Problem 5.10.10 Suppose you have n suitcases and suitcase i holds Xi dollars where X1, X2,...

- Problem 5.10.10

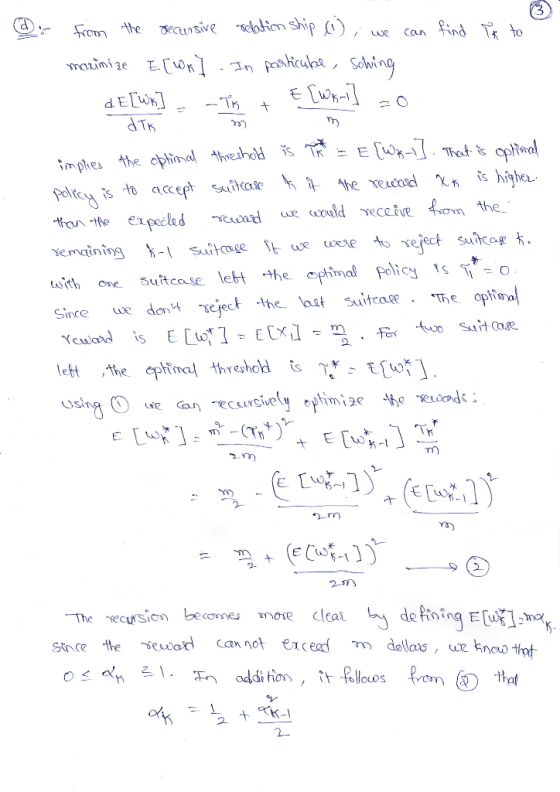

Suppose you have n suitcases and suitcase i holds Xi dollars where X1, X2, …, Xn are iid continuous uniform (0, m) random variables. (Think of a number like one million for the symbol m.) Unfortunately, you don’t know Xi until you open suitcase i.

Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase 1. After opening suitcase i, you can either accept or reject Xi dollars. If you accept suitcase i, the game ends. If you reject, then you get to choose only from the still unopened suitcases.

- should you do? Perhaps it is not so obvious? In fact, you can decide before the game on a policy, a set of rules to follow. We will specify a policy by a vector (t1, … tn) of threshold parameters.

- After opening suitcase i, you accept the amount Xi if Xi≥ti .

- Otherwise, you reject suitcase i and open suitcase i-1.

- If you have rejected suitcases n down through 2, then you must accept the amount X1 in suitcase 1. Thus the threshold t1=0 since you never reject the amount in the last suitcase.

- Suppose you reject suitcase n through i+1, but then you accept suitcase i. Find E[Xi|Xi≥ ti ].

- Let Wk denote your reward given that there are k unopened suitcases remaining. What is E[W1]?

- As a function of tk, find a recursive relationship for E[Wk] in terms of tk and E[Wk-1].

- For n=4 suitcases, find the policy (t1*, … t4*) that maximizes E[W4].

"Can I assume that Tau_i is m if i ==n, is 1/2 m at i ==1, and 0 at i ==0?"

Homework Answers

Add Answer to:

Problem 5.10.10

Suppose you have n suitcases and

suitcase i holds Xi dollars where

X1, X2,...

Problem 5.10.10 Suppose you have n suitcases and suitcase i holds Xi dollars where X1, X2, …, Xn ...

Problem 5.10.10 Suppose you have n suitcases and suitcase i holds Xi dollars where X1, X2, …, Xn are iid continuous uniform (0, m) random variables. (Think of a number like one million for the symbol m.) Unfortunately, you don’t know Xi until you open suitcase i. Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase 1. After opening suitcase i, you can either accept or reject Xi dollars. If you...

This question is from the book Probability and Stochastic Processes (3rd Edition) by Yates questi...

this

question is from the book Probability and Stochastic Processes (3rd

Edition) by Yates question 5.10.10

2. Problem 5.10.10 Suppose you have n suitcases and suitcase i holds I dollars where Xi. X. I are iid continuous uniform (0. m) random variables. Think of mber ke one milion for the symbo m.) Unfortunately, you don t know X, until you open suitcase Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase...

this

question is from the book Probability and Stochastic Processes (3rd

Edition) by Yates question 5.10.10

2. Problem 5.10.10 Suppose you have n suitcases and suitcase i holds I dollars where Xi. X. I are iid continuous uniform (0. m) random variables. Think of mber ke one milion for the symbo m.) Unfortunately, you don t know X, until you open suitcase Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase...

Suppose Y = X1 + X2, where Xi ? exp(1) for i = 1, 2. Determine...

Suppose Y = X1 + X2, where Xi ? exp(1) for i = 1, 2. Determine the distribution of Y

Suppose n numbers X1, X2, . . . , Xn are chosen from a uniform distribution on [0, 10]. We say th...

Suppose n numbers X1, X2, . . . , Xn are chosen from a uniform distribution on [0, 10]. We say that there is an increase at i if Xi < Xi+1. Let I be the number of increases. Find E[I].

Suppose X1, X2, . . . are independent discrete random variables, having the same distribution, and...

Suppose X1, X2, . . . are independent discrete random variables,

having the same distribution, and E[Xi] > 0, for each i. Is thus

true for any two positive integers n and m?:

Why not, or why yes?

Suppose X1, X2, . . . are independent discrete random variables,

having the same distribution, and E[Xi] > 0, for each i. Is thus

true for any two positive integers n and m?:

Why not, or why yes?

Problem 4 Suppose X1, ..., Xn ~ f(x) independently. Let u = E(Xi) and o2 = Var(Xi). Let X Xi/n. (1) Calculate E(X) and...

Problem 4 Suppose X1, ..., Xn ~ f(x) independently. Let u = E(Xi) and o2 = Var(Xi). Let X Xi/n. (1) Calculate E(X) and Var(X) (2) Explain that X -> u as n -> co. What is the shape of the density of X? (3) Let XiBernoulli(p), calculate u and a2 in terms of p. (4) Continue from (3), explain that X is the frequency of heads. Calculate E(X) and Var(X). Explain that X -> p. What is the shape...

Problem 4 Suppose X1, ..., Xn ~ f(x) independently. Let u = E(Xi) and o2 = Var(Xi). Let X Xi/n. (1) Calculate E(X) and Var(X) (2) Explain that X -> u as n -> co. What is the shape of the density of X? (3) Let XiBernoulli(p), calculate u and a2 in terms of p. (4) Continue from (3), explain that X is the frequency of heads. Calculate E(X) and Var(X). Explain that X -> p. What is the shape...

11. Let X1, X2, X3 and X4 be independent lifetimes of memory chips. Suppose that Xi...

11. Let X1, X2, X3 and X4 be independent lifetimes of memory chips. Suppose that Xi N(300, 102) for i = 1, 2, 3, 4 where the parameters are measured in hours. Compute the prob- ability that at least two of the four chips lasts at least 310 hours. (You may leave your answer in terms of an integral, in terms of, or you may leave your answer as an actual real number).

11. Let X1, X2, X3 and X4 be independent lifetimes of memory chips. Suppose that Xi N(300, 102) for i = 1, 2, 3, 4 where the parameters are measured in hours. Compute the prob- ability that at least two of the four chips lasts at least 310 hours. (You may leave your answer in terms of an integral, in terms of, or you may leave your answer as an actual real number).

Suppose that Xi, X2,..., Xn are independent random variables (not iid) with densities x, (x^, where...

Suppose that Xi, X2,..., Xn are independent random variables (not iid) with densities x, (x^, where 6, > 0, for i-1, 2, , n. versus H1: not Ho (c) Suppose Ho is true so that the common distribution of X1, X2,..., Xn, now viewed as being conditional on 6, is described by where θ > 0. Identify a conjugate prior for 0. Specify any hyperparameters in your prior (pick values for fun if you want). Show how to carry out...

Suppose that Xi, X2,..., Xn are independent random variables (not iid) with densities x, (x^, where 6, > 0, for i-1, 2, , n. versus H1: not Ho (c) Suppose Ho is true so that the common distribution of X1, X2,..., Xn, now viewed as being conditional on 6, is described by where θ > 0. Identify a conjugate prior for 0. Specify any hyperparameters in your prior (pick values for fun if you want). Show how to carry out...

Need help solving a linear programming problem. Can you please use step by teps in excel solver and show work so I can follow. Thank you. Portfolio Xi= The amount of dollars to invest in stock i i=1=A...

Need help solving a linear programming problem. Can you please use step by teps in excel solver and show work so I can follow. Thank you. Portfolio Xi= The amount of dollars to invest in stock i i=1=A, 2=B, 3=C, 4=D, 5=E Max Expected Return Z=4.5X1+5.2X2+6.0X3+7.2X4+4.2X5 Subject to: X1+X3<=50,000 X2+X5<=50,000 X4<=50,000 X1>=20,000 X3<=0.2(X1+X3) X1+X2+X3+x4+X5<=100,000 Xi>=0 for all i

4. Suppose X1, . . . ,X, are independent, normally distributed with mean E(Xi) and variance...

4. Suppose X1, . . . ,X, are independent, normally distributed with mean E(Xi) and variance Var(X)-σί. Let Żi-(X,-μ.)/oi so that Zi , . . . , Ζ,, are independent and each has a N(0, 1) distribution. Show that LZhas a x2 distribution. Hint: Use the fact that each Z has a xî distribution i naS

4. Suppose X1, . . . ,X, are independent, normally distributed with mean E(Xi) and variance Var(X)-σί. Let Żi-(X,-μ.)/oi so that Zi , . . . , Ζ,, are independent and each has a N(0, 1) distribution. Show that LZhas a x2 distribution. Hint: Use the fact that each Z has a xî distribution i naS

this

question is from the book Probability and Stochastic Processes (3rd

Edition) by Yates question 5.10.10

2. Problem 5.10.10 Suppose you have n suitcases and suitcase i holds I dollars where Xi. X. I are iid continuous uniform (0. m) random variables. Think of mber ke one milion for the symbo m.) Unfortunately, you don t know X, until you open suitcase Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase...

this

question is from the book Probability and Stochastic Processes (3rd

Edition) by Yates question 5.10.10

2. Problem 5.10.10 Suppose you have n suitcases and suitcase i holds I dollars where Xi. X. I are iid continuous uniform (0. m) random variables. Think of mber ke one milion for the symbo m.) Unfortunately, you don t know X, until you open suitcase Suppose you can open the suitcases one by one, starting with suitcase n and going down to suitcase...

Suppose X1, X2, . . . are independent discrete random variables,

having the same distribution, and E[Xi] > 0, for each i. Is thus

true for any two positive integers n and m?:

Why not, or why yes?

Suppose X1, X2, . . . are independent discrete random variables,

having the same distribution, and E[Xi] > 0, for each i. Is thus

true for any two positive integers n and m?:

Why not, or why yes?

Problem 4 Suppose X1, ..., Xn ~ f(x) independently. Let u = E(Xi) and o2 = Var(Xi). Let X Xi/n. (1) Calculate E(X) and Var(X) (2) Explain that X -> u as n -> co. What is the shape of the density of X? (3) Let XiBernoulli(p), calculate u and a2 in terms of p. (4) Continue from (3), explain that X is the frequency of heads. Calculate E(X) and Var(X). Explain that X -> p. What is the shape...

Problem 4 Suppose X1, ..., Xn ~ f(x) independently. Let u = E(Xi) and o2 = Var(Xi). Let X Xi/n. (1) Calculate E(X) and Var(X) (2) Explain that X -> u as n -> co. What is the shape of the density of X? (3) Let XiBernoulli(p), calculate u and a2 in terms of p. (4) Continue from (3), explain that X is the frequency of heads. Calculate E(X) and Var(X). Explain that X -> p. What is the shape...

11. Let X1, X2, X3 and X4 be independent lifetimes of memory chips. Suppose that Xi N(300, 102) for i = 1, 2, 3, 4 where the parameters are measured in hours. Compute the prob- ability that at least two of the four chips lasts at least 310 hours. (You may leave your answer in terms of an integral, in terms of, or you may leave your answer as an actual real number).

11. Let X1, X2, X3 and X4 be independent lifetimes of memory chips. Suppose that Xi N(300, 102) for i = 1, 2, 3, 4 where the parameters are measured in hours. Compute the prob- ability that at least two of the four chips lasts at least 310 hours. (You may leave your answer in terms of an integral, in terms of, or you may leave your answer as an actual real number).

Suppose that Xi, X2,..., Xn are independent random variables (not iid) with densities x, (x^, where 6, > 0, for i-1, 2, , n. versus H1: not Ho (c) Suppose Ho is true so that the common distribution of X1, X2,..., Xn, now viewed as being conditional on 6, is described by where θ > 0. Identify a conjugate prior for 0. Specify any hyperparameters in your prior (pick values for fun if you want). Show how to carry out...

Suppose that Xi, X2,..., Xn are independent random variables (not iid) with densities x, (x^, where 6, > 0, for i-1, 2, , n. versus H1: not Ho (c) Suppose Ho is true so that the common distribution of X1, X2,..., Xn, now viewed as being conditional on 6, is described by where θ > 0. Identify a conjugate prior for 0. Specify any hyperparameters in your prior (pick values for fun if you want). Show how to carry out...

4. Suppose X1, . . . ,X, are independent, normally distributed with mean E(Xi) and variance Var(X)-σί. Let Żi-(X,-μ.)/oi so that Zi , . . . , Ζ,, are independent and each has a N(0, 1) distribution. Show that LZhas a x2 distribution. Hint: Use the fact that each Z has a xî distribution i naS

4. Suppose X1, . . . ,X, are independent, normally distributed with mean E(Xi) and variance Var(X)-σί. Let Żi-(X,-μ.)/oi so that Zi , . . . , Ζ,, are independent and each has a N(0, 1) distribution. Show that LZhas a x2 distribution. Hint: Use the fact that each Z has a xî distribution i naS

Most questions answered within 3 hours.

-

Water has significant IMF, which result in many of its unique

properties—high boiling point relative to...

asked 12 minutes ago -

I need help with an executive summary for Adidas Items to be

included are a discription...

asked 5 minutes ago -

19. Most progressive reform activists were white

and a. upper class. b. lower class. c. wokring...

asked 7 minutes ago -

If X is a binomial random variable with n = 8

and p = 0.2, the...

asked 17 minutes ago -

Seasonal or cyclical variation in a time-series model…

---exhibits irregular

variation that can be accounted for...

asked 18 minutes ago -

Please use Barney's VRIO framework of analysis to evaluate a

firm's competencies. Please choose a specific...

asked 31 minutes ago -

Where would you expect to have diabetes contributing to the most

DALYs in 2035, according to...

asked 32 minutes ago -

1.) Major league baseball salaries averaged $1.5 million with a

standard deviation of $1 million in...

asked 41 minutes ago -

A hedge fund is holding a three-year,

$10 million face value 6 percent annual coupon bond...

asked 53 minutes ago -

The focal length of a makeup (concave) mirror is 0.48 m. What

magnification does this mirror...

asked 57 minutes ago -

TRUE/FALSE

Long-lived assets that are tangible in nature, used in the

operations of the business, and...

asked 58 minutes ago -

A dragon biologist is setting up an experimental population of

1000 individuals. In dragons, pointy crests...

asked 1 hour ago