3. Covered Interest Arbitrage. Assume the following information: Spot rate of Mexican peso = $ .100 1-year Forward...

3. Covered Interest Arbitrage. Assume the following information:

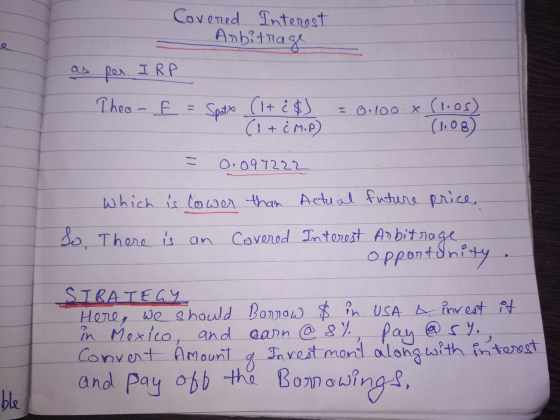

Spot rate of Mexican peso = $ .100

1-year Forward rate of Mexican peso = $ .098

Mexican interest rate = 8%

US. interest rate =5%

Show how to identify any arbitrage opportunity based on the Interest Rate Parity (IRP). What is your strategy to achieve your profit? What is your arbitrage profit per $1,000,000 (CIA) ?

Homework Answers

Add Answer to:

3. Covered Interest

Arbitrage. Assume the following

information:

Spot rate of Mexican peso = $ .100

1-year Forward...

Assume the following information: Spot rate of Mexican peso : $.100 180-day forward rate of Mexican...

Assume the following information: Spot rate of Mexican peso : $.100 180-day forward rate of Mexican peso : $.098 180-day Mexican interest rate : 6% 180-day U.S. interest rate : 5% a) What would be the return to a Mexican investor who has 1,000,000 Mexican pesos from using covered interest arbitrage? (i.e. the Mexican investor will convert the peso into U.S. dollar at the spot rate and invest it in the U.S. for 180 days, and simultaneously sell a U.S....

2. Assume the following information: Spot rate of Mexican peso : $.100 180-day forward rate of Mexican peso : $.098 180-...

2. Assume the following information: Spot rate of Mexican peso : $.100 180-day forward rate of Mexican peso : $.098 180-day Mexican interest rate : 6% 180-day U.S. interest rate : 5% a) What would be the return to a Mexican investor who has 1,000,000 Mexican pesos from using covered interest arbitrage? (i.e. the Mexican investor will convert the peso into U.S. dollar at the spot rate and invest it in the U.S. for 180 days, and simultaneously sell a...

spot rate of mexican peso: 0.1 180 day mexican interest rate: 6% 180 day US interest...

spot rate of mexican peso: 0.1 180 day mexican interest rate: 6% 180 day US interest rate: 5% 180 day forward rate of mexican peso: $0.098 a. US investor has $50,000 to invest. find the return from covered interest arbitage for the US investor b. Mexican investor 500,000 Mexican pesos to invest. find the return from covered interest arbitage for the Mexican investor c. realignment of covered interest arbitrage from the presceptive of the mexican investor:

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

(a)Assume that the one-year interest rate is 6% in New Zealand and 10% in the US. The spot rate o...

(a)Assume that the one-year interest rate is 6% in New Zealand and 10% in the US. The spot rate of the NZ$ is $0.50 while the forward rate is $0.54. Would covered interest arbitrage be feasible for a US investor who is willing to invest $1,000,000 to exploit the opportunity of differences in interest rates? If the investment is worthwhile, find the profit the investor could earn in a year. (b) Explain the realignment process that would eventually produce interest...

The spot EUR/USD is 1.12 and the forward rate is 1.1. The interest rate in France...

The spot EUR/USD is 1.12 and the forward rate is 1.1. The interest rate in France is 3% and 4% in the US. a) Does the iRP hold? b) If not, how could you make a CIA profit by using 1000 EUR? Show your work. c) What is the forward rate that would make CIA disappear?

KBL Inc. with $20m funds available is seeking covered interest arbitrage (CIA) in Denmark Spot Rate...

KBL Inc. with $20m funds available is seeking covered interest arbitrage (CIA) in Denmark Spot Rate = 6.15 (Kr/$) 3-month forward rate = 6.20 (Kr/S) 3-Month interest rate in US = 2.75% 3-month interest rate in Denmark = 3.25% The CIA profit potential is: Select one: a. -3.23% b. 0.81% c. -2.73% d. None of the Above e. 0.50%

KBL Inc. with $20m funds available is seeking covered interest arbitrage (CIA) in Denmark Spot Rate...

KBL Inc. with $20m funds available is seeking covered interest arbitrage (CIA) in Denmark Spot Rate = 6.15 (Kr/$) 3-month forward rate = 6.20 (Kr/S) 3-Month interest rate in US = 2.75% 3-month interest rate in Denmark = 3.25% The CIA profit potential is: Select one: a. -3.23% b. 0.81% c. -2.73% d. None of the Above e. 0.50%

1) Assume the interest rate is 4% in the UK and 8% in Australia. The forward...

1) Assume the interest rate is 4% in the UK and 8% in Australia. The forward GBP/AUD is 187 AUD. Compute the spot GBP/AUD that makes the IRP hold. Show your work . 2) The spot EUR/USD is 1.12 and the forward rate is 1.1. The interest rate in France is 3% and 4% in the US. a) Does the iRP hold? b) If not, how could you make a CIA profit by using 1000 EUR? Show your work. c)...

Currently, the spot exchange rate is $0.85/A$, and the one-year forward exchange rate is $0.81/A$. One-year...

Currently, the spot exchange rate is $0.85/A$, and the one-year forward exchange rate is $0.81/A$. One-year interest is 3.5% in the United States and 4.2% in Australia. You may borrow up to $1,000,000 or A$1,176,471, which is equivalent to $1,000,000 at the current spot rate. Determine if Interest Rate Parity (IRP) is holding between Australia and the United States. If IRP is not holding, explain in detail how you would realize certain profit in U.S. dollar terms. Explain how IRP...

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

Most questions answered within 3 hours.

-

Given the line notation, identify the anodic and

cathodic reactions and overall reaction:

Ag(s)| AgCl(s) |...

asked 15 minutes ago -

The money raised and spent (both in millions of dollars) by

all congressional campaigns for 8...

asked 18 minutes ago -

Annual salaries for employees in a large company are

approximately normally distributed with a mean of...

asked 27 minutes ago -

1. Lifetimes of a certain brand of lightbulbs is known to follow

a right-skewed distribution with...

asked 26 minutes ago -

The gravitational field

F(x,y,z) =cx /(x2 + y2 + z2)3/2 e1+ cy /(x2 + y2 +...

asked 25 minutes ago -

Below is an abstract from the following paper published in

Frontiers in Cell and Developmental Biology....

asked 27 minutes ago -

Company A is assigned $200,000 of goodwill arising from a recent

business combination. The current carrying...

asked 34 minutes ago -

Write any individual Class A IP address below. It cannot be

non-routable address. Include the subnet...

asked 35 minutes ago -

Coronado Industries had January 1 inventory of $301000 when it

adopted dollar-value LIFO. During the year,...

asked 44 minutes ago -

The cable supporting a 2145-kg elevator has a maximum strength

of 2.18×104 N.

a) What maximum...

asked 54 minutes ago -

Find the critical value(s) and rejection region(s) for a

two-tailed chi-square test with a sample size...

asked 58 minutes ago -

One of your experts gave me an answer of $7.36 but there are

many different answers...

asked 1 hour ago