- 1. Prepare a flexible budget.

- 2. Compute the sales volume variance and the variable cost volume variances based on a comparison between the master budget and the flexible budget

- 3.Compute flexible budget variances by comparing the flexible budget with the actual results.

- 4.Summarize the results of the sales volume and variable cost volume variances computations based on the comparison between the master budget and the flexible budget.

- 5.Summarize the results of the flexible budget variances computations based on the comparison between the flexible budget and the actual results.

- 6.Justify the favorable or unfavorable budget variances.

- 7.Since this is a not-for-profit organization, address why anyone should be concerned with meeting the budget.

- 8.Make recommendations for what can be done differently to stay on budget for future luncheons. Provide specific examples to support your recommendations.

Homework Answers

a.

|

Master Budget |

- |

Flexible Budget |

= |

Volume Variance |

|

|

Allocated funds |

$25,290 |

$25,290 |

$0 |

||

|

Expenses: |

|||||

|

Variable expenses |

|||||

|

Meals |

20,300 |

23,490 (1) |

3,190 U |

||

|

Postage |

1,470 |

1,960 (2) |

490 U |

||

|

Fixed expenses |

|||||

|

Facility |

1,000 |

1,500 (3) |

500 U |

||

|

Printing |

950 |

950 |

0 |

||

|

Decorations |

840 |

840 |

0 |

||

|

Speaker's gift |

130 |

130 |

0 |

||

|

Publicity |

600 |

600 |

0 |

||

|

Total expenses |

25,290 |

29,470 |

4,180 U |

||

|

Surplus(deficit) |

$ 0 |

$ (4,180) |

$ 4,180 U |

||

(1) 1,620 x $14.50 = $23,490

(2) 4,000 x $0.49 = $1,960

(3) Higher charge due to higher attendance

b.

|

Flexible Budget |

- |

Actual Results |

= |

Flexible Variances |

|

|

Allocated funds |

$25,290 |

$25,290 |

$0 |

||

|

Expenses: |

|||||

|

Variable costs: |

|||||

|

Meals |

23,490 |

25,110 |

1,620 U |

||

|

Postage |

1,960 |

1,960 |

0 |

||

|

Fixed costs: |

|||||

|

Facility |

1,500 |

1,500 |

0 |

||

|

Printing |

950 |

950 |

0 |

||

|

Decorations |

840 |

840 |

0 |

||

|

Speaker's gift |

130 |

130 |

0 |

||

|

Publicity |

600 |

600 |

0 |

||

|

Total expenses |

29,470 |

31,090 |

1,620 U |

||

|

Surplus (deficit) |

$ (4,180) |

$ (5,800) |

$1,620 U |

||

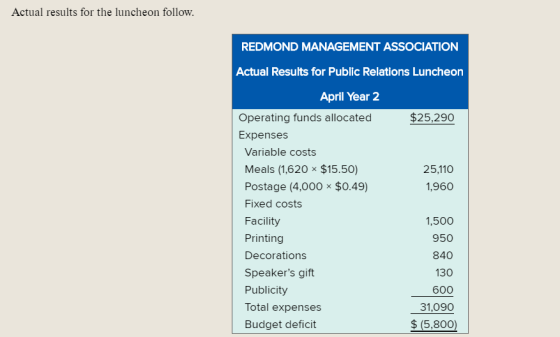

c. The $4,810 ($25,110 - $20,300) variance associated with meal cost is due to two factors. As indicated by the volume variance computed in Requirement a, $3,190 of the variance was due to higher than expected attendance. The higher attendance was caused by Mr. Snow's decision to increase the invitation list to include former members. As indicated by the flexible budget variance computed in Requirement b only $1,620 of the total variance was due to adding the dessert thereby increasing meal cost. The increase in the invitation list and the resultant increase in attendance also caused postage and facility costs to be over budget. In summary Mr. Snow is responsible for the $4,180 volume variance computed in Requirement a, while Ms. Hubbard is responsible for the $1,620 flexible budget variance computed in Requirement b. These two variances combined equal the total variance of $5,800. Accordingly, Mr. Snow is responsible for a far greater portion of the total variance than is Ms. Hubbard.

d. The members of the organization are certainly concerned with the control of costs. The costs incurred by the organization are ultimately related to the dues charged to members. Not-for-profit entities are responsible for the effective utilization of resources. Acco

Add Answer to:

1. Prepare a flexible

budget.

2. Compute the sales volume

variance and the variable cost volume...

The Rooney Management Association held its annual public relations luncheon in April Year 2. Based on...

The Rooney Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $27,938 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $13.10. The cost...

The Rooney Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $27,938 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $13.10. The cost...

The Munoz Management Association held its annual public relations luncheon in April Year 2. Based on...

The Munoz Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $26,360 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $12.80. The cost...

The Munoz Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $26,360 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $12.80. The cost...

The Adams Management Association held its annual public relations luncheon in April 2017. Based on the...

The Adams Management Association held its annual public relations luncheon in April 2017. Based on the previous year’s results, the organization allocated $21,842 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. The meal cost per person was expected to be $11.90. The cost driver for meals...

The Stuart Management Association held its annual public relations luncheon in April 2017. Based on the...

The Stuart Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the ted $29,010 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $13.30. The cost driver for meals...

The Stuart Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the ted $29,010 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $13.30. The cost driver for meals...

The Baird Management Association held its annual public relations luncheon in April 2017. Based o...

The Baird Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the organization allocated $22,328 of its operating budget to cover the cost of the luncheon, To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $12.00. The cost driver for...

The Baird Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the organization allocated $22,328 of its operating budget to cover the cost of the luncheon, To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $12.00. The cost driver for...

Actual Results Flexible Budget Variance Flexible Budget Sales Volume Static Variance Budget Units 12,000 12,000 15,000...

Actual Results Flexible Budget Variance Flexible Budget Sales Volume Static Variance Budget Units 12,000 12,000 15,000 S Sales Revenue $ 2,52,000 12,000 | F | $ 2,40,000 60,000 $3,00,000 Less: Variable Expenses 84,000 12,000F 96,000 24,000 F S 1,20,000 Contribution margin $1,68,000 24,000 $1,44,000 36,000 U $1,80,000 S Less: Fixed Expenses $ 1,50,000 5,000 $1,45,000 None S 1,45,000 Operating Income / (loss) $ 18,000 19,000 FS -1,000 36,000 U S 35,000 Look at the two outside columns - how was...

Actual Results Flexible Budget Variance Flexible Budget Sales Volume Static Variance Budget Units 12,000 12,000 15,000 S Sales Revenue $ 2,52,000 12,000 | F | $ 2,40,000 60,000 $3,00,000 Less: Variable Expenses 84,000 12,000F 96,000 24,000 F S 1,20,000 Contribution margin $1,68,000 24,000 $1,44,000 36,000 U $1,80,000 S Less: Fixed Expenses $ 1,50,000 5,000 $1,45,000 None S 1,45,000 Operating Income / (loss) $ 18,000 19,000 FS -1,000 36,000 U S 35,000 Look at the two outside columns - how was...

Prepare a flexible budget in Excel for Vroom-Vroom. (36 points) Show the flexible budget for December...

Prepare a flexible budget in Excel for Vroom-Vroom. (36 points) Show the flexible budget for December in Contribution Margin Income Statement format. Compare December’s flexible budget to December’s actual results. Specify which line items are favorable or unfavorable and how much. For Ingredient Costs and Packaging Costs, break out the Price and Volume Variances for December. Provide potential explanations Show the flexible budget for January in Contribution Margin Income Statement format. Compare January’s flexible budget to January’s actual results. Specify...

Match each form to the correct definition Terms a. Flexible budget b. Flexible budget variance c....

Match each form to the correct definition Terms a. Flexible budget b. Flexible budget variance c. Sales volume variance d Static budget e. Variance - Definitions 1. A summarized budget for several levels of volume that separates variable costs from foxed costs 2. A budget prepared for only one level of sales 3. The difference between an actual amount and the budgeted amount 4. The difference arising because the company actually earned more or less revenue, or incurred more or...

Match each form to the correct definition Terms a. Flexible budget b. Flexible budget variance c. Sales volume variance d Static budget e. Variance - Definitions 1. A summarized budget for several levels of volume that separates variable costs from foxed costs 2. A budget prepared for only one level of sales 3. The difference between an actual amount and the budgeted amount 4. The difference arising because the company actually earned more or less revenue, or incurred more or...

Problem #2-Flexible Budget-Selling &Admin Expense Only Static Budget Budget Results Variance Flex...

Problem #2-Flexible Budget-Selling &Admin Expense Only Static Budget Budget Results Variance Flex Actual Memo: Sales Selling & Admin Expenses Variable Sales Commissions-8% of sales var Advertising Exp-3% of sales Selling Supplies Exp-1% of sales Office Supplies-2% of sales $ 3,000,000 3,738,00o $ 240,000 90,000 30,000 60,000 $ 420,000 $301,500 110,862 38,241 74,083 S 524,686 Total Variable Sell & Admin Exp Fixed Sales Salaries Sales Travel expense Advertising- fixed portion Administrative salaries Rent Exp Utilities/Phones/Internet Total Fixed Sell & Admin Exp...

Problem #2-Flexible Budget-Selling &Admin Expense Only Static Budget Budget Results Variance Flex Actual Memo: Sales Selling & Admin Expenses Variable Sales Commissions-8% of sales var Advertising Exp-3% of sales Selling Supplies Exp-1% of sales Office Supplies-2% of sales $ 3,000,000 3,738,00o $ 240,000 90,000 30,000 60,000 $ 420,000 $301,500 110,862 38,241 74,083 S 524,686 Total Variable Sell & Admin Exp Fixed Sales Salaries Sales Travel expense Advertising- fixed portion Administrative salaries Rent Exp Utilities/Phones/Internet Total Fixed Sell & Admin Exp...

Master Master Budget Variance Actual 60,500 Budget 57,000 Sales volume (number of cases sold) Sales revenue...

Master Master Budget Variance Actual 60,500 Budget 57,000 Sales volume (number of cases sold) Sales revenue Less: Variable expenses Contribution margin Less: Fixed expenses $ 193,700 $ 71,200 176,700 62,700 $ 122,500 $ 73,200 114,000 72,000 $ 49,300 $ 42,000 Operating income The budgeted sales price per unit is $ 3.10 Requirement 2. What is the budgeted variable expense per unit? The budgeted variable expense per unit is $ 1.10. Requirement 3. What is the budgeted fixed cost for the...

Master Master Budget Variance Actual 60,500 Budget 57,000 Sales volume (number of cases sold) Sales revenue Less: Variable expenses Contribution margin Less: Fixed expenses $ 193,700 $ 71,200 176,700 62,700 $ 122,500 $ 73,200 114,000 72,000 $ 49,300 $ 42,000 Operating income The budgeted sales price per unit is $ 3.10 Requirement 2. What is the budgeted variable expense per unit? The budgeted variable expense per unit is $ 1.10. Requirement 3. What is the budgeted fixed cost for the...

The Rooney Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $27,938 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $13.10. The cost...

The Rooney Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $27,938 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $13.10. The cost...

The Munoz Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $26,360 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $12.80. The cost...

The Munoz Management Association held its annual public relations luncheon in April Year 2. Based on the previous year's results, the organization allocated $26,360 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon. The budget for the luncheon was based on the following expectations: 1. The meal cost per person was expected to be $12.80. The cost...

The Stuart Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the ted $29,010 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $13.30. The cost driver for meals...

The Stuart Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the ted $29,010 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $13.30. The cost driver for meals...

The Baird Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the organization allocated $22,328 of its operating budget to cover the cost of the luncheon, To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $12.00. The cost driver for...

The Baird Management Association held its annual public relations luncheon in April 2017. Based on the previous year's results, the organization allocated $22,328 of its operating budget to cover the cost of the luncheon, To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the 2017 luncheon. The budget for the luncheon was based on the following expectations. 1. The meal cost per person was expected to be $12.00. The cost driver for...

Actual Results Flexible Budget Variance Flexible Budget Sales Volume Static Variance Budget Units 12,000 12,000 15,000 S Sales Revenue $ 2,52,000 12,000 | F | $ 2,40,000 60,000 $3,00,000 Less: Variable Expenses 84,000 12,000F 96,000 24,000 F S 1,20,000 Contribution margin $1,68,000 24,000 $1,44,000 36,000 U $1,80,000 S Less: Fixed Expenses $ 1,50,000 5,000 $1,45,000 None S 1,45,000 Operating Income / (loss) $ 18,000 19,000 FS -1,000 36,000 U S 35,000 Look at the two outside columns - how was...

Actual Results Flexible Budget Variance Flexible Budget Sales Volume Static Variance Budget Units 12,000 12,000 15,000 S Sales Revenue $ 2,52,000 12,000 | F | $ 2,40,000 60,000 $3,00,000 Less: Variable Expenses 84,000 12,000F 96,000 24,000 F S 1,20,000 Contribution margin $1,68,000 24,000 $1,44,000 36,000 U $1,80,000 S Less: Fixed Expenses $ 1,50,000 5,000 $1,45,000 None S 1,45,000 Operating Income / (loss) $ 18,000 19,000 FS -1,000 36,000 U S 35,000 Look at the two outside columns - how was...

Match each form to the correct definition Terms a. Flexible budget b. Flexible budget variance c. Sales volume variance d Static budget e. Variance - Definitions 1. A summarized budget for several levels of volume that separates variable costs from foxed costs 2. A budget prepared for only one level of sales 3. The difference between an actual amount and the budgeted amount 4. The difference arising because the company actually earned more or less revenue, or incurred more or...

Match each form to the correct definition Terms a. Flexible budget b. Flexible budget variance c. Sales volume variance d Static budget e. Variance - Definitions 1. A summarized budget for several levels of volume that separates variable costs from foxed costs 2. A budget prepared for only one level of sales 3. The difference between an actual amount and the budgeted amount 4. The difference arising because the company actually earned more or less revenue, or incurred more or...

Problem #2-Flexible Budget-Selling &Admin Expense Only Static Budget Budget Results Variance Flex Actual Memo: Sales Selling & Admin Expenses Variable Sales Commissions-8% of sales var Advertising Exp-3% of sales Selling Supplies Exp-1% of sales Office Supplies-2% of sales $ 3,000,000 3,738,00o $ 240,000 90,000 30,000 60,000 $ 420,000 $301,500 110,862 38,241 74,083 S 524,686 Total Variable Sell & Admin Exp Fixed Sales Salaries Sales Travel expense Advertising- fixed portion Administrative salaries Rent Exp Utilities/Phones/Internet Total Fixed Sell & Admin Exp...

Problem #2-Flexible Budget-Selling &Admin Expense Only Static Budget Budget Results Variance Flex Actual Memo: Sales Selling & Admin Expenses Variable Sales Commissions-8% of sales var Advertising Exp-3% of sales Selling Supplies Exp-1% of sales Office Supplies-2% of sales $ 3,000,000 3,738,00o $ 240,000 90,000 30,000 60,000 $ 420,000 $301,500 110,862 38,241 74,083 S 524,686 Total Variable Sell & Admin Exp Fixed Sales Salaries Sales Travel expense Advertising- fixed portion Administrative salaries Rent Exp Utilities/Phones/Internet Total Fixed Sell & Admin Exp...

Master Master Budget Variance Actual 60,500 Budget 57,000 Sales volume (number of cases sold) Sales revenue Less: Variable expenses Contribution margin Less: Fixed expenses $ 193,700 $ 71,200 176,700 62,700 $ 122,500 $ 73,200 114,000 72,000 $ 49,300 $ 42,000 Operating income The budgeted sales price per unit is $ 3.10 Requirement 2. What is the budgeted variable expense per unit? The budgeted variable expense per unit is $ 1.10. Requirement 3. What is the budgeted fixed cost for the...

Master Master Budget Variance Actual 60,500 Budget 57,000 Sales volume (number of cases sold) Sales revenue Less: Variable expenses Contribution margin Less: Fixed expenses $ 193,700 $ 71,200 176,700 62,700 $ 122,500 $ 73,200 114,000 72,000 $ 49,300 $ 42,000 Operating income The budgeted sales price per unit is $ 3.10 Requirement 2. What is the budgeted variable expense per unit? The budgeted variable expense per unit is $ 1.10. Requirement 3. What is the budgeted fixed cost for the...

Most questions answered within 3 hours.

-

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 28 minutes ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 2 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 2 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 4 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 4 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 4 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 4 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 4 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 4 hours ago -

The cliché we use quite a lot in finance is: there is a need to

maximize...

asked 4 hours ago -

In class we discussed the addition of HCl to alpha pinene. Would

you expect one or...

asked 4 hours ago -

I'm trying to explain to my daughter to help her please help

me

I tagged the...

asked 4 hours ago