Bonds (Straight-Line Metho when a company needs to raise significant amounts of cash, one option may be to sue (sel) bonds. From the company's standpoint, this is a lot like going to the bank and getting a loan. These are the steps a company takes to borrow money by issuing bonds. 1) The company informs the necessary govenmental regulatory agencies of its plans to issue bonds. 2) The company partners with an investment banker and begins to prepare an Offering Circular Among other things, the Offering Circular acts as a marketing document for the sale of the bonds. 3) At the time the initial filings are made, a Stated rate (Coupon rate) of interest is assigned to the bond issue and recorded in the Offering Circular. This rate essentially reflects the current interest rate at the time. This is also the rate that is used to pay interest either semi-annually or annually 4) In the months (usually 3-6 months) that it takes to finish the filing process and the Offering Circular the current interest rate often fluctuates in the market place. When the date comes to finally issue (sell) the bonds to potential bondholders, the Effective rate (Market rate) of interest is often different than the Stated rate of interest 5) A bond pricing model is then used to price the bonds reflecting the difference in the Stated and Effective rates of interest at the time of issue. Prices are essentially reflected as a percentage. A bond price of 100 would indicate that there is no difference between the Stated and Effective rates of interest and the bond issues at Par Value. Premium 00Par Value Discount If the bond pricing model results in a price above 100, the bond will be issued at a Premium. If the price is below 100, the bond will be issued at a Discount Exercise Review the following completed example for a bond issued at a price of 100. A $50.000, 10 year, 9% (Stated rate) bond is issued on January 1. The bond pays interest semi-annually each January 1 and July 1. The bond's Stated rate is equal to the Effective rate at the time of issue so the bond price is 100. Review the following entries 1. Entry required upon issuance of the bond. $50,000 x 1.00 $50,000 2. Entry on first interest payment date $50,000 x 9% x 6/12-$2,250 (Jan-June)

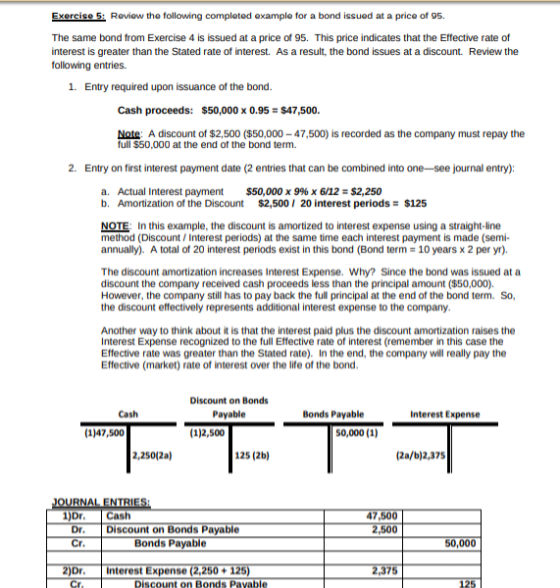

Exercise 5: Reviow the following completed example for a bond issued at a price of 95. The same bond from Exercise 4 is issued at a price of 95. This price indicates that the Effective rate of interest is greater than the Stated rate of interest. As a result, the bond issues at a discount. Review the following entries. 1. Entry required upon issuance of the bond Cash proceeds: $50,000 x 0.95 $47,500. Note: A discount of $2,500 ($50,000-47,500) is recorded as the company must repay the full $50,000 at the end of the bond term. 2. Entry on first interest payment date (2 entries that can be combined into one-see journal entry): a. Actual Interest payment $50,000 x 996 x 6/12-$2,250 b. Amortization of the Discount $2,500/ 20 interest periods-$125 NOTE: In this example, the discount is amortized to interest expense using a straight-line method (Discount/Interest periods) at the same time each interest payment is made (semi- annually). A total of 20 interest periods exist in this bond (Bond term 10 years x 2 per yr). The discount amortization increases Interest Expense. Why? Since the bond was issued at a discount the company received cash proceeds less than the principal amount ($50,000). However, the company still has to pay back the full principal at the end of the bond term. So, the discount effectively represents additional interest expense to the company Another way to think about it is that the interest paid plus the discount amortization raises the Interest Expense recognized to the full Effective rate of interest (remember in this case the Effective rate was greater than the Stated rate). In the end, the company will really pay the Effective (market) rate of interest over the life of the bond Discount on Bonds Cash Payable Bonds Payable Interest Expense (1)47,500 (1)2,500 50,000 (1 2,250(2a) 125 (2b) (2a/b)2,375 1)Dr. Cash 7,500 500 Dr Discount on ds Paya Bonds Payable Interest Expense Discount on Bonds Pavable

JOURNAL ENTRIES 1)Dr. Cash 47,500 2,500 Dr Cr Discount on Bonds Payable Bonds Payable 50,000 2)Dr. Interest Expense (2,250125) 2,375 Cr Cr Discount on Bonds Payable Cash 125 250 Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts belovw The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium. 1. Entry required upon issuance of the bond Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just $50,000 at the end of the bond term 2. Entry on first interest payment date: a. Actual Interest payment b. Amortization of the Premium %x 6/12: $ Interest periods NOTE: Much like amortizing a discount, use the total number of interest periods to amortize the premium using the straight-line method. In this case the premium amortization effectively decreases Interest Expense. Why? Once again, since the bond was issued at a premium the company received cash proceeds greater than the principal amount ($50,000), However, the company only has to pay back the principal at the end of the bond term. So, the premium received up front effectively reduces the overall interest expense to the company over the life of the bond Another way to think about it is that the interest paid combined with the premium amortization

Another way to think about it is that the interest paid combined with the premium amortization lowers the Interest Expense recognized to the full Effective rate of interest (remember in this case the Effective rate was less than the Stated rate). In the end, the company will really pay the Effective (market) rate of interest over the life of the bond. Premium on Bonds Cash Payable Bonds Payable Interest Expense QURNAL ENTRIES In the previous examples, you learned how to amortize bond premiums and discounts using a straight-ine method. However, per GAAP, the straight-line method can only be used if the results are not materially amortization amount each interest period based on the Effective (market) rate of interest. Exercise Zi Review the completed example below. Pay close attention to the table below used to A $100,000, 2 year, 11% (Stated rate) bond is sold when the Effective (market) rate is 13%. Interest is

Exercise : Review the completed exariple below. Pay cluse atterntiorn tu the table below used to calculate the discount amortization each period. A $100,000, 2 year, 11% (Stated rate) bond is sold when the Effective (market) rate is 13%. Interest is paid semi-annually. Since the Effective rate is greater than the Stated rate, the bond pricing model results in a discounted issue price of 96.643. Note: Don't try to calculate how this price is calculated at this point. You'd need to know how the bond pricing model works which we are not covering in this chapter Assuming a price of 96.643 at issuance, calculate the cash proceeds at bond issuance: 1) Entry upon issuance of bond. Cash proceeds: $100,000 x.96643 $96,643 2) Entry on first interest payment date a. Actual Interest payment $100,000 x 11% x 6/12-$5,500 b. Amortization of the discount. See table. 3) Next, record the entries for the remaining 3 interest payments and discount amortizations. Discount on Bonds Cash Bonds Payable Interest Expense 96,643 (1) ss00 (2) 3,357 (1) 782 (2) 833 (3) 887 (3) 855 (3) 100,000(1) (2a/b)6,282 5500 (3) 5500 (3) 5500 (3) (3) 6,333 (3) 6,387 (3) 6,355 1196 x $100K / | 13% x Col.E , (B - A) (D- C) ($100K D) rrying nterest rest nterest nt scount Balan 357 Amortization 96643 742 ,425 5,500 50 6,333 387 833 742 98,258 9.14 100.00 (not 6,444)(vs. (vs. 944-rounding)

Exercise 8: Complete the following problem. A $20,000, 2 year, 10% (Stated rate) bond is sold when the Effective (Market) rate is 8%. The bond pays interest semi-annually. Assuming a price of 104 at issuance record the following. 1. Entry required upon issuance of the bond. Cash proceeds:$ 2. Entry on the first interest payment date. Use STRAIGHT-LINE method for amortization. a. Actual Interest payment %x6/12 : $ b. Amortization of the Premium using the STRAIGHT-LINE method. $periods S Entry on the second interest payment date. Use STRAIGHT-LINE method for amortization. a. Actual Interest payment 3. b. Amortization of the Premium using the STRAIGHT-LINE method Premium on Bonds Cash Payable Bonds Payable Interest Expense Next, use the t-accounts below the table to repeat the same three steps (from above) but this time use the EFFECTIVE INTEREST RATE METHOD. Round any calculations to the nearest dollar 10% x S20K | 896 x Col.E (B - A) Premium Amortization (D-C) Premium Balance 800 (S20KD) Interest PymtInterest Paid Interest ise Amount Premium on Bonds Payable Cash Bonds Payable Interest Expense

Examnle 9: Review the completed example below. A company has a S500,000 callable bond with a $7,000 premium on the books. These balances are reflected in the t-accts below. The bond is retired at a price of 102. Review these steps to record the retirement entry 1) Determine how much cash must be paid and record in the T-acct. $500,000 x 1.02-$510,00o 2) Record entry to zero out the Bonds Payable account. 3) Record entry to zero out the Premium account. 4) Add up your debits and credits to this point. If you need a debit to balance out the entry, record it to a "Loss on Retirement of Bonds" account. If you need a credit to balance out the entry, record it to a "Gain on Retirement of Bonds account. In this example, a loss is recorded. Premium on Bonds Loss on Retirement of Bonds Payable 7,000 bal. bal 510,000 500,000 7,000 3,000 What if the bonds were called at a price of 101? $500,000 x 1.01- 505,000 Premium on Bonds Gain on Retirement of Bonds Cash Bonds Payable Payable 00,000 bal 7,000 bal. 505,000 500,000 7,000 2,000 Example 10 Use the t-accounts below to record the following bond retirement. A $200,000 callable bond with a $5,000 discount is called at a price of 104 Discount on Bonds Loss on Retirement of Bonds Payable 200,000 bal ,000 bal.

Homework Answers

Answer:- Exercise 1 all parts.

Add Answer to:

Payable: Use the t-accts below to record the following entries. If you get stuck, carefully revie...

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below The...

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium 1. Entry required upon issuance of the bond Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just...

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium 1. Entry required upon issuance of the bond Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just...

please solve this for me, thanks PR 14-5A Bond discount, entries for bonds payable transactions, interest...

please solve this for me, thanks

PR 14-5A Bond discount, entries for bonds payable transactions, interest method of amortizing bond discount On July 1, 2016, Merideth Industries Inc. issued $28,500,000 of 10-year, 8% bonds at a market (effective) interest rate of 9%, receiving cash of $26,646,292. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Instructions 1. Joumalize the entry to record the amount of cash...

please solve this for me, thanks

PR 14-5A Bond discount, entries for bonds payable transactions, interest method of amortizing bond discount On July 1, 2016, Merideth Industries Inc. issued $28,500,000 of 10-year, 8% bonds at a market (effective) interest rate of 9%, receiving cash of $26,646,292. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Instructions 1. Joumalize the entry to record the amount of cash...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, Year 1, Rodgers Corporation issued $65,000,000 of 10 year, 12% bonds at a market (effective) interest rate of 10%, receiving cash of $73,100,469. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries with a compound transaction, if an amount box does not require an...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, Year 1, Rodgers Corporation issued $65,000,000 of 10 year, 12% bonds at a market (effective) interest rate of 10%, receiving cash of $73,100,469. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries with a compound transaction, if an amount box does not require an...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 20Y1, Rodgers issued $67,500,000 of 10-year, 11% bonds at a market (effective) interest rate of 10%, receiving cash of $71,706,030. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Journalize the...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 20Y1, Livingston Corporation, a wholesaler of...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 20Y1, Livingston Corporation, a wholesaler of manufacturing equipment, issued $7,900,000 of 5-year, 8% bonds at a market (effective) interest rate of 10%, receiving cash of $7,289,956. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Journalize the entry...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 2041, Rodgers issued $70,600,000 of 10-year, 14% bonds at a market (effective) interest rate of 125, receiving cash of 578,697,425. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank, 1. Journalize the...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 2041, Rodgers issued $70,600,000 of 10-year, 14% bonds at a market (effective) interest rate of 125, receiving cash of 578,697,425. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank, 1. Journalize the...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 2041, Livingston Corporation, a wholesaler of...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 2041, Livingston Corporation, a wholesaler of manufacturing equipment, issued $4,000,000 of 6-year, 11% bonds at a market (effective) interest rate of 12%, receiving cash of $3,832,325. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Joumalize the entry...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 2041, Livingston Corporation, a wholesaler of manufacturing equipment, issued $4,000,000 of 6-year, 11% bonds at a market (effective) interest rate of 12%, receiving cash of $3,832,325. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Joumalize the entry...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 20Y1, Rodgers issued $48,500,000 of 10-year, 11% bonds at a market (effective) interest rate of 10%, receiving cash of $51,522,110. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Journalize the...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 20Y1, Livingston Corporation, a wholesaler of...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 20Y1, Livingston Corporation, a wholesaler of manufacturing equipment, issued $4,400,000 of 8-year, 11% bonds at a market (effective) interest rate of 12%, receiving cash of $4,177,688. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Journalize the entry...

PR.11-02.ALGo Bond Premium, Entries for Bonds Payable Transactions Campbell Inc. produces and sells outdoor equipment. On...

PR.11-02.ALGo Bond Premium, Entries for Bonds Payable Transactions Campbell Inc. produces and sells outdoor equipment. On July 1, Year 1, Campbell issued $31,800,000 of 10-year, 12% bonds at a market (effective) interest rate of 11%, receiving cash of $33,700,139. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: If an amount box does not require an entry, leave it blank. 1. Journalize the entry to...

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium 1. Entry required upon issuance of the bond Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just...

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium 1. Entry required upon issuance of the bond Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just...

please solve this for me, thanks

PR 14-5A Bond discount, entries for bonds payable transactions, interest method of amortizing bond discount On July 1, 2016, Merideth Industries Inc. issued $28,500,000 of 10-year, 8% bonds at a market (effective) interest rate of 9%, receiving cash of $26,646,292. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Instructions 1. Joumalize the entry to record the amount of cash...

please solve this for me, thanks

PR 14-5A Bond discount, entries for bonds payable transactions, interest method of amortizing bond discount On July 1, 2016, Merideth Industries Inc. issued $28,500,000 of 10-year, 8% bonds at a market (effective) interest rate of 9%, receiving cash of $26,646,292. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Instructions 1. Joumalize the entry to record the amount of cash...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, Year 1, Rodgers Corporation issued $65,000,000 of 10 year, 12% bonds at a market (effective) interest rate of 10%, receiving cash of $73,100,469. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries with a compound transaction, if an amount box does not require an...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, Year 1, Rodgers Corporation issued $65,000,000 of 10 year, 12% bonds at a market (effective) interest rate of 10%, receiving cash of $73,100,469. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries with a compound transaction, if an amount box does not require an...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 2041, Rodgers issued $70,600,000 of 10-year, 14% bonds at a market (effective) interest rate of 125, receiving cash of 578,697,425. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank, 1. Journalize the...

Bond Premium, Entries for Bonds Payable Transactions Rodgers Corporation produces and sells football equipment. On July 1, 2041, Rodgers issued $70,600,000 of 10-year, 14% bonds at a market (effective) interest rate of 125, receiving cash of 578,697,425. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank, 1. Journalize the...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 2041, Livingston Corporation, a wholesaler of manufacturing equipment, issued $4,000,000 of 6-year, 11% bonds at a market (effective) interest rate of 12%, receiving cash of $3,832,325. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Joumalize the entry...

Bond Discount, Entries for Bonds Payable Transactions On July 1, 2041, Livingston Corporation, a wholesaler of manufacturing equipment, issued $4,000,000 of 6-year, 11% bonds at a market (effective) interest rate of 12%, receiving cash of $3,832,325. Interest on the bonds is payable semiannually on December 31 and June 30. The fiscal year of the company is the calendar year. Required: For all journal entries, if an amount box does not require an entry, leave it blank. 1. Joumalize the entry...

Most questions answered within 3 hours.

-

Calculate the following: ***SHOW ALL WORK!!!! Or

NO CREDIT*** Circle your answers. 8pts

each

In the...

asked 1 hour ago -

Bank Z is currently advertising interest rates on its checking

account. They claim to pay an...

asked 1 hour ago -

List two ways of transformation on the response variable that

can be used to deal with...

asked 2 hours ago -

If a 2000 ohm resistor has a -3.90 mA current going through it.

What is the...

asked 2 hours ago -

Please comment on the sentences.

Some types of jobs require more training than others. Some

companies...

asked 3 hours ago -

The )G01 for the hydrolysis of phosphorarginine

reaction depicted below is –32 kJ mol-1.

Phosphoarginine ...

asked 3 hours ago -

Cross a heterozygous blue-eyed goat with a homozygous brown-eyed

goat. Be sure to indicate which kids...

asked 4 hours ago -

Use the following information to answer the next two

questions.

Please refer to question 9-90. A...

asked 4 hours ago -

A solution containing 0.050 g of an unknown electrolyte in 2.50

g of cyclohexane was found...

asked 4 hours ago -

Question 1

a) Hydraulic conductivity of soils is an important parameter for

the design of engineering...

asked 4 hours ago -

Suppose your credit card balance is

$15,000

The minimum payment is

$313

and the annual percentage...

asked 4 hours ago -

Professor plays basketball and makes 75% of free

throws she shoots. If professor shot 5 free...

asked 4 hours ago