Homework Answers

Let’s calculate the initial bond price

Bond price P0 = C* [1- 1/ (1+i) ^n] /i + M / (1+i) ^n

Where

M = value at maturity, or par value = $ 1000 (assumed)

C = coupon payment = 15.3% of $1000 = $153

n = number of payments = 30

i = interest rate, or required yield = 9% or 0.09

Bond Price = $153 * [1 – 1 / (1+0.09) ^30] /0.09 + $1000 / (1+0.09) ^30

= $1,571.87 + $75.37

= $1,647.24

e-1. Let’s calculate the exact bond price if it's yield to maturity rises to 10%.

Bond price P0 = C* [1- 1/ (1+i) ^n] /i + M / (1+i) ^n

Where

M = value at maturity, or par value = $ 1000 (assumed)

C = coupon payment = 15.3% of $1000 = $153

n = number of payments = 30

i = interest rate, or required yield = 10% or 0.10

Bond Price = $153 * [1 – 1 / (1+0.1) ^30] /0.1 + $1000 / (1+0.1) ^30

= $1,442.32 + $57.31

=$1,499.63

The price of the bond if its yield to maturity rises to 10% is $1,499.63

e-2. The price predicted by the duration rule

We have duration = 10.59 years and y is yield to maturity = 9%

Predicted price change = – Duration * (change in y)/ (1+y)* P0

= - 10.59 *(0.01)/ (1.09) * $1,647.24

= - $160.04

Therefore, predicted new price =- $160.04 +$1,647.24 = $1,490.06

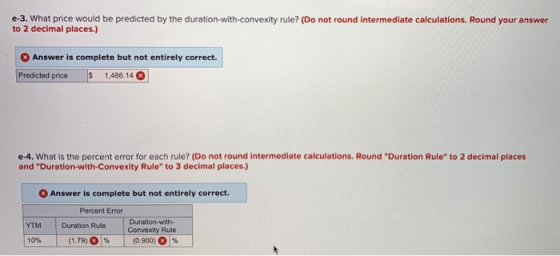

e-3. Using Duration-with-Convexity Rule, assuming yield to maturity rises to 10%

Predicted price change

= [(– Duration * change in y/ (1+y)) + (0.5 * convexity *(change in y) ^2)] * P0

= [(- 10.59 * (0.01) / (1 +0.09)) + (0.5 * 163.0 * (0.01) ^2)] * $1,647.24

= -$146.87

Therefore, predicted price = -$146.87 +$1,647.24 = $1,503.23

e-4.

|

Percent Error |

||

|

YTM |

Duration Rule |

Duration-with- |

|

10% |

[($1,490.06– $1,499.63)/ $1,499.63] * 100 = -0.64% |

[($1,503.23 – $1,499.63)/ $1,499.63] * 100 = 0.240% |

Add Answer to:

Can you please show your work and/or calculator steps?

Problem 11-26 A 30-year maturity bond making...

A 30-year maturity bond making annual coupon payments with a coupon rate of 15.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 15.5% has duration of 9.96 years and convexity of 144.6. The bond currently sells at a yield to maturity of 10%. a. Find the price of the bond if its yield to maturity falls to 9%. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price of the bond $ b. What price would be predicted by the duration rule? (Do not round intermediate...

A 30-year maturity bond making annual coupon payments with a coupon rate of 14.3% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 14.3% has duration of 11.34 years and convexity of 185.7. The bond currently sells at a yield to maturity of 8%. a. Find the price of the bond if its yield to maturity falls to 7%. (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answer to...

A 30-year maturity bond making annual coupon payments with a coupon rate of 15.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 15.5% has duration of 9.96 years and convexity of 144.6. The bond currently sells at a yield to maturity of 10%. a. Find the price of the bond if its yield to maturity falls to 9%. (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answer to...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration of 12.27 years and convexity of 216.28. The bond currently sells at a yield to maturity of 8%. e-1. Find the price of the bond if its yield to maturity increases to 9%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) e-2. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answers to...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration of 12.27 years and convexity of 216.28. The bond currently sells at a yield to maturity of 8%. a. Find the price of the bond if its yield to maturity falls to 7%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) b. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answers to...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8%...

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1392 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration -12.30 years--but considerably higher convexity of 272.9. 1.25 points a. Suppose the yield to maturity on both bonds increases to 9% IWhat will be the actual percentage...

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1392 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration -12.30 years--but considerably higher convexity of 272.9. 1.25 points a. Suppose the yield to maturity on both bonds increases to 9% IWhat will be the actual percentage...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) F...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 146.5 and modified duration of 11.65 years. A 30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration—-11.79 years—-but considerably higher convexity of 231.2. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1392 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration -12.30 years--but considerably higher convexity of 272.9. 1.25 points a. Suppose the yield to maturity on both bonds increases to 9% IWhat will be the actual percentage...

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1392 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration -12.30 years--but considerably higher convexity of 272.9. 1.25 points a. Suppose the yield to maturity on both bonds increases to 9% IWhat will be the actual percentage...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

Most questions answered within 3 hours.

-

In order to investigate how many hours a day students at their

school tend to spend...

asked 1 minute ago -

Discuss why it is necessary to use repetitive statement, and use

segment codes to demonstrate your...

asked 5 minutes ago -

Need help with coming up with competitive strategies in

the furniture retail industry. Any help would...

asked 13 minutes ago -

how to select perpendicular gd&t tolerance value

using IT tolerance. and gave example

asked 20 minutes ago -

plz explain: A sound that changes pressure from 100 mPa to 10

mPa has a change...

asked 20 minutes ago -

What is the measured air concentration from a sample that has 38

μg of contaminant when...

asked 40 minutes ago -

In support of the argument that we have free will, what are the

implications of seemingly...

asked 40 minutes ago -

Share your thoughts concerning the pros and cons of using

natural products as anticancer agents. (please...

asked 50 minutes ago -

Describe in detail how your own actions reflect the

ideas shared in the discussion, and relate...

asked 54 minutes ago -

Name and clearly describe one technique for determining the age

of fossils in geological context. Are...

asked 1 hour ago -

A ball is thrown with an initial velocity of 20.0 m/s at an

angle of 35.00...

asked 1 hour ago -

When assessing pension risk, analysts compute ratios for both

long- and short-term risk. Which statement below...

asked 1 hour ago