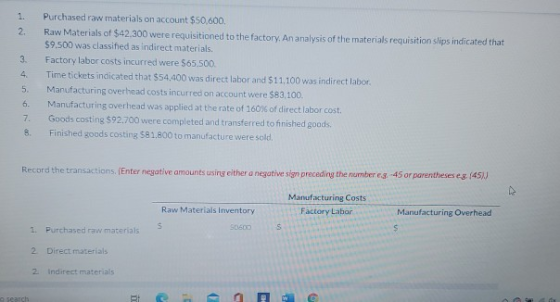

1. Purchased raw materials on account $50,600.

2. Raw Materials of $42.300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9.500 was classified as indirect materials.

3. Factory labor costs incurred were $65.500.

4. Time tickets indicated that $54,400 was direct labor and $11,100 was indirect labor.

5. Manufacturing overhead costs incurred on account were $83,100.

6. Manufacturing overhead was applied at the rate of 160% of direct labor cost.

7. Goods costing $92.700 were completed and transferred to fnished goods.

8. Finished goods costing S81.800 to manufacture were sold.

Homework Answers

Request Answer!

We need at least 10 more requests to produce the answer.

0 / 10 have requested this problem solution

The more requests, the faster the answer.

Crawford Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $50,600....

Crawford Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $50,600. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,500 was classified as indirect materials. Factory labor costs incurred were $65,500, of which $50,900 pertained to factory wages payable and $14,600 pertained to employer payroll taxes payable. Time tickets indicated that $54,400 was direct labor and $11,100 was indirect labor. Manufacturing overhead costs incurred on...

Crawford Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $50,600. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,500 was classified as indirect materials. Factory labor costs incurred were $65,500, of which $50,900 pertained to factory wages payable and $14,600 pertained to employer payroll taxes payable. Time tickets indicated that $54,400 was direct labor and $11,100 was indirect labor. Manufacturing overhead costs incurred on...

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,000. 2. Raw Materials...

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,000. 2. Raw Materials of $41,800 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,700 was classified as indirect materials. 3. Factory labor costs incurred were $60,500, of which $50,600 pertained to factory wages payable and $9,900 pertained to employer payroll taxes payable. 4. Time tickets indicated that $54,800 was direct labor and $5,700 was indirect labor. 5. Manufacturing overhead costs incurred...

1. 2. Crane Corporation incurred the following transactions. Purchased raw materials on account $46,400. Raw Materials...

1. 2. Crane Corporation incurred the following transactions. Purchased raw materials on account $46,400. Raw Materials of $36,100 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $6,900 was classified as indirect materials. Factory labor costs incurred were $60,000. Time tickets indicated that $54,100 was direct labor and $5,900 was indirect labor. Manufacturing overhead costs incurred on account were $81,500. Manufacturing overhead was applied at the rate of 150% of direct labor cost. Goods costing...

1. 2. Crane Corporation incurred the following transactions. Purchased raw materials on account $46,400. Raw Materials of $36,100 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $6,900 was classified as indirect materials. Factory labor costs incurred were $60,000. Time tickets indicated that $54,100 was direct labor and $5,900 was indirect labor. Manufacturing overhead costs incurred on account were $81,500. Manufacturing overhead was applied at the rate of 150% of direct labor cost. Goods costing...

Crawford Corporation incurred the following transactions. Purchased raw materials on account $46,300. Raw materials of $36,000...

Crawford Corporation incurred the following transactions. Purchased raw materials on account $46,300. Raw materials of $36,000 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $6,800 was classified as indirect materials. Factory labor costs incurred were $59,900, of which $51,000 pertained to factory wages payable and $8,900 pertained to employer payroll taxes payable. Time tickets indicated that $54,000 was direct labor and $5,900 was indirect labor. Manufacturing overhead costs incurred on account were $80,500. Depreciation...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $46,600. 2. Raw Materials...

Sheridan Corporation incurred the following transactions. 1.

Purchased raw materials on account $46,600. 2. Raw Materials of

$40,800 were requisitioned to the factory. An analysis of the

materials requisition slips indicated that $7,000 was classified as

indirect materials. 3. Factory labor costs incurred were $60,300.

4. Time tickets indicated that $55,700 was direct labor and $4,600

was indirect labor. 5. Manufacturing overhead costs incurred on

account were $83,700. 6. Manufacturing overhead was applied at the

rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1.

Purchased raw materials on account $46,600. 2. Raw Materials of

$40,800 were requisitioned to the factory. An analysis of the

materials requisition slips indicated that $7,000 was classified as

indirect materials. 3. Factory labor costs incurred were $60,300.

4. Time tickets indicated that $55,700 was direct labor and $4,600

was indirect labor. 5. Manufacturing overhead costs incurred on

account were $83,700. 6. Manufacturing overhead was applied at the

rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $51,800. 2 Raw Materials...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $51,800. 2 Raw Materials of $45,000 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,000 was classified as indirect materials. 3. Factory labor costs incurred were $64,100. 4. Time tickets indicated that $54,900 was direct labor and $9,200 was indirect labor. 5. Manufacturing overhead costs incurred on account were $83,600. 6. Manufacturing overhead was applied at the rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $51,800. 2 Raw Materials of $45,000 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,000 was classified as indirect materials. 3. Factory labor costs incurred were $64,100. 4. Time tickets indicated that $54,900 was direct labor and $9,200 was indirect labor. 5. Manufacturing overhead costs incurred on account were $83,600. 6. Manufacturing overhead was applied at the rate of 160% of direct...

Exercise 15-7 Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $51,000. 2....

Exercise 15-7 Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $51,000. 2. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,800 was classified as indirect materials. 3. Factory labor costs incurred were $66,200, of which $50,600 pertained to factory wages payable and $15,600 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,000 was direct labor and $11,200 was indirect labor. 5. Manufacturing overhead...

Exercise 15-7 Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $51,000. 2. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,800 was classified as indirect materials. 3. Factory labor costs incurred were $66,200, of which $50,600 pertained to factory wages payable and $15,600 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,000 was direct labor and $11,200 was indirect labor. 5. Manufacturing overhead...

Oriole Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $54,500....

Oriole Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $54,500. Raw Materials of $38,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,000 was classified as indirect materials. Factory labor costs incurred were $62,500. Time tickets indicated that $54,700 was direct labor and $7,800 was indirect labor. Manufacturing overhead costs incurred on account were $84,900. Manufacturing overhead was applied at the rate of 150% of direct labor cost....

Oriole Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $54,500. Raw Materials of $38,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,000 was classified as indirect materials. Factory labor costs incurred were $62,500. Time tickets indicated that $54,700 was direct labor and $7,800 was indirect labor. Manufacturing overhead costs incurred on account were $84,900. Manufacturing overhead was applied at the rate of 150% of direct labor cost....

Sheffield Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $53,800....

Sheffield Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $53,800. Raw Materials of $36,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,500 was classified as indirect materials. Factory labor costs incurred were $61,900. Time tickets indicated that $54,900 was direct labor and $7,000 was indirect labor. Manufacturing overhead costs incurred on account were $82,300. Manufacturing overhead was applied at the rate of 160% of direct labor cost....

Sheffield Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $53,800. Raw Materials of $36,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,500 was classified as indirect materials. Factory labor costs incurred were $61,900. Time tickets indicated that $54,900 was direct labor and $7,000 was indirect labor. Manufacturing overhead costs incurred on account were $82,300. Manufacturing overhead was applied at the rate of 160% of direct labor cost....

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,600. 2. Raw Materials...

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,600. 2. Raw Materials of $44,800 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,600 was classified as indirect materials. 3. Factory labor costs incurred were $66,300, of which $51,500 pertained to factory wages payable and $14,800 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,200 was direct labor and $11,100 was indirect labor. 5. Manufacturing overhead costs incurred...

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,600. 2. Raw Materials of $44,800 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,600 was classified as indirect materials. 3. Factory labor costs incurred were $66,300, of which $51,500 pertained to factory wages payable and $14,800 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,200 was direct labor and $11,100 was indirect labor. 5. Manufacturing overhead costs incurred...

Crawford Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $50,600. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,500 was classified as indirect materials. Factory labor costs incurred were $65,500, of which $50,900 pertained to factory wages payable and $14,600 pertained to employer payroll taxes payable. Time tickets indicated that $54,400 was direct labor and $11,100 was indirect labor. Manufacturing overhead costs incurred on...

Crawford Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $50,600. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,500 was classified as indirect materials. Factory labor costs incurred were $65,500, of which $50,900 pertained to factory wages payable and $14,600 pertained to employer payroll taxes payable. Time tickets indicated that $54,400 was direct labor and $11,100 was indirect labor. Manufacturing overhead costs incurred on...

1. 2. Crane Corporation incurred the following transactions. Purchased raw materials on account $46,400. Raw Materials of $36,100 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $6,900 was classified as indirect materials. Factory labor costs incurred were $60,000. Time tickets indicated that $54,100 was direct labor and $5,900 was indirect labor. Manufacturing overhead costs incurred on account were $81,500. Manufacturing overhead was applied at the rate of 150% of direct labor cost. Goods costing...

1. 2. Crane Corporation incurred the following transactions. Purchased raw materials on account $46,400. Raw Materials of $36,100 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $6,900 was classified as indirect materials. Factory labor costs incurred were $60,000. Time tickets indicated that $54,100 was direct labor and $5,900 was indirect labor. Manufacturing overhead costs incurred on account were $81,500. Manufacturing overhead was applied at the rate of 150% of direct labor cost. Goods costing...

Sheridan Corporation incurred the following transactions. 1.

Purchased raw materials on account $46,600. 2. Raw Materials of

$40,800 were requisitioned to the factory. An analysis of the

materials requisition slips indicated that $7,000 was classified as

indirect materials. 3. Factory labor costs incurred were $60,300.

4. Time tickets indicated that $55,700 was direct labor and $4,600

was indirect labor. 5. Manufacturing overhead costs incurred on

account were $83,700. 6. Manufacturing overhead was applied at the

rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1.

Purchased raw materials on account $46,600. 2. Raw Materials of

$40,800 were requisitioned to the factory. An analysis of the

materials requisition slips indicated that $7,000 was classified as

indirect materials. 3. Factory labor costs incurred were $60,300.

4. Time tickets indicated that $55,700 was direct labor and $4,600

was indirect labor. 5. Manufacturing overhead costs incurred on

account were $83,700. 6. Manufacturing overhead was applied at the

rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $51,800. 2 Raw Materials of $45,000 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,000 was classified as indirect materials. 3. Factory labor costs incurred were $64,100. 4. Time tickets indicated that $54,900 was direct labor and $9,200 was indirect labor. 5. Manufacturing overhead costs incurred on account were $83,600. 6. Manufacturing overhead was applied at the rate of 160% of direct...

Sheridan Corporation incurred the following transactions. 1. Purchased raw materials on account $51,800. 2 Raw Materials of $45,000 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,000 was classified as indirect materials. 3. Factory labor costs incurred were $64,100. 4. Time tickets indicated that $54,900 was direct labor and $9,200 was indirect labor. 5. Manufacturing overhead costs incurred on account were $83,600. 6. Manufacturing overhead was applied at the rate of 160% of direct...

Exercise 15-7 Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $51,000. 2. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,800 was classified as indirect materials. 3. Factory labor costs incurred were $66,200, of which $50,600 pertained to factory wages payable and $15,600 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,000 was direct labor and $11,200 was indirect labor. 5. Manufacturing overhead...

Exercise 15-7 Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $51,000. 2. Raw Materials of $42,300 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,800 was classified as indirect materials. 3. Factory labor costs incurred were $66,200, of which $50,600 pertained to factory wages payable and $15,600 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,000 was direct labor and $11,200 was indirect labor. 5. Manufacturing overhead...

Oriole Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $54,500. Raw Materials of $38,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,000 was classified as indirect materials. Factory labor costs incurred were $62,500. Time tickets indicated that $54,700 was direct labor and $7,800 was indirect labor. Manufacturing overhead costs incurred on account were $84,900. Manufacturing overhead was applied at the rate of 150% of direct labor cost....

Oriole Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $54,500. Raw Materials of $38,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,000 was classified as indirect materials. Factory labor costs incurred were $62,500. Time tickets indicated that $54,700 was direct labor and $7,800 was indirect labor. Manufacturing overhead costs incurred on account were $84,900. Manufacturing overhead was applied at the rate of 150% of direct labor cost....

Sheffield Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $53,800. Raw Materials of $36,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,500 was classified as indirect materials. Factory labor costs incurred were $61,900. Time tickets indicated that $54,900 was direct labor and $7,000 was indirect labor. Manufacturing overhead costs incurred on account were $82,300. Manufacturing overhead was applied at the rate of 160% of direct labor cost....

Sheffield Corporation incurred the following transactions. 1. 2. 3. 4. Purchased raw materials on account $53,800. Raw Materials of $36,500 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $8,500 was classified as indirect materials. Factory labor costs incurred were $61,900. Time tickets indicated that $54,900 was direct labor and $7,000 was indirect labor. Manufacturing overhead costs incurred on account were $82,300. Manufacturing overhead was applied at the rate of 160% of direct labor cost....

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,600. 2. Raw Materials of $44,800 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,600 was classified as indirect materials. 3. Factory labor costs incurred were $66,300, of which $51,500 pertained to factory wages payable and $14,800 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,200 was direct labor and $11,100 was indirect labor. 5. Manufacturing overhead costs incurred...

Crawford Corporation incurred the following transactions. 1. Purchased raw materials on account $53,600. 2. Raw Materials of $44,800 were requisitioned to the factory. An analysis of the materials requisition slips indicated that $9,600 was classified as indirect materials. 3. Factory labor costs incurred were $66,300, of which $51,500 pertained to factory wages payable and $14,800 pertained to employer payroll taxes payable. 4. Time tickets indicated that $55,200 was direct labor and $11,100 was indirect labor. 5. Manufacturing overhead costs incurred...

Most questions answered within 3 hours.

-

What mechanisms Drive speciation??

(I.e. what was Dawins theory on the orgin of species, and how...

asked 17 minutes ago -

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 1 hour ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 2 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 3 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 5 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 5 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 5 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 5 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 5 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 5 hours ago -

The cliché we use quite a lot in finance is: there is a need to

maximize...

asked 5 hours ago -

In class we discussed the addition of HCl to alpha pinene. Would

you expect one or...

asked 5 hours ago