Expected Return Standard Deviation Portfolio A 12% 20% Portfolio B 6% 12% T...

|

Expected Return |

Standard Deviation |

|

|

Portfolio A |

12% |

20% |

|

Portfolio B |

6% |

12% |

|

T-bill |

3% |

0% |

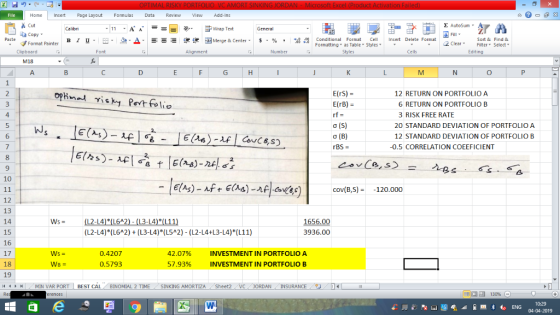

You are an investment adviser and you have the three investments above to recommend to your clients. The correlation between A and B is -0.5.

Solve for the optimal risky portfolio and enter the weights as a %, 99% should be entered as 99.00%.

Percent invested in Portfolio A

Percent invested in Portfolio B

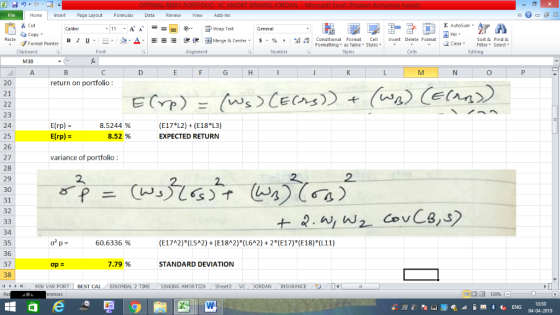

What is the standard deviation of the optimal risky portfolio?

What is the expected return of the optimal risky portfolio?

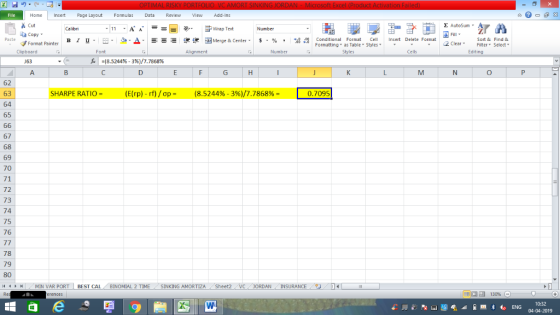

What is the Sharpe ratio of the optimal risky portfolio?

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP PLEASE

EXPECTED RETURN AND STANDARD DEVIATION ROUNDED TO 2 DECIMALS. SHARPE RATIO WAS ROUNDED TO 4 DECIMALS. THANK YOU

EXPECTED RETURN : 8.5244% AND STANDARD DEVIATION :7.7868%, THEN ROUNDED TO 2 DECIMALS.

FOR SHARPE RATIO, BOTH ARE TAKEN TILL 4 DECIMALS. THANK

YOU

Add Answer to:

Expected Return Standard Deviation Portfolio A 12% 20% Portfolio B 6% 12% T...

13. Consider a Market Portfolio with 12% expected return and 20% return standard deviation. If the...

13. Consider a Market Portfolio with 12% expected return and 20% return standard deviation. If the Sharpe ratio of the market portfolio is 0.5, what is the risk-free rate of return? (a) 0.01 (b) 0.02 (c) 0.03 (d) 0.04

13. Consider a Market Portfolio with 12% expected return and 20% return standard deviation. If the Sharpe ratio of the market portfolio is 0.5, what is the risk-free rate of return? (a) 0.01 (b) 0.02 (c) 0.03 (d) 0.04

you are considering investing in two securities. Security 1 has a expected return of 12% and a standard deviation of ret...

you are considering investing in two securities. Security 1 has a expected return of 12% and a standard deviation of return of 10%. Security 2 has an expected return of 9%and a standard deviation of returns of 8%. The correlation coefficient of returns for the two securities is 0.3. What would the weights be for each of the two securities in the minimum variance portfolio? W1= W2= Given the weights computed in (a), compute the expected return and standard deviation...

You manage a risky portfolio with an expected return of 12% and a standard deviation of 24%. Assume that you can invest...

You manage a risky portfolio with an expected return of 12% and a standard deviation of 24%. Assume that you can invest and borrow at a risk-free rate of 3%, using T-bills. a. Draw the Capital Allocation Line (CAL) for this combination of risky portfolio and risk-free asset. What is the Sharpe ratio of the risky portfolio? b. Your client chooses to invest 50% of their funds into your risky portfolio and 50% risk-free. What is the expected return and...

Suppose the optimal risky portfolio has an expected return of 13.25% and a standard deviation of...

Suppose the optimal risky portfolio has an expected return of 13.25% and a standard deviation of 24.57%. Mr. Jones wants an efficient portfolio with an expected return of 12%. If the optimal risky portfolio consists of 70.75% in stocks and 29.25% in bonds, what is the proportion of Mr. Jones' portfolio invested in the stock fund. the risk-free rate is 5.5%.

An investor has a risk aversion coefficient of 5. The expected return and standard deviation of...

An investor has a risk aversion coefficient of 5. The expected return and standard deviation of the optimal risky portfolio are 15% and 25%, respectively. If the Sharpe ratio of the optimal capital allocation line is 0.48, what is the proportion of the investor’s combined portfolio that should be invested in the risky portfolio that would maximise their utility?

The expected return of Security A is 12 percent with a standard deviation of 15 percent....

The expected return of Security A is 12 percent with a standard deviation of 15 percent. The expected return of Security B is 9 percent with a standard deviation of 10 percent. Securities A and B have a correlation of 0.4. The market return is 11 percent with a standard deviation of 13 percent and the risk-free rate is 4 percent. What is the Sharpe ratio of a portfolio if 35 percent of the portfolio is in Security A and...

3. You have a risky portfolio that yields an expected rate of return of 15% with...

3. You have a risky portfolio that yields an expected rate of return of 15% with a standard deviation of 25%. Draw the CAL for an expected return/standard deviation diagram if the risk free rate is 5%. a. What is the slope of the CAL? b. If your coefficient of risk aversion is 5, how much should you invest in the risky portfolio? 4. A pension fund manager is considering three mutual funds. The first is a stock fund, the...

You manage a risky portfolio with an expected rate of return of 19% and a standard...

You manage a risky portfolio with an expected rate of return of 19% and a standard deviation of 33%. The T-bill rate is 7%. Your client chooses to invest 80% of a portfolio in your fund and 20% in a T-bill money market fund. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client’s? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Your reward-to-volatility ratio?________ Clients' reward-to-volatility ratio?_________

A risky portfolio has an expected return of 12% and standard deviation of 25%. Given a...

A risky portfolio has an expected return of 12% and standard deviation of 25%. Given a risk free rate of 3%, what percentage of a clients portfolio should be allocated to the risky portfolio if the client has a risk aversion of 4?

Stocks offer an expected rate of return of 18%, with a standard deviation of 22%. Gold...

Stocks offer an expected rate of return of 18%, with a standard deviation of 22%. Gold offers an expected return of 10% with a standard deviation of 30%. In light of the apparent inferiority of gold with respect to average return and volatility, would anyone hold gold in his portfolio? Assume that the correlation between Stocks and Gold is -0.5. Find the weights wS and wG of the efficient risky portfolio which is invested in Stocks and Gold and which...

13. Consider a Market Portfolio with 12% expected return and 20% return standard deviation. If the Sharpe ratio of the market portfolio is 0.5, what is the risk-free rate of return? (a) 0.01 (b) 0.02 (c) 0.03 (d) 0.04

13. Consider a Market Portfolio with 12% expected return and 20% return standard deviation. If the Sharpe ratio of the market portfolio is 0.5, what is the risk-free rate of return? (a) 0.01 (b) 0.02 (c) 0.03 (d) 0.04

Most questions answered within 3 hours.

-

This picture is a visual representation of helium. Write the

chemical formula for helium.

asked 1 minute ago -

1. Sample Mean:

mens- 27.91

women - 31.57

2. Standard Deviation

men- 0.664

women- 1.167

Sample...

asked 11 minutes ago -

Needs Help with Java Programming language!

Lights Camera

Action Purpose: To learn the basics of linked...

asked 9 minutes ago -

Please answer my questions:

True or False and Explain

5)In a perfectly competitive market, if price...

asked 14 minutes ago -

Suppose the interest on a foreign government bonds is 7.5%, and

the current exchange rate is...

asked 15 minutes ago -

Explain why it is important to know common Windows processes

when conducting a forensic investigation

asked 20 minutes ago -

How do child protective services help to reduce the

vulnerability of minors to human trafficking?

asked 28 minutes ago -

Which of the following is correct?

a. ATC = AVC/Q

b. ATC = AFC/Q

c. ATC...

asked 28 minutes ago -

The height of a Harrier airplane above the ground is given by h

= 4.00t 3...

asked 37 minutes ago -

Subject Conflict resolution :

1-Describe the basic model for engaging someone in a

collaborative discussion in...

asked 37 minutes ago -

Using the four models of CSR, and given your own personal

values, what type of firm...

asked 41 minutes ago -

A 10 kg mass slides along a frictionless plane inclined at 38

degrees to the horizontal....

asked 45 minutes ago