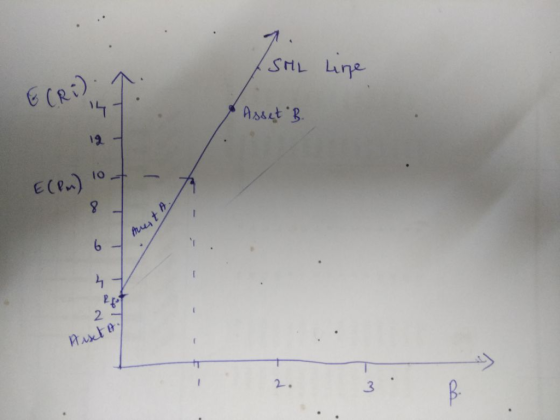

Homework Answers

a) The security Market Line is based on following CAPM equation

E(Ri)=Ri+  i* (E (Rm)-

Rf)

i* (E (Rm)-

Rf)

where E(Ri) is expected return of security , Rf is risk free

rate , i

security beta coefficient and E(Rm) is an expected market

return.

The slope of the SML is market risk premium. The Y intercept of SML Line is Beta cofficient.

b) Alpha  = E(Ri)-Ri-

(i* (E (Rm)-

Rf))

= E(Ri)-Ri-

(i* (E (Rm)-

Rf))

Alpha of Asset A = .021-.03- ((-.1)*(0.1-.03)

= -0.20%

Alpha of Asset B = 0.142- .03- ((1.6)*(0.1-.03)

= 0.00%

Alpha of Asset C = 0.06- .03- ((.4)*(0.1-.03)

= .20%

Asset A- Overpriced

Asset B - Fairly Priced

Asset C - Underpriced

Add Answer to:

Problem, 6· (20 points total) Assume that the risk-free rate is 3% and the expected rate...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

The expected return on the market portfolio is 15%. The risk-free rate is 8%. The expected...

The expected return on the market portfolio is 15%. The risk-free rate is 8%. The expected return on SDA Corp. common stock is 16%. The β of SDA Corp. common stock is 1.25. Within the context of the Capital Asset Pricing Model, is the common stock of SDA Corp. overpriced, underpriced or fairly priced?

The risk-free rate is 6% and the expected rate of return on the market portfolio is...

The risk-free rate is 6% and the expected rate of return on the market portfolio is 13%.

a. Calculate the required rate of return on a security with a beta of 1.25. (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.)

b. If the security is expected to return 16%, is it overpriced or underpriced?

The risk-free rate is 6% and the expected rate of return on the market portfolio is 13%.

a. Calculate the required rate of return on a security with a beta of 1.25. (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.)

b. If the security is expected to return 16%, is it overpriced or underpriced?

CAPM For a risky return r, CAPM equation is Er -r- B(E[rm] -r), where r is risk-free rate, Tm is ...

CAPM For a risky return r, CAPM equation is Er -r- B(E[rm] -r), where r is risk-free rate, Tm is market return, and is loading of risky return r on market return rm In what follows, X and Y denote arbitrary assets, B risk-free bond, M market portfolio. Determine which of the following scenarios are consistent or inconsistent with mean-variance efficiency (that is, CAPM). In your answer, write "Consistent" or "Inconsistent", and give brief explanation. 25% 12% 0.8 1.2 25...

CAPM For a risky return r, CAPM equation is Er -r- B(E[rm] -r), where r is risk-free rate, Tm is market return, and is loading of risky return r on market return rm In what follows, X and Y denote arbitrary assets, B risk-free bond, M market portfolio. Determine which of the following scenarios are consistent or inconsistent with mean-variance efficiency (that is, CAPM). In your answer, write "Consistent" or "Inconsistent", and give brief explanation. 25% 12% 0.8 1.2 25...

11. Assume that the Risk Free rate is 5% and the Expected Return on the market...

11. Assume that the Risk Free rate is 5% and the Expected Return on the market is 10%. Show if these stocks are under, over, or fairly valued. Illustrate it in a chart with the SML and the expected returns of the stocks. CAPM returnasseti RiskFree + [E(Rmarket)- Risk Free] Basset i Security САРМ Over/Under E(Return) Beta Return |Valued? Stock W Stock Y Stock Z 0.035 0.85 1.2 0.095 0.12 1.1 Show (and explain) your results in the following chart....

11. Assume that the Risk Free rate is 5% and the Expected Return on the market is 10%. Show if these stocks are under, over, or fairly valued. Illustrate it in a chart with the SML and the expected returns of the stocks. CAPM returnasseti RiskFree + [E(Rmarket)- Risk Free] Basset i Security САРМ Over/Under E(Return) Beta Return |Valued? Stock W Stock Y Stock Z 0.035 0.85 1.2 0.095 0.12 1.1 Show (and explain) your results in the following chart....

Security X has a rate of return of 13% and a beta of 1.15. The risk-free...

Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%. According to the capital asset pricing model, security X is 1) fairly priced 2) underpriced 3) overpriced 4) None of the answers are correct Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%....

Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%. According to the capital asset pricing model, security X is 1) fairly priced 2) underpriced 3) overpriced 4) None of the answers are correct Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%....

Problem 3 The risk-free rate is 2%, the market risk premium is 5%, and the size...

Problem 3 The risk-free rate is 2%, the market risk premium is 5%, and the size factor and value factor return are 2% and 3%. Below table shows the return characteristics of two stocks A and B: Stock Forecasted return (FR) BMKT BSMB BHML 9.60% 0.9 0.8 -0.5 4.80% 0.8 -0.2 0.4 a. [2pts) According to the Fama-French 3-factor model, what would be the fair return for each stock? b. 2pts Characterize each stock as underpriced, overpriced, or properly priced.

Problem 3 The risk-free rate is 2%, the market risk premium is 5%, and the size factor and value factor return are 2% and 3%. Below table shows the return characteristics of two stocks A and B: Stock Forecasted return (FR) BMKT BSMB BHML 9.60% 0.9 0.8 -0.5 4.80% 0.8 -0.2 0.4 a. [2pts) According to the Fama-French 3-factor model, what would be the fair return for each stock? b. 2pts Characterize each stock as underpriced, overpriced, or properly priced.

#4. If the expected return and risk of the market portfolio are respectively 5% and 5%...

#4. If the expected return and risk of the market portfolio are respectively 5% and 5% and the riskless rate is 1% use the CAPM to determine if the following stocks are mispriced: Stock Burger King McDonald's Windy City Wieners Expected Return 4% 7.5% 9% Beta 0.6 1.2 1.4 If mispriced, which is (are) underpriced and which is (are) overpriced?

#4. If the expected return and risk of the market portfolio are respectively 5% and 5% and the riskless rate is 1% use the CAPM to determine if the following stocks are mispriced: Stock Burger King McDonald's Windy City Wieners Expected Return 4% 7.5% 9% Beta 0.6 1.2 1.4 If mispriced, which is (are) underpriced and which is (are) overpriced?

2. Consider a market with only two risky stocks, A and B, and one risk-free asset....

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

You own a portfolio equally invested in a risk-free asset and two stocks (If one of...

You own a portfolio equally invested in a risk-free asset and two stocks (If one of the stocks has a beta of 0.97 and the total portfolio is equally as risky as the market, what must the beta be for the other stock in your portfolio? (Hint: Remember that the market has a Beta=1; also remember that equally invested means that each asset has the same weight- since there are 3 assets, each asset's weight is 1/3 or 0.3333). Enter...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

The risk-free rate is 6% and the expected rate of return on the market portfolio is 13%.

a. Calculate the required rate of return on a security with a beta of 1.25. (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.)

b. If the security is expected to return 16%, is it overpriced or underpriced?

The risk-free rate is 6% and the expected rate of return on the market portfolio is 13%.

a. Calculate the required rate of return on a security with a beta of 1.25. (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.)

b. If the security is expected to return 16%, is it overpriced or underpriced?

CAPM For a risky return r, CAPM equation is Er -r- B(E[rm] -r), where r is risk-free rate, Tm is market return, and is loading of risky return r on market return rm In what follows, X and Y denote arbitrary assets, B risk-free bond, M market portfolio. Determine which of the following scenarios are consistent or inconsistent with mean-variance efficiency (that is, CAPM). In your answer, write "Consistent" or "Inconsistent", and give brief explanation. 25% 12% 0.8 1.2 25...

CAPM For a risky return r, CAPM equation is Er -r- B(E[rm] -r), where r is risk-free rate, Tm is market return, and is loading of risky return r on market return rm In what follows, X and Y denote arbitrary assets, B risk-free bond, M market portfolio. Determine which of the following scenarios are consistent or inconsistent with mean-variance efficiency (that is, CAPM). In your answer, write "Consistent" or "Inconsistent", and give brief explanation. 25% 12% 0.8 1.2 25...

11. Assume that the Risk Free rate is 5% and the Expected Return on the market is 10%. Show if these stocks are under, over, or fairly valued. Illustrate it in a chart with the SML and the expected returns of the stocks. CAPM returnasseti RiskFree + [E(Rmarket)- Risk Free] Basset i Security САРМ Over/Under E(Return) Beta Return |Valued? Stock W Stock Y Stock Z 0.035 0.85 1.2 0.095 0.12 1.1 Show (and explain) your results in the following chart....

11. Assume that the Risk Free rate is 5% and the Expected Return on the market is 10%. Show if these stocks are under, over, or fairly valued. Illustrate it in a chart with the SML and the expected returns of the stocks. CAPM returnasseti RiskFree + [E(Rmarket)- Risk Free] Basset i Security САРМ Over/Under E(Return) Beta Return |Valued? Stock W Stock Y Stock Z 0.035 0.85 1.2 0.095 0.12 1.1 Show (and explain) your results in the following chart....

Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%. According to the capital asset pricing model, security X is 1) fairly priced 2) underpriced 3) overpriced 4) None of the answers are correct Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%....

Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%. According to the capital asset pricing model, security X is 1) fairly priced 2) underpriced 3) overpriced 4) None of the answers are correct Security X has a rate of return of 13% and a beta of 1.15. The risk-free rate is 5% and the market expected rate of return is 10%....

Problem 3 The risk-free rate is 2%, the market risk premium is 5%, and the size factor and value factor return are 2% and 3%. Below table shows the return characteristics of two stocks A and B: Stock Forecasted return (FR) BMKT BSMB BHML 9.60% 0.9 0.8 -0.5 4.80% 0.8 -0.2 0.4 a. [2pts) According to the Fama-French 3-factor model, what would be the fair return for each stock? b. 2pts Characterize each stock as underpriced, overpriced, or properly priced.

Problem 3 The risk-free rate is 2%, the market risk premium is 5%, and the size factor and value factor return are 2% and 3%. Below table shows the return characteristics of two stocks A and B: Stock Forecasted return (FR) BMKT BSMB BHML 9.60% 0.9 0.8 -0.5 4.80% 0.8 -0.2 0.4 a. [2pts) According to the Fama-French 3-factor model, what would be the fair return for each stock? b. 2pts Characterize each stock as underpriced, overpriced, or properly priced.

#4. If the expected return and risk of the market portfolio are respectively 5% and 5% and the riskless rate is 1% use the CAPM to determine if the following stocks are mispriced: Stock Burger King McDonald's Windy City Wieners Expected Return 4% 7.5% 9% Beta 0.6 1.2 1.4 If mispriced, which is (are) underpriced and which is (are) overpriced?

#4. If the expected return and risk of the market portfolio are respectively 5% and 5% and the riskless rate is 1% use the CAPM to determine if the following stocks are mispriced: Stock Burger King McDonald's Windy City Wieners Expected Return 4% 7.5% 9% Beta 0.6 1.2 1.4 If mispriced, which is (are) underpriced and which is (are) overpriced?

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

Most questions answered within 3 hours.

-

Problem 1: Present entries to record the selected transactions

described below:

(a)

Issued $2,790,000 of 5-year,...

asked 1 minute ago -

Using technology to support HR activities increases:

a.

the efficiency of the administrative HR functions.

b....

asked 2 minutes ago -

1. List the features used to classify leaf

types.

2. List some characteristics that are shared...

asked 7 minutes ago -

The three elements of Value Proposition, Key Customers, and

Capabilities operate within an environment. Which of...

asked 9 minutes ago -

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 17 minutes ago -

Each row of the table below describes an aqueous solution at

25°C

.

The second column...

asked 21 minutes ago -

A horizontal wire is at y = 0. Current travels in the +x

direction. The magnetic...

asked 22 minutes ago -

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 43 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 41 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 46 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 45 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 51 minutes ago