month and the end of 24-month. (d) Consider a 2-year bond providing semiannual coupon...

Exercise 2. The 6-month, 12-month. I 8-month, and 24-month zero rates are 4%, 4.5%, 4.75% and 5%, with continuous compounding (a) What are the rates with semi-annual compounding? (c) Forward rates are rates of interest implied by current zero rates for periods of time in the future. Calculate the forward rate for year 2, i.e. the rate for the period of time between the end of 12-month and the end of 24-month. (d) Consider a 2-year bond providing semiannual coupon...

Six-month LIBOR is 3.5%. LIBOR forward rates for the 6- to 12-month period and for the...

Six-month LIBOR is 3.5%. LIBOR forward rates for the 6- to 12-month period and for the 12- to 18-month period are both 3.7%. Swap rates for 2- and 3-year semiannual pay swaps are 3.6% and 3.8%, respectively. Estimate the LIBOR forward rates for maturities of 18-month to 2 years, 2 to 2.5 years, and 2.5 to 3 years. Assume that the 2.5-year swap rate is the average of the 2- and 3-year swap rates and that OIS zero rates for...

Six-month LIBOR is 3.5%. LIBOR forward rates for the 6- to 12-month period and for the 12- to 18-month period are both 3.7%. Swap rates for 2- and 3-year semiannual pay swaps are 3.6% and 3.8%, respectively. Estimate the LIBOR forward rates for maturities of 18-month to 2 years, 2 to 2.5 years, and 2.5 to 3 years. Assume that the 2.5-year swap rate is the average of the 2- and 3-year swap rates and that OIS zero rates for...

XYZ stock has a share price of $125 today. All rates of interest are 5% per year with continuous compounding. Finally, X...

XYZ stock has a share price of $125 today. All rates of interest are 5% per year with continuous compounding. Finally, XYZ is scheduled to pay the following dividends per share over the next year: a dividend of $3.0 per share in three months and a dividend of $3.0 per share in six months. Derive today’s forward price of the stock for delivery in nine months.

XYZ stock has a share price of $125 today. All rates of interest are 5% per year with continuous compounding. Finally, X...

XYZ stock has a share price of $125 today. All rates of interest are 5% per year with continuous compounding. Finally, XYZ is scheduled to pay the following dividends per share over the next year: a dividend of $3.0 per share in three months and a dividend of $3.0 per share in six months. Derive today’s forward price of the stock for delivery in nine months.

i need simple explain please 7) The zero rates for three, six, nine and twelve compounding....

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

Suppose that all investors expect that interest rates for the 4 years will be as follows:...

Suppose that all investors expect that interest rates for the 4 years will be as follows: Year Forward Interest Rate 0 (today) 5° 70 2 99 10° 3 What is the yield to maturity of a 3-year zero-coupon bond? A. 9.00% B. 6.99% c. 7.03% D. 7.49% O E. None of the options

Suppose that all investors expect that interest rates for the 4 years will be as follows: Year Forward Interest Rate 0 (today) 5° 70 2 99 10° 3 What is the yield to maturity of a 3-year zero-coupon bond? A. 9.00% B. 6.99% c. 7.03% D. 7.49% O E. None of the options

Suppose that the nominal annual interest rate on an investment is 12%. Calculate the effective interest...

Suppose that the nominal annual interest rate on an investment is 12%. Calculate the effective interest rate if compounding occurs continuously. Suppose that the nominal annual interest rate on an investment is 12% Calculate the effective interest rate if compounding occurs monthly.

Suppose that the nominal annual interest rate on an investment is 12%. Calculate the effective interest rate if compounding occurs continuously. Suppose that the nominal annual interest rate on an investment is 12% Calculate the effective interest rate if compounding occurs monthly.

Suppose that zero interest rates with continuous compounding are as follows: Maturity (months) 34 62 94 Rate % per annum) 3.02 3.22 3.42 3.5e 3.62 3.72 12e 152 18 Calculate forward interest rates for the second, third, fourth, fifth, and sixth quarters.

Suppose that zero interest rates with continuous compounding are as follows: Maturity (months) 34 62 94 Rate % per annum) 3.02 3.22 3.42 3.5e 3.62 3.72 12e 152 18 Calculate forward interest rates for the second, third, fourth, fifth, and sixth quarters.

2. Suppose that zero interest rates with quarterly compounding are as follows: Maturity (months) Rate(%) 3 8.0 6 8.4 9 8.8 12 9.0 i. Calculate the forward interest rates for the second, third, and fourth quarters. ii. You should have found that the forward rate over the fourth quarter is 9.6006%. Carefully explain the available arbitrage strategy and calculate your profit) if you found a bank willing to lend to you forward at 9.0000% over the fourth quarter.

2. Suppose that zero interest rates with quarterly compounding are as follows: Maturity (months) Rate(%) 3 8.0 6 8.4 9 8.8 12 9.0 i. Calculate the forward interest rates for the second, third, and fourth quarters. ii. You should have found that the forward rate over the fourth quarter is 9.6006%. Carefully explain the available arbitrage strategy and calculate your profit) if you found a bank willing to lend to you forward at 9.0000% over the fourth quarter.

Exercise 2. The 6-month, 12-month. I 8-month, and 24-month zero rates are 4%, 4.5%, 4.75% and 5%, with continuous compounding (a) What are the rates with semi-annual compounding? (c) Forward rates are rates of interest implied by current zero rates for periods of time in the future. Calculate the forward rate for year 2, i.e. the rate for the period of time between the end of 12-month and the end of 24-month. (d) Consider a 2-year bond providing semiannual coupon...

Exercise 2. The 6-month, 12-month. I 8-month, and 24-month zero rates are 4%, 4.5%, 4.75% and 5%, with continuous compounding (a) What are the rates with semi-annual compounding? (c) Forward rates are rates of interest implied by current zero rates for periods of time in the future. Calculate the forward rate for year 2, i.e. the rate for the period of time between the end of 12-month and the end of 24-month. (d) Consider a 2-year bond providing semiannual coupon...

Six-month LIBOR is 3.5%. LIBOR forward rates for the 6- to 12-month period and for the 12- to 18-month period are both 3.7%. Swap rates for 2- and 3-year semiannual pay swaps are 3.6% and 3.8%, respectively. Estimate the LIBOR forward rates for maturities of 18-month to 2 years, 2 to 2.5 years, and 2.5 to 3 years. Assume that the 2.5-year swap rate is the average of the 2- and 3-year swap rates and that OIS zero rates for...

Six-month LIBOR is 3.5%. LIBOR forward rates for the 6- to 12-month period and for the 12- to 18-month period are both 3.7%. Swap rates for 2- and 3-year semiannual pay swaps are 3.6% and 3.8%, respectively. Estimate the LIBOR forward rates for maturities of 18-month to 2 years, 2 to 2.5 years, and 2.5 to 3 years. Assume that the 2.5-year swap rate is the average of the 2- and 3-year swap rates and that OIS zero rates for...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

Suppose that all investors expect that interest rates for the 4 years will be as follows: Year Forward Interest Rate 0 (today) 5° 70 2 99 10° 3 What is the yield to maturity of a 3-year zero-coupon bond? A. 9.00% B. 6.99% c. 7.03% D. 7.49% O E. None of the options

Suppose that all investors expect that interest rates for the 4 years will be as follows: Year Forward Interest Rate 0 (today) 5° 70 2 99 10° 3 What is the yield to maturity of a 3-year zero-coupon bond? A. 9.00% B. 6.99% c. 7.03% D. 7.49% O E. None of the options

Suppose that the nominal annual interest rate on an investment is 12%. Calculate the effective interest rate if compounding occurs continuously. Suppose that the nominal annual interest rate on an investment is 12% Calculate the effective interest rate if compounding occurs monthly.

Suppose that the nominal annual interest rate on an investment is 12%. Calculate the effective interest rate if compounding occurs continuously. Suppose that the nominal annual interest rate on an investment is 12% Calculate the effective interest rate if compounding occurs monthly.

Most questions answered within 3 hours.

-

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 2 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 28 seconds ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 6 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 4 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 10 minutes ago -

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 32 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 33 minutes ago -

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 25 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 24 minutes ago -

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 47 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 43 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 47 minutes ago