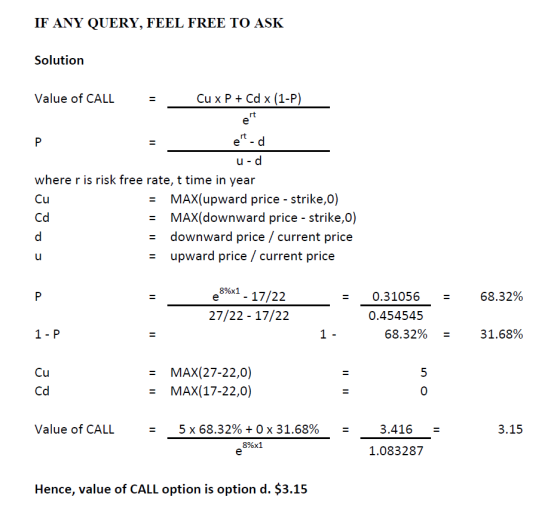

The current price of a stock is $22, and at the end of one year its...

The current price of a stock is $22, and at the end of one year

its price will be either $27 or $17. The annual risk free rate is

8.0%, based on daily compounding.

A 1-year call option on the stock with an exercise price of $22 is

available. Based on the binomial model what is the option's

value?

a. $3.55

b. $3.41

c. $3.23

d. $3.15

Homework Answers

Add Answer to:

The current price of a stock is $22, and at the end of one year

its...

Binomial option pricing model A stock currently trades for $41. In one month, the price will...

Binomial option pricing model A stock currently trades for $41. In one month, the price will either be $50 or $36. The annual risk-free rate is 6%; assume daily interest compounding, and 365 days per year. The value of a one-month call option with an exercise price of $39 is $______.

Binomial option pricing model A stock currently trades for $41. In one month, the price will either be $47 or $34. The a...

Binomial option pricing model A stock currently trades for $41. In one month, the price will either be $47 or $34. The annual risk-free rate is 6%; assume daily interest compounding and 365 days per year. The value of a one-month call option with an exercise price of $39 is $______.

The current price of a stock is $39.99. A one-year call option on the stock with...

The current price of a stock is $39.99. A one-year call option on the stock with a strike price of $38.83 has a current price of $6.02. The annual risk-free rate is 4%. Assume daily interest compounding. What is the current value of a one-year put option on the stock with the same exercise price?

Binomial Model The current price of a stock is $16. In 6 months, the price will...

Binomial Model The current price of a stock is $16. In 6 months, the price will be either $20 or $11. The annual risk-free rate is 5%. Find the price of a call option on the stock that has an strike price of $14 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations. $

eBook Problem 8-07 Binomial Model The current price of a stock is $16. In 6 months,...

eBook Problem 8-07 Binomial Model The current price of a stock is $16. In 6 months, the price will be either $20 or $12. The annual risk-free rate is 3%. Find the price of a call option on the stock that has an strike price of $15 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations

eBook Problem 8-07 Binomial Model The current price of a stock is $16. In 6 months, the price will be either $20 or $12. The annual risk-free rate is 3%. Find the price of a call option on the stock that has an strike price of $15 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations

1) The current price of a stock is $15. In 6 months, the price will be...

1) The current price of a stock is $15. In 6 months, the price will be either $18 or $13. The annual risk-free rate is 3%. Find the price of a call option on the stock that has a strike price of $14 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations. 2) The current price of a stock is $20. In...

The current price of Estelle Corporation stock is $ 23.00. In each of the next two...

The current price of Estelle Corporation stock is $ 23.00. In each of the next two years, this stock price will either go up by 16 % or go down by 16 %. The stock pays no dividends. The one-year risk-free interest rate is 8.0 % and will remain constant. Using the Binomial Model, calculate the price of a one-year call option on Estelle stock with a strike price of $ 23.00. The price of the one-year call option is...

The current price of Estelle Corporation stock is $ 23.00 In each of the next two...

The current price of Estelle Corporation stock is $ 23.00 In each of the next two years, this stock price will either go up by 18 % or go down by 18 %. The stock pays no dividends. The one-year risk-free interest rate is 8.0 % and will remain constant. Using the Binomial Model, calculate the price of a one-year call option on Estelle stock with a strike price of $ 23.00

The current price of Estelle Corporation stock is $25. Its stock price will either go up...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The Call option on the stock has a $13 exercise price and one-year maturity. The volatility...

The Call option on the stock has a $13 exercise price and one-year maturity. The volatility of the stock is 10%. The probability of an up or down movement is an equal 50%. The risk-free interest rate is 6% per annum The current stock price is $13. Stock movement is 2 times a year. Value the premium of the option based on Binomial Model.

The Call option on the stock has a $13 exercise price and one-year maturity. The volatility of the stock is 10%. The probability of an up or down movement is an equal 50%. The risk-free interest rate is 6% per annum The current stock price is $13. Stock movement is 2 times a year. Value the premium of the option based on Binomial Model.

eBook Problem 8-07 Binomial Model The current price of a stock is $16. In 6 months, the price will be either $20 or $12. The annual risk-free rate is 3%. Find the price of a call option on the stock that has an strike price of $15 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations

eBook Problem 8-07 Binomial Model The current price of a stock is $16. In 6 months, the price will be either $20 or $12. The annual risk-free rate is 3%. Find the price of a call option on the stock that has an strike price of $15 and that expires in 6 months. (Hint: Use daily compounding.) Round your answer to the nearest cent. Assume a 365-day year. Do not round your intermediate calculations

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The current price of Estelle Corporation stock is $25. Its stock price will either go up by 20% or go down by 20% in one year. The stock pays no dividends. The one-year risk-free interest rate is 6%. Using the binomial model, calculate the price of a one-year call option on Estelle stock with a strike price of $25. The price of a one-year call option on Estelle stock with a strike price of $25 is $ (Round to the...

The Call option on the stock has a $13 exercise price and one-year maturity. The volatility of the stock is 10%. The probability of an up or down movement is an equal 50%. The risk-free interest rate is 6% per annum The current stock price is $13. Stock movement is 2 times a year. Value the premium of the option based on Binomial Model.

The Call option on the stock has a $13 exercise price and one-year maturity. The volatility of the stock is 10%. The probability of an up or down movement is an equal 50%. The risk-free interest rate is 6% per annum The current stock price is $13. Stock movement is 2 times a year. Value the premium of the option based on Binomial Model.

Most questions answered within 3 hours.

-

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 32 minutes ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 33 minutes ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 39 minutes ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 52 minutes ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 55 minutes ago -

A 1.3 eV electron has a 10-4 probability of tunneling

through a 2.4 eV potential barrier....

asked 1 hour ago -

What is the one ingredient that is common to being successful

with all stakeholders?

profit

trust...

asked 1 hour ago -

Write an assembly language 32 bit program that reads in lines of

text by a .txt...

asked 1 hour ago -

what is the density ( in g/L) of hydrogen gas at 29 degrees C and a...

asked 1 hour ago -

5-6. You are considering three investment alternatives for some

spare cash: Old Reliable Corporation stock (A1),...

asked 1 hour ago -

Problem 16-02

Receivables Investment

Medwig Corporation has a DSO of 45 days. The company averages

$7,250...

asked 1 hour ago -

Mr. Brown hired Lowe's Maintenance Services Limited to repair

and paint the exterior wall of his...

asked 1 hour ago