Req 1 Req 2 Req 3 Complete the standard cost card for each product, showing the standard cost of direct materials and direct labor. (Round your answers to 2 decimal places.) Standard Quantity or Hours Standard Price or Rate Standaro Cost Alpha6 Direct materials-X442 Direct materials-Y661 Direct labor-Sintering Direct labor-Finishing Total kilos iters hours hours per kilo per liter per hour per hour Zeta7 Direct materials-X442 Direct materials-Y661 Direct labor-Sintering Direct labor-Finishing Total kilos liters hours hours per kilo per liter per hour per hour

Req 1 Req 2 Req 3 Compute the materials price and quantity variances for each material. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (i.e., zero variance). Input all amounts as positive values.) Direct Materials Variances-Material X442: Materials price variance Materials quantity variance Direct Materials Variances-Material Y661 Materials price variance Materials quantity variance 〈 Req 1 Req 3>

Homework Answers

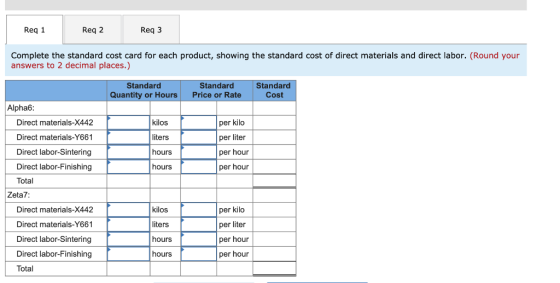

| 1 | Standard cost card: | ||||||||

|

Standard quantity or hours |

Standard price or rate |

Standard cost |

|||||||

| Alpha6: | |||||||||

| Direct materials-X442 | 2 | Kilos | 4.3 | Per kilo | 8.6 | ||||

| Direct materials-Y661 | 1.5 | Liters | 1.6 | Per liter | 2.4 | ||||

| Direct labor-Sintering | 0.1 | Hours | 22 | Per hour | 2.2 | ||||

| Direct labor-Finishing | 0.8 | Hours | 21 | Per hour | 16.8 | ||||

| Total | 30 | ||||||||

| Zeta7: | |||||||||

| Direct materials-X442 | 3 | Kilos | 4.3 | Per kilo | 12.9 | ||||

| Direct materials-Y661 | 2.5 | Liters | 1.6 | Per liter | 4 | ||||

| Direct labor-Sintering | 0.45 | Hours | 22 | Per hour | 9.9 | ||||

| Direct labor-Finishing | 0.9 | Hours | 21 | Per hour | 18.9 | ||||

| Total | 45.7 | ||||||||

| 2 | Material X442: | ||||||||

| Material price variance=Actual material purchased*(Standard rate for material-Actual rate for material) | |||||||||

| Actual material purchased=14800 Kilos | |||||||||

| Standard rate=$ 4.3 per kilo | |||||||||

| Actual rate=66600/14800=$4.5 per kilo | |||||||||

| Material price variance=14800*(4.3-4.5)=2960 U | |||||||||

| (Actual rate is more than the standard rate.Hence, variance is unfavorable) | |||||||||

| Material quantity variance=Standard rate for materials*(Standard materials required-Actual material used) | |||||||||

| Standard rate=$ 4.3 per kilo | |||||||||

| Standard materials required=Actual units produced*Material required per unit=(2300*2)+(1600*3)=9400 kilos | |||||||||

| Actual material used=9300 kilos | |||||||||

| Material quantity variance=4.3*(9400-9300)=430 F | |||||||||

| (Actual material used is less than the standard material required.Hence, variance is favorable) | |||||||||

| Material Y661: | |||||||||

| Material price variance=Actual material purchased*(Standard rate for material-Actual rate for material) | |||||||||

| Actual material purchased=15800 liters | |||||||||

| Standard rate=$ 1.6 per liter | |||||||||

| Actual rate=23700/15800=$1.5 per liter | |||||||||

| Material price variance=15800*(1.6-1.5)=1580 F | |||||||||

| (Actual rate is less than the standard rate.Hence, variance is favorable) | |||||||||

| Material quantity variance=Standard rate for materials*(Standard materials required-Actual material used) | |||||||||

| Standard rate=$ 1.6 per liter | |||||||||

| Standard materials required=Actual units produced*Material required per unit=(2300*1.5)+(1600*2.5)=7450 liters | |||||||||

| Actual material used=13800 liters | |||||||||

| Material quantity variance=1.6*(7450-13800)=10160 U | |||||||||

| (Actual material used is more than the standard material required.Hence, variance is unfavorable) | |||||||||

| 3 | Sintering: | ||||||||

| Labor rate variance=Actual hours worked*(Statndard labor rate-Actual labor rate) | |||||||||

| Actual hours worked=1220 hours | |||||||||

| Standard labor rate=$22 per hour | |||||||||

| Actual labor rate=Actual direct labor cost/Actual hours=28060/1220=$23 per hour | |||||||||

| Labor rate variance=1220*(22-23)=1220 U | |||||||||

| (Actual labor rate is more than standard labor rate.Hence variance is unfavorable) | |||||||||

| Labor efficiency variance=Standard labor rate*(Standard labor hours required-Actual labor hours worked) | |||||||||

| Standard labor rate=$22 per hour | |||||||||

| Standard labor hours required=Actual units produced*Labor hours required per unit=(2300*0.10)+(1600*0.45)=950 hours | |||||||||

| Actual hours worked=1220 hours | |||||||||

| Labor efficiency variance=22*(950-1220)=5940 U | |||||||||

| (Actual hours worked is more than the standard hours required.Hence, variance is unfavorable) | |||||||||

| Finishing: | |||||||||

| Labor rate variance=Actual hours worked*(Statndard labor rate-Actual labor rate) | |||||||||

| Actual hours worked=2930 hours | |||||||||

| Standard labor rate=$21 per hour | |||||||||

| Actual labor rate=Actual direct labor cost/Actual hours=67390/2930=$23 per hour | |||||||||

| Labor rate variance=2930*(21-23)=5860 U | |||||||||

| (Actual labor rate is more than standard labor rate.Hence variance is unfavorable) | |||||||||

| Labor efficiency variance=Standard labor rate*(Standard labor hours required-Actual labor hours worked) | |||||||||

| Standard labor rate=$21 per hour | |||||||||

| Standard labor hours required=Actual units produced*Labor hours required per unit=(2300*0.80)+(1600*0.90)=3280 hours | |||||||||

| Actual hours worked=2930 hours | |||||||||

| Labor efficiency variance=21*(3280-2930)=7350 F | |||||||||

| (Actual hours worked is less than the standard hours required.Hence, variance is favorable) | |||||||||

Add Answer to:

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations,...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Sintering 0.20 hours Finishing Product X442 Y661 Alpha6 2.5 kilos 2.5 liters 0.90 hours 4.5 kilos 3.5 liters 0.30 hours 1.20 hours Zeta7 Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Sintering 0.20 hours Finishing Product X442 Y661 Alpha6 2.5 kilos 2.5 liters 0.90 hours 4.5 kilos 3.5 liters 0.30 hours 1.20 hours Zeta7 Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materlals-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material standard Labor Time sintering Finishing e.9 hours e.80 hours Product X442 Y661 2.5 liters 3.5 liters Alpha6 Zeta7 1.5 kilos e.20 hours 3.5 kilos e.35 hours Information relating to materials purchased and materlals...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materlals-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material standard Labor Time sintering Finishing e.9 hours e.80 hours Product X442 Y661 2.5 liters 3.5 liters Alpha6 Zeta7 1.5 kilos e.20 hours 3.5 kilos e.35 hours Information relating to materials purchased and materlals...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

1.5 kilos

2.0 liters

0.20 hours

0.80 hours

Zeta7

3.5 kilos

4.0 liters

0.40 hours

0.90 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

1.5 kilos

2.0 liters

0.20 hours

0.80 hours

Zeta7

3.5 kilos

4.0 liters

0.40 hours

0.90 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials, X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Finishing 0.90 hours Sintering Y661 1.5 liters Product X442 2.0 kilos Alpha6 0.30 hours 4.0 kilos 3.0 liters Zeta7 0.40 hours 1.00 hours Information relating to materials purchased and...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials, X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Finishing 0.90 hours Sintering Y661 1.5 liters Product X442 2.0 kilos Alpha6 0.30 hours 4.0 kilos 3.0 liters Zeta7 0.40 hours 1.00 hours Information relating to materials purchased and...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Standard Labor Time sintering 0.20 hours Raw Material Product Alpha6 Zeta7 x442 2.0 kilos 4.0 kilos Y661 3.4 1iters Finishing 0.80 hours 5.0 liters 0.25 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Standard Labor Time sintering 0.20 hours Raw Material Product Alpha6 Zeta7 x442 2.0 kilos 4.0 kilos Y661 3.4 1iters Finishing 0.80 hours 5.0 liters 0.25 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials—X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Product X442 Y661 Sintering Finishing Alpha6 2.0 kilos 1.5 liters 0.10 hours 0.80 hours Zeta7 3.0 kilos 2.5 liters 0.45 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishin...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials—X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Product X442 Y661 Sintering Finishing Alpha6 1.8 kilos 2.0 liters 0.20 hours 0.80 hours Zeta7 3.0 kilos 4.5 liters 0.35 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

2.0 kilos

1.5 liters

0.30 hours

0.90 hours

Zeta7

4.0 kilos

3.0 liters

0.40 hours

1.00 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

2.0 kilos

1.5 liters

0.30 hours

0.90 hours

Zeta7

4.0 kilos

3.0 liters

0.40 hours

1.00 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials—X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Product X442 Y661 Sintering Finishing Alpha6 1.8 kilos 2.0 liters 0.20 hours 0.80 hours Zeta7 3.0 kilos 4.5 liters 0.35 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing....

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials—X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Product X442 Y661 Sintering Finishing Alpha6 1.8 kilos 2.0 liters 0.20 hours 0.80 hours Zeta7 3.0 kilos 4.5 liters 0.35 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Sintering 0.20 hours Finishing Product X442 Y661 Alpha6 2.5 kilos 2.5 liters 0.90 hours 4.5 kilos 3.5 liters 0.30 hours 1.20 hours Zeta7 Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Sintering 0.20 hours Finishing Product X442 Y661 Alpha6 2.5 kilos 2.5 liters 0.90 hours 4.5 kilos 3.5 liters 0.30 hours 1.20 hours Zeta7 Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materlals-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material standard Labor Time sintering Finishing e.9 hours e.80 hours Product X442 Y661 2.5 liters 3.5 liters Alpha6 Zeta7 1.5 kilos e.20 hours 3.5 kilos e.35 hours Information relating to materials purchased and materlals...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materlals-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material standard Labor Time sintering Finishing e.9 hours e.80 hours Product X442 Y661 2.5 liters 3.5 liters Alpha6 Zeta7 1.5 kilos e.20 hours 3.5 kilos e.35 hours Information relating to materials purchased and materlals...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

1.5 kilos

2.0 liters

0.20 hours

0.80 hours

Zeta7

3.5 kilos

4.0 liters

0.40 hours

0.90 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

1.5 kilos

2.0 liters

0.20 hours

0.80 hours

Zeta7

3.5 kilos

4.0 liters

0.40 hours

0.90 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials, X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Finishing 0.90 hours Sintering Y661 1.5 liters Product X442 2.0 kilos Alpha6 0.30 hours 4.0 kilos 3.0 liters Zeta7 0.40 hours 1.00 hours Information relating to materials purchased and...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials, X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Raw Material Standard Labor Time Finishing 0.90 hours Sintering Y661 1.5 liters Product X442 2.0 kilos Alpha6 0.30 hours 4.0 kilos 3.0 liters Zeta7 0.40 hours 1.00 hours Information relating to materials purchased and...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Standard Labor Time sintering 0.20 hours Raw Material Product Alpha6 Zeta7 x442 2.0 kilos 4.0 kilos Y661 3.4 1iters Finishing 0.80 hours 5.0 liters 0.25 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s, which pass through two operations, Sintering and Finishing. Each of the products uses two raw materials-X442 and Y661. The company uses a standard cost system, with the following standards for each product (on a per unit basis): Standard Labor Time sintering 0.20 hours Raw Material Product Alpha6 Zeta7 x442 2.0 kilos 4.0 kilos Y661 3.4 1iters Finishing 0.80 hours 5.0 liters 0.25 hours 0.90 hours Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

2.0 kilos

1.5 liters

0.30 hours

0.90 hours

Zeta7

4.0 kilos

3.0 liters

0.40 hours

1.00 hours

Information relating to materials purchased and materials...

Mickley Corporation produces two products, Alpha6s and Zeta7s,

which pass through two operations, Sintering and Finishing. Each of

the products uses two raw materials—X442 and Y661. The company uses

a standard cost system, with the following standards for each

product (on a per unit basis):

Raw Material

Standard Labor Time

Product

X442

Y661

Sintering

Finishing

Alpha6

2.0 kilos

1.5 liters

0.30 hours

0.90 hours

Zeta7

4.0 kilos

3.0 liters

0.40 hours

1.00 hours

Information relating to materials purchased and materials...

Most questions answered within 3 hours.

-

2) You are given the task of finding a representation for a

circle in a drawing...

asked 49 minutes ago -

STUDY QUESTION: Does use of diet drug fen-phen

(fenfluramine-phentermine) cause valvular heart disease?

HINT: Valvular heart...

asked 40 minutes ago -

1. An object weighing 40 N rests on a surface. The coefficient

of friction is 0.35....

asked 1 hour ago -

Investor company owns 35% of investee company voting stock and

accounts for the investment under the...

asked 3 hours ago -

The number of major faults on a randomly chosen 1 km stretch of

highway has a...

asked 3 hours ago -

Consider the competitive environment of Starbuck's, Progressive

Insurance, a manufacturing firm with low turnover, or a...

asked 4 hours ago -

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 6 hours ago -

A business executive has the option to invest money in two

plans: Plan A guarantees that...

asked 8 hours ago -

Hello, can someone please help me answer this question?

How much heat is absorbed by a...

asked 8 hours ago -

. A marketing researcher conducted a survey of 25 shoppers

randomly selected at the local mall...

asked 8 hours ago -

Create an comprehensive response to the

following:

Antimicrobial agents work on a multitude of microbes (bacteria,...

asked 8 hours ago -

6.13 LAB: Step counter. Section 6.3.

A pedometer treats walking 2,000 steps as walking 1 mile....

asked 8 hours ago