Consider a bond that has a 30-year maturity, an 8% coupon rate, and sells at an...

- Consider a bond that has a 30-year maturity, an 8% coupon rate, and sells at an initial yield to maturity of 8%. Because the coupon rate equals the yield to maturity, the bond sells at par value: P = $1,000.00. Calculate the duration and the modified duration. If we assume the convexity of the bond is 212.4 and the bond’s yield increases from 8% to 10%, how much should the bond price decline?

Homework Answers

| Period | Cash Flow | Discounting factor | PV Cash Flow | Duration Calc |

| 0 | ($1,000.00) | =(1+YTM/number of coupon payments in the year)^period | =cashflow/discounting factor | =PV cashflow*period |

| 1 | 80.00 | 1.08 | 74.07 | 74.07 |

| 2 | 80.00 | 1.17 | 68.59 | 137.17 |

| 3 | 80.00 | 1.26 | 63.51 | 190.52 |

| 4 | 80.00 | 1.36 | 58.80 | 235.21 |

| 5 | 80.00 | 1.47 | 54.45 | 272.23 |

| 6 | 80.00 | 1.59 | 50.41 | 302.48 |

| 7 | 80.00 | 1.71 | 46.68 | 326.75 |

| 8 | 80.00 | 1.85 | 43.22 | 345.77 |

| 9 | 80.00 | 2.00 | 40.02 | 360.18 |

| 10 | 80.00 | 2.16 | 37.06 | 370.55 |

| 11 | 80.00 | 2.33 | 34.31 | 377.42 |

| 12 | 80.00 | 2.52 | 31.77 | 381.23 |

| 13 | 80.00 | 2.72 | 29.42 | 382.41 |

| 14 | 80.00 | 2.94 | 27.24 | 381.32 |

| 15 | 80.00 | 3.17 | 25.22 | 378.29 |

| 16 | 80.00 | 3.43 | 23.35 | 373.62 |

| 17 | 80.00 | 3.70 | 21.62 | 367.57 |

| 18 | 80.00 | 4.00 | 20.02 | 360.36 |

| 19 | 80.00 | 4.32 | 18.54 | 352.20 |

| 20 | 80.00 | 4.66 | 17.16 | 343.28 |

| 21 | 80.00 | 5.03 | 15.89 | 333.74 |

| 22 | 80.00 | 5.44 | 14.72 | 323.74 |

| 23 | 80.00 | 5.87 | 13.63 | 313.38 |

| 24 | 80.00 | 6.34 | 12.62 | 302.78 |

| 25 | 80.00 | 6.85 | 11.68 | 292.04 |

| 26 | 80.00 | 7.40 | 10.82 | 281.22 |

| 27 | 80.00 | 7.99 | 10.01 | 270.40 |

| 28 | 80.00 | 8.63 | 9.27 | 259.65 |

| 29 | 80.00 | 9.32 | 8.59 | 249.00 |

| 30 | 1,080.00 | 10.06 | 107.33 | 3,219.83 |

| Total | 12,158.41 |

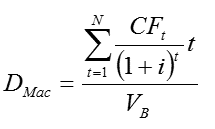

| Macaulay duration =(∑ Duration calc)/(bond price*number of coupon per year) |

| =12158.41/(1000*1) |

| =12.158406 |

| Modified duration = Macaulay duration/(1+YTM) |

| =12.16/(1+0.08) |

| =11.257783 |

| New bond price @ YTM =10 using duration | |||||||||

| Mod.duration prediction = -Mod. Duration*Yield_Change*Bond_Price | |||||||||

| =-11.2577*0.02*1000 | |||||||||

| =-225.154 | |||||||||

| New bond price = bond price+Modified duration prediction | |||||||||

| =1000+-225.154 | |||||||||

| =774.85 | |||||||||

| New bond price @ YTM =10 using duration and convexity | |||||||||

| Convexity adjustment = 0.5*convexity*Yield_Change^2*Bond_Price | |||||||||

| =0.5*212.4*0.02^2*1000 | |||||||||

| =42.48 | |||||||||

| New bond price = bond price+Mod.duration pred.+convex. Adj. | |||||||||

| =1000+-225.15+21.24 | |||||||||

| =817.33 |

Price declined by 1000-817.33=182.67

Add Answer to:

Consider a bond that has a 30-year maturity, an 8% coupon rate,

and sells at an...

Bond Y has a 30-year maturity, an 8% coupon, and sells at an initial yield-to-maturity (YTM)...

Bond Y has a 30-year maturity, an 8% coupon, and sells at an initial yield-to-maturity (YTM) of 8 percent. The modified duration of Bond Y is 11.26 years and its convexity measure equals 212.40. If the bond's yield increases from 8% to 10% how much on a percentage basis is the Duration-With- Convexity Rule more accurate (Part 1)? Briefly explain the concept of Convexity Measure as it relates to Bond Y (Part 2):

Bond Y has a 30-year maturity, an 8% coupon, and sells at an initial yield-to-maturity (YTM) of 8 percent. The modified duration of Bond Y is 11.26 years and its convexity measure equals 212.40. If the bond's yield increases from 8% to 10% how much on a percentage basis is the Duration-With- Convexity Rule more accurate (Part 1)? Briefly explain the concept of Convexity Measure as it relates to Bond Y (Part 2):

A newly issued bond has a maturity of 10 years and pays a 7.4% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.4% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7.4% to 8.4% (with maturity still 10 years). Assume...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) F...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration of 12.27 years and convexity of 216.28. The bond currently sells at a yield to maturity of 8%. e-1. Find the price of the bond if its yield to maturity increases to 9%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) e-2. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answers to...

A newly issued bond has a maturity of 10 years and pays a 5.4% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 5.4% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 5.4% to 6.4% (with maturity still 10 years). Assume...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity - 61.810 Duration - 7.330 Years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7.7% to...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 146.5 and modified duration of 11.65 years. A 30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration—-11.79 years—-but considerably higher convexity of 231.2. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

1. An investor purchases an annual coupon bond with a 6% coupon rate and exactly 20...

1. An investor purchases an annual coupon bond with a 6% coupon rate and exactly 20 years remaining until maturity at a price equal to par value. The investor’s investment horizon is eight years. The approximate modified duration of the bond is 11.470 years. What is the duration gap at the time of purchase? (Hint: use approximate Macaulay duration to calculate the duration gap) 2. An investor plans to retire in 10 years. As part of the retirement portfolio, the...

Bond Y has a 30-year maturity, an 8% coupon, and sells at an initial yield-to-maturity (YTM) of 8 percent. The modified duration of Bond Y is 11.26 years and its convexity measure equals 212.40. If the bond's yield increases from 8% to 10% how much on a percentage basis is the Duration-With- Convexity Rule more accurate (Part 1)? Briefly explain the concept of Convexity Measure as it relates to Bond Y (Part 2):

Bond Y has a 30-year maturity, an 8% coupon, and sells at an initial yield-to-maturity (YTM) of 8 percent. The modified duration of Bond Y is 11.26 years and its convexity measure equals 212.40. If the bond's yield increases from 8% to 10% how much on a percentage basis is the Duration-With- Convexity Rule more accurate (Part 1)? Briefly explain the concept of Convexity Measure as it relates to Bond Y (Part 2):

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity Duration years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7% to 8% (with maturity still...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

Most questions answered within 3 hours.

-

Write a program to solve the Josephus problem, with the following

modification:

Sample Input:

./a.out n...

asked 25 minutes ago -

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 1 hour ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 2 hours ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 3 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 3 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 3 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 4 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 4 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 4 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 4 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 4 hours ago -

Why are polymers not typically casted into products?

asked 5 hours ago