Consolidation: Intra-group transactions On 1 July 2015, Ping Pong Ltd acquired all the issued sha...

Consolidation: Intra-group transactions

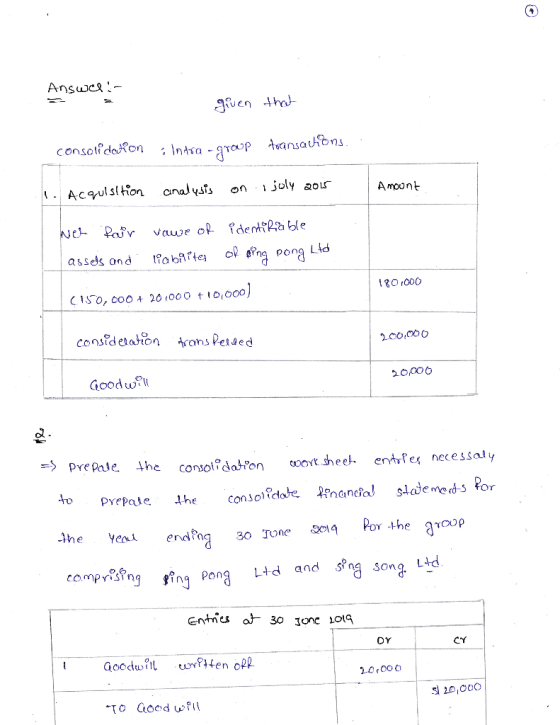

On 1 July 2015, Ping Pong Ltd acquired all the issued shares of Sing Song Ltd. At the date of acquisition, the shareholders’ equity of Sing Song Ltd consisted of share capital $150,000; general reserve $20,000 and retained earnings $10,000. The identifiable net assets of Sing Song Ltd were recorded at amounts equal to their fair values at the date of acquisition. At 30 June 2019, four years after acquisition, the accounts of the two companies appear as follows:

| Ping Pong Ltd | Sing Song Ltd | |

| $ | $ | |

| Sales | 340,000 | 140,000 |

| Cost of sales | ||

| Opening inventory at 1 July 2018 | 20,000 | 5,000 |

| Purchases | 200,000 | 73,000 |

| 220,000 | 78,000 | |

| Closing inventory 30 June 2019 | (25,000) | (15,000) |

| Cost of sales | 195,000 | 63,000 |

| Gross profit | 145,000 | 77,000 |

| Depreciation expenses | 32,000 | 23,000 |

| Interest expense | 9,000 | 1,000 |

| Management fee expense | – | 7,000 |

| Other expenses | 43,000 | 34,000 |

| Total expenses | 84,000 | 65,000 |

| Gross profit less total expenses | 61,000 | 12,000 |

| Other income | ||

| Dividend revenue | 5,000 | – |

| Interest revenue | 3,000 | |

| Management fee revenue | 7,000 | |

| Total other income | 12,000 | 3,000 |

| Operating profit before tax | 73,000 | 15,000 |

| Income tax expense | 28,000 | 5,000 |

| Operating profit after tax | 45,000 | 10,000 |

| Retained earnings 1 July 2018 | 35,000 | 5,000 |

| Available for appropriation | 80,000 | 15,000 |

| Interim dividend paid | 10,000 | 2,000 |

| Final dividend proposed | 30,000 | 3,000 |

| Dividends paid and proposed | 40,000 | 5,000 |

| Retained earnings 30 June 2019 | 40,000 | 10,000 |

| Share capital | 400,000 | 150,000 |

| General reserve | 20,000 | 30,000 |

| Accounts payable | 40,000 | 20,000 |

| Dividend payable | 30,000 | 3,000 |

| 12% unsecured notes | 50,000 | – |

| Other liabilities | 16,000 | 15,000 |

| 596,000 | 228,000 | |

| Assets | ||

| Accounts receivable | 50,000 | 26,000 |

| Inventory | 25,000 | 15,000 |

| Dividend receivable | 3,000 | – |

| Unsecured notes – Ping Pong Ltd | – | 25,000 |

| Investment in Sing Song Ltd | 200,000 | – |

| Other assets | 318,000 | 162,000 |

| 596,000 | 228,000 |

Additional information:

- The directors have decided that goodwill should be written off completely, no writedowns for goodwill impairment losses were made in prior years.

- During the current financial year, Sing Song Ltd paid management fees of $7,000 to Ping Pong Ltd.

- On 1 June 2019, Ping Pong Ltd sold inventory to Sing Song Ltd for $30,000. All of this inventory has been sold by Sing Song Ltd to parties external to the group during June 2019. This intra-group sale was made on credit terms, and $10,000 remains owing to Ping Pong at 30 June 2019.

- Sing Song Ltd holds half of the unsecured notes issued by Ping Pong Ltd. Interest at a rate of 12% has been paid on these notes during the year.

- On 25 January 2019, Sing Song Ltd paid an interim dividend of $2,000 to Ping Pong Ltd.

- Sing Song Ltd declared a final dividend of $3,000 on 20 June 2019. Ping Pong Ltd has recognised this dividend as a receivable at 30 June 2019.

- The tax rate is 30%.

Required:

- Prepare an acquisition analysis.

- Prepare the consolidation worksheet entries necessary to prepare the consolidated financial statements for the year ending 30 June 2019 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidation worksheet and the consolidated financial statements.

Homework Answers

Add Answer to:

Consolidation: Intra-group transactions On 1 July 2015, Ping Pong Ltd acquired all the issued sha...

On 1 July 2017, Parent Ltd acquired all the shares of Son Ltd, on a cum-div....

On 1 July 2017, Parent Ltd acquired all the shares of Son Ltd, on a cum-div. basis, for $3,230,000. At this date, the equity of Son Ltd consisted of: $1,200,000 Share capital -600 000 shares General reserve Retained earnings 500,000 900,000 At the acquisition date, Son Ltd reported a dividend payable of $50,000 and its assets included $100, 000 of recorded goodwill. The dividend payable at the acquisition date was subsequently paid in August 2017. On 1 July 2017, all...

On 1 July 2017, Parent Ltd acquired all the shares of Son Ltd, on a cum-div. basis, for $3,230,000. At this date, the equity of Son Ltd consisted of: $1,200,000 Share capital -600 000 shares General reserve Retained earnings 500,000 900,000 At the acquisition date, Son Ltd reported a dividend payable of $50,000 and its assets included $100, 000 of recorded goodwill. The dividend payable at the acquisition date was subsequently paid in August 2017. On 1 July 2017, all...

Question 1 King Ltd acquired 100% of the share capital of Sing Ltd on 1 July...

Question 1 King Ltd acquired 100% of the share capital of Sing Ltd on 1 July 2015, for $356,000. At the acquisition date, the equity of Sing Ltd comprise of the following: $ Share capital 200,000 Retained earnings 80,000 Total 280,000 The identifiable net assets of Sing Ltd were recorded at fair value at the date of acquisition, except for inventory that had a fair value which was $2,000 higher than its carrying amount, and an item of plant...

NCI Intra-group transactions. Frank Ltd had acquired 70% of Barry Ltd, on 1/07/2016. A. On 10...

NCI Intra-group transactions. Frank Ltd had acquired 70% of Barry Ltd, on 1/07/2016. A. On 10 April 2019, Barry Ltd sold equipment to Frank Ltd for $50 000. At the time of the sale, the equipment had a carrying amount of $46 875 in the books of Barry Ltd. Winnaleah Wines had purchased the equipment on 30 June 2015 for $75 000 and depreciated it at 10% straight-line on cost with no residual value. Frank Ltd uses the same method...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration of $500,000 cash and a brand that was held in their accounts at a book value of $10,000 but at 1 July 2013 had a fair value of $24,000. At that date all the identifiable assets and liabilities were recorded at fair value with the exception of: The inventory was all sold by 30/6/14. The remaining useful life of the plant is...

a) Liala Ltd acquired all the issued shares of Jordan Ltd on 1 January 2015. The...

a) Liala Ltd acquired all the issued shares of Jordan Ltd on 1 January 2015. The following transactions occurred between the two entities: On 1 June 2016, Liala Ltd sold inventory to Jordan Ltd for $12,000, this inventory previously costed Liala Ltd $10,000. By 30 June 2016, Jordan Ltd had sold 20% of this inventory to other entities for $3,000. The other 80% was all sold to external entities by 30 June 2017 for $13,000. During the 2016–17...

a) Liala Ltd acquired all the issued shares of Jordan Ltd on 1 January 2015. The...

a) Liala Ltd acquired all the issued shares of Jordan Ltd on 1 January 2015. The following transactions occurred between the two entities: On 1 June 2016, Liala Ltd sold inventory to Jordan Ltd for $12,000, this inventory previously costed Liala Ltd $10,000. By 30 June 2016, Jordan Ltd had sold 20% of this inventory to other entities for $3,000. The other 80% was all sold to external entities by 30 June 2017 for $13,000. During the 2016–17...

Question 1 King Ltd acquired 80% of the shares of Queen Ltd on 1 July 2005...

Question 1 King Ltd acquired 80% of the shares of Queen Ltd on 1 July 2005 for S 325,000 when the equity of Queen Ltd consisted of Share Capital Retained Earnings General Reserve $250,000 45,000 35,000 All identifiable assets and liabilities of Queen Ltd are recorded at fair value at this date except for the following: Carrying Amount: Fair Value: Inventory Plant (cost $200,000) $50,000 $150,000 $60,000 $180,000 Queen Ltd had not recorded an intermally generated Trademark. King Ltd valued...

Question 1 King Ltd acquired 80% of the shares of Queen Ltd on 1 July 2005 for S 325,000 when the equity of Queen Ltd consisted of Share Capital Retained Earnings General Reserve $250,000 45,000 35,000 All identifiable assets and liabilities of Queen Ltd are recorded at fair value at this date except for the following: Carrying Amount: Fair Value: Inventory Plant (cost $200,000) $50,000 $150,000 $60,000 $180,000 Queen Ltd had not recorded an intermally generated Trademark. King Ltd valued...

Hitech Ltd acquired all of the issued share capital of Lotech Ltd on 30 June 2016...

Hitech Ltd acquired all of the issued share capital of Lotech Ltd on 30 June 2016 for a cash consideration of $400,000 At that time the net assets of Lotech Ltd were represented as follows: Share capital 300,000 Retained earnings 50,000 Net assets 350,000 When Hitech acquired its investment in Lotech the following information applied: Land held by Lotech had a fair value $10,000 greater than the carrying value A contingent liability relating to an unsettled legal claim with a...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration of $500,000 cash and a brand that was held in their accounts at a book value of $10,000 but at 1 July 2013 had a fair value of $24,000 At that date all the identifiable assets and liabilities were recorded at fair value with the exception of ASSET Inventory Land Plant (less depn) Book Value Market Value 12,000 28,000 10,000 25,000 20,000...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration of $500,000 cash and a brand that was held in their accounts at a book value of $10,000 but at 1 July 2013 had a fair value of $24,000 At that date all the identifiable assets and liabilities were recorded at fair value with the exception of ASSET Inventory Land Plant (less depn) Book Value Market Value 12,000 28,000 10,000 25,000 20,000...

Sky Ltd acquired all the issued shares (Ex div.) of Nu Ltd on 1 July 2018...

Sky Ltd acquired all the issued shares (Ex div.) of Nu Ltd on 1 July 2018 for $100 000. At this date Nu Ltd recorded a dividend payable of $10 000 and equity of: | Share capital Retained earnings | Asset revaluation surplus $54 000 36 000 18 000 All the identifiable assets and liabilities of Nu Ltd were recorded at amounts equal to their fair values at acquisition date except for: Inventories Machinery (cost $100 000) Carrying amount 16...

Sky Ltd acquired all the issued shares (Ex div.) of Nu Ltd on 1 July 2018 for $100 000. At this date Nu Ltd recorded a dividend payable of $10 000 and equity of: | Share capital Retained earnings | Asset revaluation surplus $54 000 36 000 18 000 All the identifiable assets and liabilities of Nu Ltd were recorded at amounts equal to their fair values at acquisition date except for: Inventories Machinery (cost $100 000) Carrying amount 16...

On 1 July 2017, Parent Ltd acquired all the shares of Son Ltd, on a cum-div. basis, for $3,230,000. At this date, the equity of Son Ltd consisted of: $1,200,000 Share capital -600 000 shares General reserve Retained earnings 500,000 900,000 At the acquisition date, Son Ltd reported a dividend payable of $50,000 and its assets included $100, 000 of recorded goodwill. The dividend payable at the acquisition date was subsequently paid in August 2017. On 1 July 2017, all...

On 1 July 2017, Parent Ltd acquired all the shares of Son Ltd, on a cum-div. basis, for $3,230,000. At this date, the equity of Son Ltd consisted of: $1,200,000 Share capital -600 000 shares General reserve Retained earnings 500,000 900,000 At the acquisition date, Son Ltd reported a dividend payable of $50,000 and its assets included $100, 000 of recorded goodwill. The dividend payable at the acquisition date was subsequently paid in August 2017. On 1 July 2017, all...

Question 1 King Ltd acquired 80% of the shares of Queen Ltd on 1 July 2005 for S 325,000 when the equity of Queen Ltd consisted of Share Capital Retained Earnings General Reserve $250,000 45,000 35,000 All identifiable assets and liabilities of Queen Ltd are recorded at fair value at this date except for the following: Carrying Amount: Fair Value: Inventory Plant (cost $200,000) $50,000 $150,000 $60,000 $180,000 Queen Ltd had not recorded an intermally generated Trademark. King Ltd valued...

Question 1 King Ltd acquired 80% of the shares of Queen Ltd on 1 July 2005 for S 325,000 when the equity of Queen Ltd consisted of Share Capital Retained Earnings General Reserve $250,000 45,000 35,000 All identifiable assets and liabilities of Queen Ltd are recorded at fair value at this date except for the following: Carrying Amount: Fair Value: Inventory Plant (cost $200,000) $50,000 $150,000 $60,000 $180,000 Queen Ltd had not recorded an intermally generated Trademark. King Ltd valued...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration of $500,000 cash and a brand that was held in their accounts at a book value of $10,000 but at 1 July 2013 had a fair value of $24,000 At that date all the identifiable assets and liabilities were recorded at fair value with the exception of ASSET Inventory Land Plant (less depn) Book Value Market Value 12,000 28,000 10,000 25,000 20,000...

On 1 July 2013 David Ltd acquired all of the share capital of Goliath Limited for a consideration of $500,000 cash and a brand that was held in their accounts at a book value of $10,000 but at 1 July 2013 had a fair value of $24,000 At that date all the identifiable assets and liabilities were recorded at fair value with the exception of ASSET Inventory Land Plant (less depn) Book Value Market Value 12,000 28,000 10,000 25,000 20,000...

Sky Ltd acquired all the issued shares (Ex div.) of Nu Ltd on 1 July 2018 for $100 000. At this date Nu Ltd recorded a dividend payable of $10 000 and equity of: | Share capital Retained earnings | Asset revaluation surplus $54 000 36 000 18 000 All the identifiable assets and liabilities of Nu Ltd were recorded at amounts equal to their fair values at acquisition date except for: Inventories Machinery (cost $100 000) Carrying amount 16...

Sky Ltd acquired all the issued shares (Ex div.) of Nu Ltd on 1 July 2018 for $100 000. At this date Nu Ltd recorded a dividend payable of $10 000 and equity of: | Share capital Retained earnings | Asset revaluation surplus $54 000 36 000 18 000 All the identifiable assets and liabilities of Nu Ltd were recorded at amounts equal to their fair values at acquisition date except for: Inventories Machinery (cost $100 000) Carrying amount 16...

Most questions answered within 3 hours.

-

Problem 1: Present entries to record the selected transactions

described below:

(a)

Issued $2,790,000 of 5-year,...

asked 1 minute ago -

Using technology to support HR activities increases:

a.

the efficiency of the administrative HR functions.

b....

asked 2 minutes ago -

1. List the features used to classify leaf

types.

2. List some characteristics that are shared...

asked 7 minutes ago -

The three elements of Value Proposition, Key Customers, and

Capabilities operate within an environment. Which of...

asked 9 minutes ago -

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 17 minutes ago -

Each row of the table below describes an aqueous solution at

25°C

.

The second column...

asked 21 minutes ago -

A horizontal wire is at y = 0. Current travels in the +x

direction. The magnetic...

asked 22 minutes ago -

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 43 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 41 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 46 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 45 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 51 minutes ago