Homework Answers

![Optian-2 Ρυγ ch as t -E-from 10003 . 1000 s 1-21 E-a F$26 4462 Sal t gett $20 4462 salo set 6 Ans [c] No abita opPontunita](http://img.homeworklib.com/images/fb277a90-a396-4b61-8daa-66ee764de009.png?x-oss-process=image/resize,w_560)

Add Answer to:

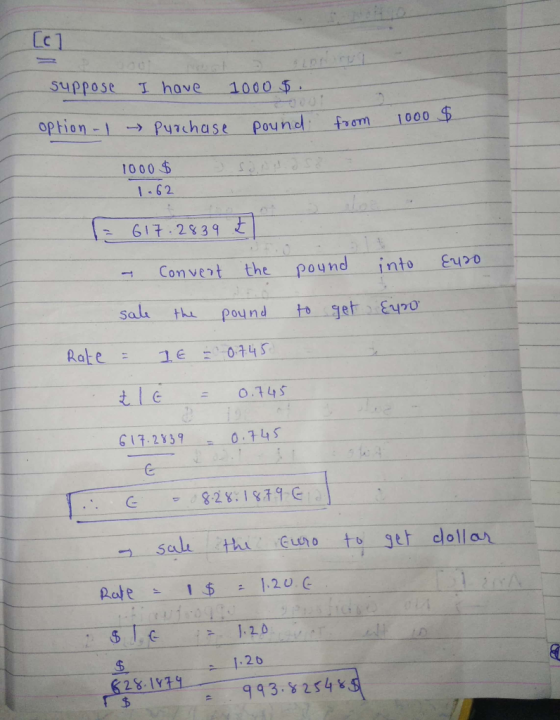

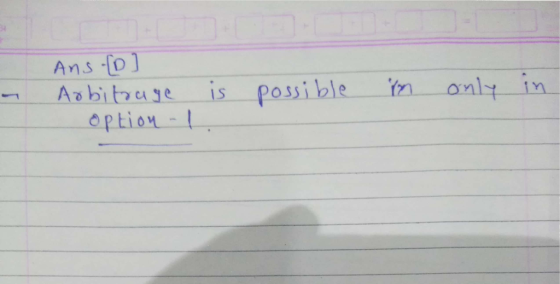

Determine if any arbitrage is possible for US Investor C) Bid Quote $1.60 Ask Quote $1.62 Spot ra...

11) (6 pts) World Nation Bank offers the following information (ignore bid/ask spreads: Spot rate...

11) (6 pts) World Nation Bank offers the following information (ignore bid/ask spreads: Spot rate on Euro 90 day forward rate on Euro Customers can borrow or deposit US dollars for 90 days at an annualized rate of 3.6% per year (0.9% per 90 days) Customers can borrow or deposit Euros for 90 days at a 1.2% per year (0.3% per 90 days) $1.118 (US$1.118/1EUR) $1.129 (US$1.129/1EUR) n annualized rate of Suppose a European investor has 100,000 Euros,if they deposit...

11) (6 pts) World Nation Bank offers the following information (ignore bid/ask spreads: Spot rate on Euro 90 day forward rate on Euro Customers can borrow or deposit US dollars for 90 days at an annualized rate of 3.6% per year (0.9% per 90 days) Customers can borrow or deposit Euros for 90 days at a 1.2% per year (0.3% per 90 days) $1.118 (US$1.118/1EUR) $1.129 (US$1.129/1EUR) n annualized rate of Suppose a European investor has 100,000 Euros,if they deposit...

15 Suppose that the current exchange rate is €1.00 - $1.60. The indirect quote from the...

15 Suppose that the current exchange rate is €1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.50 - $1.00 €1.00 - $1.60 Dy none of the options 19) The bid price A) is the price that a dealer stands ready to pay B) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

15 Suppose that the current exchange rate is €1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.50 - $1.00 €1.00 - $1.60 Dy none of the options 19) The bid price A) is the price that a dealer stands ready to pay B) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

19 Suppose that the current exchange rate is 1.00 - $1.60. The indirect quote from the...

19 Suppose that the current exchange rate is 1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.60 - $1.00 E1.00 - $1.60. D) none of the options 19) The bid price Aj is the price that a dealer stands ready to pay s) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

19 Suppose that the current exchange rate is 1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.60 - $1.00 E1.00 - $1.60. D) none of the options 19) The bid price Aj is the price that a dealer stands ready to pay s) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

a) Bid Price of New Zealand Dollar - JP Morgan Bank USD0.6533 and Well Fargo USD0.6503...

a) Bid Price of New Zealand Dollar - JP Morgan Bank USD0.6533 and Well Fargo USD0.6503 Ask Price of New Zealand Dollar - JP Morgan Bank USD0.6563 and Well Fargo USD0.6523 Justify whether locational arbitrage is possible. If so, explain the steps involved in locational arbitrage, and estimate the profit from this arbitrage if you had USD1,000,000 to use. Discuss market forces factors that would occur to eliminate any further possibilities of locational arbitrage. (6 marks) b) Currency Pair Quoted...

1. John sold a call option on Euro for $.04 per unit. The strike price was...

1. John sold a call option on Euro for $.04 per unit. The strike price was $1.30, and the spot rate at the time the option was exercised was $1.32. Assume John bought the Euro from the market if the option was exercised. Also assume that there are 100,000 units in a Euro option. What was John’s net profit on the call option? Baylor Bank believes the New Zealand dollar will appreciate over the next 20 days from $.50 to...

11) (6 pts) World Nation Bank offers the following information (ignore bid/ask spreads: Spot rate on Euro 90 day forward rate on Euro Customers can borrow or deposit US dollars for 90 days at an annualized rate of 3.6% per year (0.9% per 90 days) Customers can borrow or deposit Euros for 90 days at a 1.2% per year (0.3% per 90 days) $1.118 (US$1.118/1EUR) $1.129 (US$1.129/1EUR) n annualized rate of Suppose a European investor has 100,000 Euros,if they deposit...

11) (6 pts) World Nation Bank offers the following information (ignore bid/ask spreads: Spot rate on Euro 90 day forward rate on Euro Customers can borrow or deposit US dollars for 90 days at an annualized rate of 3.6% per year (0.9% per 90 days) Customers can borrow or deposit Euros for 90 days at a 1.2% per year (0.3% per 90 days) $1.118 (US$1.118/1EUR) $1.129 (US$1.129/1EUR) n annualized rate of Suppose a European investor has 100,000 Euros,if they deposit...

15 Suppose that the current exchange rate is €1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.50 - $1.00 €1.00 - $1.60 Dy none of the options 19) The bid price A) is the price that a dealer stands ready to pay B) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

15 Suppose that the current exchange rate is €1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.50 - $1.00 €1.00 - $1.60 Dy none of the options 19) The bid price A) is the price that a dealer stands ready to pay B) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

19 Suppose that the current exchange rate is 1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.60 - $1.00 E1.00 - $1.60. D) none of the options 19) The bid price Aj is the price that a dealer stands ready to pay s) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

19 Suppose that the current exchange rate is 1.00 - $1.60. The indirect quote from the US. perspective is A) €0.6250 - $1.00 3) €1.60 - $1.00 E1.00 - $1.60. D) none of the options 19) The bid price Aj is the price that a dealer stands ready to pay s) is the price that a dealer stands ready to sell at. is the price that the dealer has just paid for something, his historical cost of the most recent...

Most questions answered within 3 hours.

-

Your task is to design the page table for the 32bit Pentium

microprocessor. Answer the following...

asked 1 minute ago -

Although Epicurus advocates pursuing pleasure for the

good life, discuss a few reasons why he does...

asked 17 minutes ago -

Problem 1: Present entries to record the selected transactions

described below:

(a)

Issued $2,790,000 of 5-year,...

asked 23 minutes ago -

Using technology to support HR activities increases:

a.

the efficiency of the administrative HR functions.

b....

asked 24 minutes ago -

1. List the features used to classify leaf

types.

2. List some characteristics that are shared...

asked 29 minutes ago -

The three elements of Value Proposition, Key Customers, and

Capabilities operate within an environment. Which of...

asked 32 minutes ago -

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 39 minutes ago -

Each row of the table below describes an aqueous solution at

25°C

.

The second column...

asked 43 minutes ago -

A horizontal wire is at y = 0. Current travels in the +x

direction. The magnetic...

asked 44 minutes ago -

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 1 hour ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 1 hour ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 1 hour ago