The daily changes in stock prices exhibit a random behavior, which means that these daily changes...

The daily changes in stock prices exhibit a random behavior, which means that these daily changes are independent of each other and can be approximated by a normal distribution. To test this theory, collect data for one company that is traded on the Tokyo Stock Exchange, one company traded on the Shanghai Stock Exchange, and one company traded on the Hong Kong Stock Exchange and then do the following:

1. Record the daily closing stock price of each of these companies for six consecutive weeks (so you may have 30 values per company).

2. For each of your six data sets, decide if the data are approximately normally distributed by:

a. constructing the stem-and-leaf display, histogram or polygon, and boxplot.

b. comparing data characteristics to theoretical properties.

c. constructing a normal probability plot.

d. Discuss the results of (a) through (c). What can you say about your three stocks with respect to daily closing prices and daily changes in closing prices? Which, if any, of the data sets are approximately normally distributed?

Homework Answers

| Date | id | open_s | high_s | low_s | close_s | volume_s | open_h | high_h | low_h | close_h | volume_h |

| 2/13/2018 | 1 | 1,077 | 1,077 | 998 | 999 | 250,700 | 3,798 | 3,818 | 3,724 | 3,730 | 7,767,700 |

| 2/9/2018 | 2 | 1,012 | 1,042 | 1,000 | 1,036 | 148,900 | 3,751 | 3,796 | 3,740 | 3,795 | 8,358,200 |

| 2/8/2018 | 3 | 1,074 | 1,098 | 1,053 | 1,073 | 123,500 | 3,884 | 3,927 | 3,849 | 3,873 | 7,623,900 |

| 2/7/2018 | 4 | 1,151 | 1,151 | 1,061 | 1,063 | 202,200 | 3,933 | 3,947 | 3,839 | 3,840 | 9,005,600 |

| 2/6/2018 | 5 | 1,088 | 1,139 | 1,003 | 1,074 | 447,500 | 3,831 | 3,831 | 3,723 | 3,810 | 10,651,900 |

| 2/5/2018 | 6 | 1,226 | 1,263 | 1,212 | 1,238 | 185,000 | 3,983 | 4,030 | 3,946 | 3,971 | 9,843,400 |

| 2/2/2018 | 7 | 1,318 | 1,318 | 1,274 | 1,304 | 84,200 | 3,858 | 3,900 | 3,840 | 3,890 | 5,681,300 |

| 2/1/2018 | 8 | 1,317 | 1,325 | 1,281 | 1,309 | 141,700 | 3,850 | 3,871 | 3,844 | 3,859 | 4,709,900 |

| 1/31/2018 | 9 | 1,268 | 1,322 | 1,251 | 1,293 | 159,900 | 3,890 | 3,890 | 3,817 | 3,826 | 6,285,000 |

| 1/30/2018 | 10 | 1,308 | 1,315 | 1,271 | 1,289 | 202,600 | 3,958 | 3,985 | 3,916 | 3,925 | 3,991,000 |

| 1/29/2018 | 11 | 1,324 | 1,328 | 1,294 | 1,312 | 120,600 | 3,922 | 3,976 | 3,899 | 3,947 | 3,107,900 |

| 1/26/2018 | 12 | 1,269 | 1,313 | 1,262 | 1,308 | 188,000 | 3,950 | 3,968 | 3,931 | 3,933 | 3,316,700 |

| 1/25/2018 | 13 | 1,258 | 1,260 | 1,228 | 1,253 | 111,300 | 3,943 | 3,953 | 3,925 | 3,942 | 4,274,900 |

| 1/24/2018 | 14 | 1,275 | 1,279 | 1,240 | 1,264 | 123,700 | 4,025 | 4,031 | 3,993 | 3,994 | 2,881,200 |

| 1/23/2018 | 15 | 1,265 | 1,284 | 1,249 | 1,282 | 142,800 | 3,993 | 4,066 | 3,991 | 4,052 | 3,664,800 |

| 1/22/2018 | 16 | 1,216 | 1,256 | 1,196 | 1,247 | 120,800 | 4,000 | 4,000 | 3,960 | 3,980 | 2,830,500 |

| 1/19/2018 | 17 | 1,226 | 1,235 | 1,200 | 1,216 | 95,300 | 3,993 | 4,017 | 3,981 | 4,003 | 2,991,300 |

| 1/18/2018 | 18 | 1,245 | 1,264 | 1,217 | 1,218 | 182,600 | 4,037 | 4,043 | 3,971 | 3,977 | 4,732,000 |

| 1/17/2018 | 19 | 1,176 | 1,234 | 1,165 | 1,221 | 178,200 | 3,989 | 4,019 | 3,977 | 4,019 | 3,653,300 |

| 1/16/2018 | 20 | 1,169 | 1,207 | 1,151 | 1,200 | 134,500 | 3,983 | 3,998 | 3,965 | 3,989 | 2,983,200 |

| 1/15/2018 | 21 | 1,170 | 1,178 | 1,147 | 1,171 | 118,400 | 4,000 | 4,006 | 3,971 | 3,981 | 2,975,900 |

| 1/12/2018 | 22 | 1,186 | 1,192 | 1,156 | 1,164 | 100,000 | 4,005 | 4,010 | 3,966 | 3,968 | 5,005,900 |

| 1/11/2018 | 23 | 1,199 | 1,199 | 1,167 | 1,181 | 121,000 | 4,035 | 4,055 | 3,998 | 4,026 | 4,031,200 |

| 1/10/2018 | 24 | 1,217 | 1,219 | 1,179 | 1,211 | 169,500 | 4,035 | 4,151 | 4,028 | 4,102 | 4,692,400 |

| 1/9/2018 | 25 | 1,194 | 1,218 | 1,183 | 1,216 | 139,000 | 4,042 | 4,057 | 3,997 | 4,010 | 3,447,000 |

| 1/5/2018 | 26 | 1,185 | 1,190 | 1,167 | 1,182 | 53,200 | 4,000 | 4,054 | 3,990 | 4,021 | 4,765,200 |

| 1/4/2018 | 27 | 1,151 | 1,184 | 1,146 | 1,178 | 100,500 | 3,925 | 3,986 | 3,906 | 3,986 | 4,962,300 |

| 12/29/2017 | 28 | 1,155 | 1,161 | 1,131 | 1,137 | 87,700 | 3,860 | 3,880 | 3,852 | 3,862 | 2,100,400 |

| 12/28/2017 | 29 | 1,194 | 1,194 | 1,148 | 1,151 | 137,600 | 3,893 | 3,903 | 3,861 | 3,866 | 1,770,100 |

| 12/27/2017 | 30 | 1,145 | 1,194 | 1,143 | 1,194 | 102,600 | 3,886 | 3,908 | 3,879 | 3,895 | 1,387,100 |

Here, open_s, high_s, low_s, close_s, & volume_s represents the variables of the stock prices of Suzuki co. ltd. whereas open_h, high_h, low_h, close_h & volume_h represents the variables of stock prices of Honda motor co. ltd.

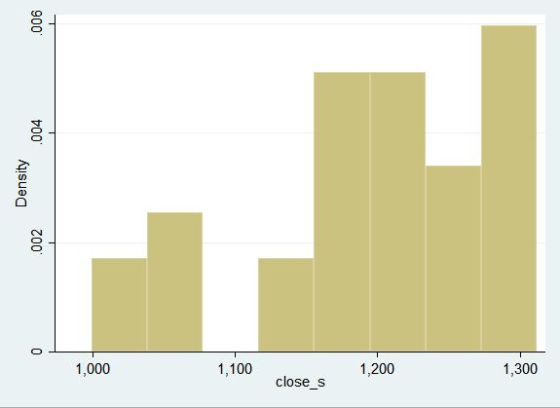

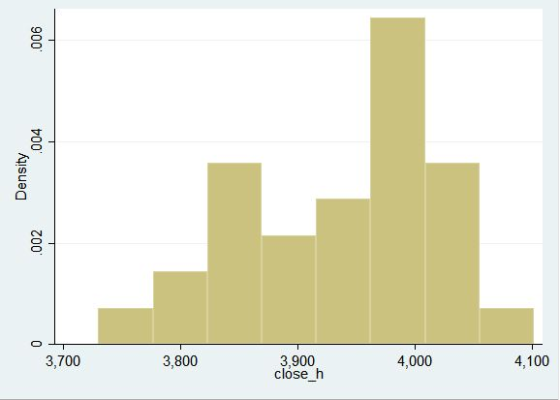

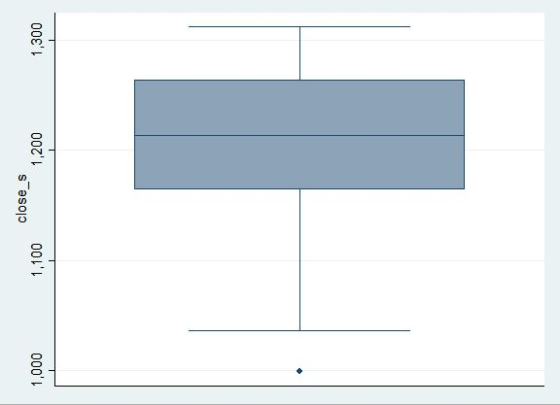

1) Just look at the 6th and 11th columns. close_s and close_h.

2) Now we make the stem and leaf display, histogram and boxplot of closing stock price.

b.) Various descriptive information

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| open_s | 30 | 1202 | 77 | 1012 | 1324 |

| high_s | 30 | 1221 | 75 | 1042 | 1328 |

| low_s | 30 | 1172 | 83 | 998 | 1294 |

| close_s | 30 | 1199 | 85 | 999 | 1312 |

| volume_s | 30 | 149117 | 70460 | 53200 | 447500 |

| open_h | 30 | 3942 | 77 | 3751 | 4042 |

| high_h | 30 | 3969 | 83 | 3796 | 4151 |

| low_h | 30 | 3909 | 85 | 3723 | 4028 |

| close_h | 30 | 3936 | 86 | 3730 | 4102 |

| volume_h | 30 | 4783040 | 2395922 | 1387100 | 10700000 |

![Normal F[(close_s-m)/s] 0.50 3 0.00 0.25 0.75 1.00 2 0 3](http://img.homeworklib.com/questions/fd2ec8d0-1ba5-11ec-9a9e-a1b9eb7e6833.png?x-oss-process=image/resize,w_560)

![Normal F[(close h-m)/s] 0.50 6 9 0.00 0.25 0.75 1.00 3 0 2 0 3](http://img.homeworklib.com/questions/fdb5aa60-1ba5-11ec-bf19-7d8da75a5cbd.png?x-oss-process=image/resize,w_560)

We will test for normality by Shapiro-Wilk test.

In the shapirowilk test, null hypothesis state that data is normally distributed. Here, p-value for close_h is 0.515 and for close_h it is 0.068. We fail to reject the null hypothesis. Here, we observed that close_h(onda) and close_s(uzuki) are normally distributed. Thus, we found that both the variables close_h and close_s are normally distributed.

Add Answer to:

The daily changes in stock prices exhibit a random behavior,

which means that these daily changes...

The daily changes in the closing price of stock follow a random walk. That is, these...

The daily changes in the closing price of stock follow a random walk. That is, these daily events are independent of each other and move upward or downward in a random matter and can be approximated by a normal distribution. Let's test this theory. Use either a newspaper, or the Internet to select one company traded on the NYSE. Record the daily closing stock price of your company for the six past consecutive weeks (so that you have 30 values)....

Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1...

Visit the NASDAQ historical prices weblink. First, set the date

range to be for exactly 1 year ending on the Monday that this

course started. Use March 18, 2018 – March 19, 2019. Do this by

clicking on the blue dates after “Time Period”. Next, click the

“Apply” button. Next, click the link on the right side of the page

that says “Download Data” to save the file to your computer.

This project will only use the Close values. Assume...

Visit the NASDAQ historical prices weblink. First, set the date

range to be for exactly 1 year ending on the Monday that this

course started. Use March 18, 2018 – March 19, 2019. Do this by

clicking on the blue dates after “Time Period”. Next, click the

“Apply” button. Next, click the link on the right side of the page

that says “Download Data” to save the file to your computer.

This project will only use the Close values. Assume...

Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year en...

Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on the Monday that this course started. For example, if the current term started on April 1, 2018, then use April 1, 2017 – March 31, 2018. (Do NOT use these dates. Use the dates that match up with the current term.) Do this by clicking on the blue dates after “Time Period”. Next, click the “Apply” button. Next, click the link...

Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year en...

Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on the Monday that this course started. For example, if the current term started on April 1, 2018, then use April 1, 2017 – March 31, 2018. (Do NOT use these dates. Use the dates that match up with the current term.) MY DATES ARE MARCH 18 2018 - MARCH 19 2019 Do this by clicking on the blue dates after “Time...

PROJECT 3 INSTRUCTIONS Based on Brase & Brase : sections 6.1-6.3 Note that you must do this Visit...

continuation to previous question

PROJECT 3 INSTRUCTIONS Based on Brase & Brase : sections 6.1-6.3 Note that you must do this Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on that says "Download Data" to save the file project on your to your computer This project will only use the Close values. Assume that the closing prices of the stock form a normally distributed data set. This means that you...

continuation to previous question

PROJECT 3 INSTRUCTIONS Based on Brase & Brase : sections 6.1-6.3 Note that you must do this Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on that says "Download Data" to save the file project on your to your computer This project will only use the Close values. Assume that the closing prices of the stock form a normally distributed data set. This means that you...

Case assignments must be completed with a written 2-page study on the assigned case questions in...

Case assignments must be completed with a written 2-page study on the assigned case questions in the textbook. The format requested for these assignments is based on elaborating and including two basic parts in the essay: 1) in a bullet presentation style (one phrase each bullet), list a summary of the key issues, situations, problems, opportunities and threats you may identify as relevant; 2) answer all the questions listed in each case in two or three sound paragraphs. Use the...

&...

SOME DRAWBACKS OF BLACK-SCHOLES To provide one motivation for the development of ARCH models (next handout), we briefly discuss here some difficulties associated with the Black Scholes formula, which is widely used to calculate the price of an option. For example, consider a European call option for a stock. This is the right to buy a specific number of shares of a specific stock on a specific date in the future, at a specific price (the exercise price, also called...

Question 12 pts The length of time a person takes to decide which shoes to purchase...

Question 12 pts The length of time a person takes to decide which shoes to purchase is normally distributed with a mean of 8.21 minutes and a standard deviation of 1.90. Find the probability that a randomly selected individual will take less than 6 minutes to select a shoe purchase. Is this outcome unusual? Group of answer choices Probability is 0.88, which is usual as it is greater than 5% Probability is 0.12, which is usual as it is not...

10.3Thank you:) Complete parts (a) through (c) below. (a) Determine the critical value(s) for a right-tailed...

10.3Thank you:)

Complete parts (a) through (c) below. (a) Determine the critical value(s) for a right-tailed test of a population mean at the a = 0.01 level of significance with 15 degrees of freedom. (b) Determine the critical value(s) for a left-tailed test of a population mean at the a = 0.01 level of significance based on a sample size of n = 10. (c) Determine the critical value(s) for a two-tailed test of a population mean at the a...

10.3Thank you:)

Complete parts (a) through (c) below. (a) Determine the critical value(s) for a right-tailed test of a population mean at the a = 0.01 level of significance with 15 degrees of freedom. (b) Determine the critical value(s) for a left-tailed test of a population mean at the a = 0.01 level of significance based on a sample size of n = 10. (c) Determine the critical value(s) for a two-tailed test of a population mean at the a...

Visit the NASDAQ historical prices weblink. First, set the date

range to be for exactly 1 year ending on the Monday that this

course started. Use March 18, 2018 – March 19, 2019. Do this by

clicking on the blue dates after “Time Period”. Next, click the

“Apply” button. Next, click the link on the right side of the page

that says “Download Data” to save the file to your computer.

This project will only use the Close values. Assume...

Visit the NASDAQ historical prices weblink. First, set the date

range to be for exactly 1 year ending on the Monday that this

course started. Use March 18, 2018 – March 19, 2019. Do this by

clicking on the blue dates after “Time Period”. Next, click the

“Apply” button. Next, click the link on the right side of the page

that says “Download Data” to save the file to your computer.

This project will only use the Close values. Assume...

continuation to previous question

PROJECT 3 INSTRUCTIONS Based on Brase & Brase : sections 6.1-6.3 Note that you must do this Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on that says "Download Data" to save the file project on your to your computer This project will only use the Close values. Assume that the closing prices of the stock form a normally distributed data set. This means that you...

continuation to previous question

PROJECT 3 INSTRUCTIONS Based on Brase & Brase : sections 6.1-6.3 Note that you must do this Visit the NASDAQ historical prices weblink. First, set the date range to be for exactly 1 year ending on that says "Download Data" to save the file project on your to your computer This project will only use the Close values. Assume that the closing prices of the stock form a normally distributed data set. This means that you...

10.3Thank you:)

Complete parts (a) through (c) below. (a) Determine the critical value(s) for a right-tailed test of a population mean at the a = 0.01 level of significance with 15 degrees of freedom. (b) Determine the critical value(s) for a left-tailed test of a population mean at the a = 0.01 level of significance based on a sample size of n = 10. (c) Determine the critical value(s) for a two-tailed test of a population mean at the a...

10.3Thank you:)

Complete parts (a) through (c) below. (a) Determine the critical value(s) for a right-tailed test of a population mean at the a = 0.01 level of significance with 15 degrees of freedom. (b) Determine the critical value(s) for a left-tailed test of a population mean at the a = 0.01 level of significance based on a sample size of n = 10. (c) Determine the critical value(s) for a two-tailed test of a population mean at the a...

Most questions answered within 3 hours.

-

Given the following table of high speed internet access vs.

annual home income:

Home Income

%...

asked 18 minutes ago -

A baseball batter hits a 0.145kg baseball straight up into the

air. The baseball leaves the...

asked 50 minutes ago -

An FM modulator is tested using

single-tone baseband signal with frequency of 50kHz and a sprectrum...

asked 1 hour ago -

Write the ionic equations for the first stage of salts

hydrolysis.

Anion, Cation?

Na2S

NiSO4

K2SO4...

asked 2 hours ago -

suppose there is a normally distributed population with a mean of

250 and a standard deviation...

asked 3 hours ago -

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 4 hours ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 4 hours ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 5 hours ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 5 hours ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 5 hours ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 6 hours ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 6 hours ago