Homework Answers

Add Answer to:

An investor is faced with two risky asset portfolios (each of which is highly diversified within ...

An investor is faced with two risky asset portfolios (each of which is highly diversified within ...

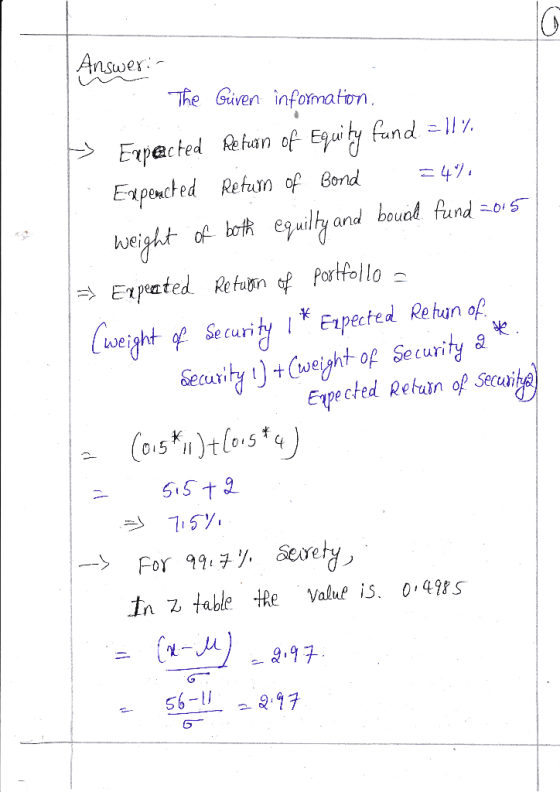

An investor is faced with two risky asset portfolios (each of which is highly diversified within its asset class) an equity fund and a bond fund. The investor is aware that asset returns are not always normally distributed, but is nonetheless prepared to use the normal distribution as a tool for the estimation of approximate portfolio risks and expected returns. The equity fund has a forecast expected return of +11 % pa over the time horizon of 12 months, and...

An investor is faced with two risky asset portfolios (each of which is highly diversified within its asset class) an equity fund and a bond fund. The investor is aware that asset returns are not always normally distributed, but is nonetheless prepared to use the normal distribution as a tool for the estimation of approximate portfolio risks and expected returns. The equity fund has a forecast expected return of +11 % pa over the time horizon of 12 months, and...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 an...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5 % , and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6 % If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5 % , and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6 % If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5%, and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6%. If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each investor's combined bond...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5%, and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6%. If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each investor's combined bond...

3 Different investor weights. Two risky portfolios exist for investing: one is a bond th a...

3 Different investor weights. Two risky portfolios exist for investing: one is a bond th a beta of 0.5 and an expected return of 8%, and the other portfolio wi uity portfolio with a beta of 1.2 and an expected return of 15%. If these portfolios are the only two available assets for investing, what combination of these two as- sets will give the following investors their desired level of expected return? What are the betas of each investor's combination...

3 Different investor weights. Two risky portfolios exist for investing: one is a bond th a beta of 0.5 and an expected return of 8%, and the other portfolio wi uity portfolio with a beta of 1.2 and an expected return of 15%. If these portfolios are the only two available assets for investing, what combination of these two as- sets will give the following investors their desired level of expected return? What are the betas of each investor's combination...

You are an investment manager considering two mutual funds. The first is an equity fund and...

You are an investment manager considering two mutual funds. The first is an equity fund and the second is a long- term corporate bond fund. It is possible to borrow or to lend limitless sums safely at 1.25%pa. The data on the risky funds are as follows: Fund Expected return Expected standard deviation Equity Fund 8% 16% Bond Fund 3% 5% The correlation coefficient between the fund returns is 0.10 a You form a risky portfolio P that is equally...

You are an investment manager considering two mutual funds. The first is an equity fund and the second is a long- term corporate bond fund. It is possible to borrow or to lend limitless sums safely at 1.25%pa. The data on the risky funds are as follows: Fund Expected return Expected standard deviation Equity Fund 8% 16% Bond Fund 3% 5% The correlation coefficient between the fund returns is 0.10 a You form a risky portfolio P that is equally...

You are constructing a risky portfolio for a client, to be comprised of both an equity...

You

are constructing a risky portfolio for a client, to be comprised of

both an equity fund and a bond fund. The probability distributions

of the two funds are guven below. The correlation between the two

funds is 0.10.

QUESTION 11

11.) For an investor with a risk-acersion score (A) of 4,

identify the portfolio he woud rationally select.

a) what is the expected return of this portfolio?

b) what is the standard devistion of this portfolio?

Use the following...

You

are constructing a risky portfolio for a client, to be comprised of

both an equity fund and a bond fund. The probability distributions

of the two funds are guven below. The correlation between the two

funds is 0.10.

QUESTION 11

11.) For an investor with a risk-acersion score (A) of 4,

identify the portfolio he woud rationally select.

a) what is the expected return of this portfolio?

b) what is the standard devistion of this portfolio?

Use the following...

An investor invests 40% of her wealth in a risky asset with an expected rate of...

An investor invests 40% of her wealth in a risky asset with an expected rate of return of 15% and a standard deviation of 20%. The rest of her wealth is invested in the risk-free asset, which yields 6%. What are the expected return and standard deviation of her portfolio?

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 14% and a standard deviation of return of 24.0%. Stock B has an expected return of 10% and a standard deviation of return of 4%. The correlation coefficient between the returns of A and B is 0.50. The risk-free rate of return is 8%. The proportion of the optimal risky portfolio that should be invested in stock A is...

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 45% and a standard deviation of return of 9%. Stock B has an expected return of 15% and a standard deviation of return of 2%.The correlation coefficient between the returns of A and B is 0.0025. The risk-free rate of return is 2%. The standard deviation of return on the minimum variance portfolio is _________.

Show work in excel please An investor can design a risky portfolio based on two stocks,...

Show work in excel please An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 19% and a standard deviation of return of 15.0%. Stock B has an expected return of 15% and a standard deviation of return of 6%. The correlation coefficient between the returns of A and B is 0.80. The risk-free rate of return is 11%. The proportion of the optimal risky portfolio that should be...

An investor is faced with two risky asset portfolios (each of which is highly diversified within its asset class) an equity fund and a bond fund. The investor is aware that asset returns are not always normally distributed, but is nonetheless prepared to use the normal distribution as a tool for the estimation of approximate portfolio risks and expected returns. The equity fund has a forecast expected return of +11 % pa over the time horizon of 12 months, and...

An investor is faced with two risky asset portfolios (each of which is highly diversified within its asset class) an equity fund and a bond fund. The investor is aware that asset returns are not always normally distributed, but is nonetheless prepared to use the normal distribution as a tool for the estimation of approximate portfolio risks and expected returns. The equity fund has a forecast expected return of +11 % pa over the time horizon of 12 months, and...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5 % , and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6 % If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5 % , and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6 % If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5%, and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6%. If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each investor's combined bond...

Different investor weights. Two risky portfolios exist for investing: one is a bond portfolio with a beta of 0.7 and an expected return of 6.5%, and the other is an equity portfolio with a beta of 1.4 and an expected return of 16.6%. If these portfolios are the only two available assets for investing, what combination of these two assets will give the following investors their desired level of expected return? What is the beta of each investor's combined bond...

3 Different investor weights. Two risky portfolios exist for investing: one is a bond th a beta of 0.5 and an expected return of 8%, and the other portfolio wi uity portfolio with a beta of 1.2 and an expected return of 15%. If these portfolios are the only two available assets for investing, what combination of these two as- sets will give the following investors their desired level of expected return? What are the betas of each investor's combination...

3 Different investor weights. Two risky portfolios exist for investing: one is a bond th a beta of 0.5 and an expected return of 8%, and the other portfolio wi uity portfolio with a beta of 1.2 and an expected return of 15%. If these portfolios are the only two available assets for investing, what combination of these two as- sets will give the following investors their desired level of expected return? What are the betas of each investor's combination...

You are an investment manager considering two mutual funds. The first is an equity fund and the second is a long- term corporate bond fund. It is possible to borrow or to lend limitless sums safely at 1.25%pa. The data on the risky funds are as follows: Fund Expected return Expected standard deviation Equity Fund 8% 16% Bond Fund 3% 5% The correlation coefficient between the fund returns is 0.10 a You form a risky portfolio P that is equally...

You are an investment manager considering two mutual funds. The first is an equity fund and the second is a long- term corporate bond fund. It is possible to borrow or to lend limitless sums safely at 1.25%pa. The data on the risky funds are as follows: Fund Expected return Expected standard deviation Equity Fund 8% 16% Bond Fund 3% 5% The correlation coefficient between the fund returns is 0.10 a You form a risky portfolio P that is equally...

You

are constructing a risky portfolio for a client, to be comprised of

both an equity fund and a bond fund. The probability distributions

of the two funds are guven below. The correlation between the two

funds is 0.10.

QUESTION 11

11.) For an investor with a risk-acersion score (A) of 4,

identify the portfolio he woud rationally select.

a) what is the expected return of this portfolio?

b) what is the standard devistion of this portfolio?

Use the following...

You

are constructing a risky portfolio for a client, to be comprised of

both an equity fund and a bond fund. The probability distributions

of the two funds are guven below. The correlation between the two

funds is 0.10.

QUESTION 11

11.) For an investor with a risk-acersion score (A) of 4,

identify the portfolio he woud rationally select.

a) what is the expected return of this portfolio?

b) what is the standard devistion of this portfolio?

Use the following...

Most questions answered within 3 hours.

-

List and explain why a company would choose to use a

published

compensation survey vs. creating...

asked 5 minutes ago -

A discrete random variable X can take values from 1 to 10. Find

the variance of...

asked 18 minutes ago -

The primary financial goal of a corporation is to maximize:

shareholders wealth.

earnings per share.

stock...

asked 25 minutes ago -

determine whether the vectors u=(1,2,3,), v=(-2,1,0) and

w=(1,0,1) are linearly dependent or independent.

asked 31 minutes ago -

python

Define a function called print_values which takes a dictionary

object as a parameter. The function...

asked 1 hour ago -

In Chapter 1 you created a program named Triangle in

which you displayed a seven-line triangle...

asked 1 hour ago -

Research question: What are the differences between separately

stated and non separately stated transactions in an...

asked 1 hour ago -

By using Arduino write a code that connects two LEDs to two

push-buttons. Each button controls...

asked 2 hours ago -

Bank of America has bonds that pay a coupon interest rate of 5.5

percent and mature...

asked 3 hours ago -

Problem: Patient Fees C++

You are to write a program that computes a patient’s bill for...

asked 5 hours ago -

In a population of interest, we know that, 77% drink coffee, and

23% drink tea. Assume...

asked 5 hours ago -

Given that f(x) = e-(x-1) for x > 1, determine the following

probabilities:

a) P(X <...

asked 5 hours ago