Homework Answers

Add Answer to:

Return to question A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8%...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 146.5 and modified duration of 11.65 years. A 30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration—-11.79 years—-but considerably higher convexity of 231.2. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each...

A 9-year maturity zero-coupon bond selling at a yield to maturity of 8.25% (effective annual yield)...

A 9-year maturity zero-coupon bond selling at a yield to maturity of 8.25% (effective annual yield) has convexity of 156.3 and modified duration of 8.06 years. A 30-year maturity 6.5% coupon bond making annual coupon payments also selling at a yield to maturity of 8.25% has nearly identical duration--8.04 years-but considerably higher convexity of 248.2 a. Suppose the yield to maturity on both bonds increases to 9.25%. What will be the actual percentage capital loss on each bond? What percentage...

A 9-year maturity zero-coupon bond selling at a yield to maturity of 8.25% (effective annual yield) has convexity of 156.3 and modified duration of 8.06 years. A 30-year maturity 6.5% coupon bond making annual coupon payments also selling at a yield to maturity of 8.25% has nearly identical duration--8.04 years-but considerably higher convexity of 248.2 a. Suppose the yield to maturity on both bonds increases to 9.25%. What will be the actual percentage capital loss on each bond? What percentage...

A 30-year maturity 6% coupon bond making annual coupon payments selling at a yield to maturity...

A 30-year maturity 6% coupon bond making annual coupon payments selling at a yield to maturity of 8% has a duration of 11.79 years and a convexity of 231.2. a. Suppose the yield to maturity increases to 9%. What will be the actual percentage capital loss on the bond? What percentage capital loss would be predicted by the duration rule and the duration-with-convexity rule? b. Repeat part (a), but this time assume the yield to maturity decreases to 7%. c....

Zero-coupon bond YTM

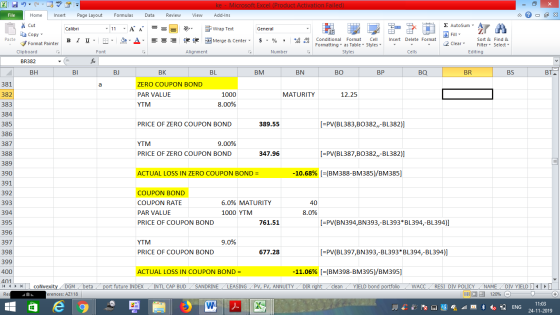

A 12.75-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 150.3 and modified duration of 11.81 years. A30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical duration—11.79 years—but considerablyhigher convexity of 231.2.Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What percentage capital loss would bepredicted...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) F...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity - 61.810 Duration - 7.330 Years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7.7% to...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

A 13.05-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 1572 and modified duration of 12.08 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years—but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. 1. What will be the actual percentage capital loss on each bond?...

A 9-year maturity zero-coupon bond selling at a yield to maturity of 8.25% (effective annual yield) has convexity of 156.3 and modified duration of 8.06 years. A 30-year maturity 6.5% coupon bond making annual coupon payments also selling at a yield to maturity of 8.25% has nearly identical duration--8.04 years-but considerably higher convexity of 248.2 a. Suppose the yield to maturity on both bonds increases to 9.25%. What will be the actual percentage capital loss on each bond? What percentage...

A 9-year maturity zero-coupon bond selling at a yield to maturity of 8.25% (effective annual yield) has convexity of 156.3 and modified duration of 8.06 years. A 30-year maturity 6.5% coupon bond making annual coupon payments also selling at a yield to maturity of 8.25% has nearly identical duration--8.04 years-but considerably higher convexity of 248.2 a. Suppose the yield to maturity on both bonds increases to 9.25%. What will be the actual percentage capital loss on each bond? What percentage...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

Most questions answered within 3 hours.

-

A statistics student finds herself struggling with a newspaper

article stating that only eighteen percent of...

asked 18 minutes ago -

People with beriberi, a disease caused by a thiamin deficiency,

have elevated levels of blood pyruvate...

asked 5 minutes ago -

PYTHON Programming Exercise 2: Create a Simple Cost Calculator

Write a program that displays input fields...

asked 11 minutes ago -

1.Seki agreed that Groupon could sell 18 hot air

balloon rides on his Magical Adventures company...

asked 12 minutes ago -

A cohort study is conducted to determine whether smoking is

associated with an increased risk of...

asked 17 minutes ago -

Create the pseudo-code/flowchart for an application class named

Monogram. Its main() method inputs three variables that...

asked 18 minutes ago -

How many liters of water are required to dissolve 1.00 g of

silver chromate? Express your...

asked 20 minutes ago -

Hot: T_inlet = 80, T_out = 65

Cold: T_inlet = 10, T_out = 25

Explain in...

asked 21 minutes ago -

Two protons fly in different directions and collide. They both

have a total energy of 1.5...

asked 30 minutes ago -

What is the oxidation number of each atom in sodium phosphate,

Na3PO4?

>>> SHOW YOUR WORK...

asked 36 minutes ago -

D company purchased goods with a list price of $60000, subject

to trade discounts of 20%...

asked 39 minutes ago -

Transposable elements make up more than 40% of the human genome

and are inserted more-or-less randomly...

asked 50 minutes ago