What is the standard deviation of Asset M and of the portfolio equally invested in assets M, N, and O?

Could Sally reduce her total risk even more by using assets M and N only, assets M and O only, or assets N and O only? Use a 50/50 split between the asset pairs, and find the standard deviation of each asset pair.

Please show all of the steps

Homework Answers

1. Find the expected return of the equally weighted

portfolio in the three economic states.

Return of Portfolio in Boom = 1/3 (12%) + 1/3 (19%) +

1/3 (2%) = 11.00%

Return of Portfolio in Normal = 1/3 (8%) + 1/3 (11%) + 1/3 (8%) =

9.00%

Return of Portfolio in Recession = 1/3 (2%) + 1/3 (-2%) + 1/3 (12%)

= 4.00% Expected Return Portfolio = 0.30 x (11%) + 0.50 x (9%) +

0.20 x (4%)

E(rp) = 3.3% + 4.5% + 0.8% = 8.6%

2. Find the expected returns of Asset M

Expected Return Asset M = 0.30 x (12%) + 0.50 x (8%) + 0.20 x

(2%)

E(rM) = 3.6% + 4.0% + 0.4% = 8%

Find the standard deviation of Asset M and the

Portfolio.

Standard Deviation of Asset M = [0.30 x (0.12 - 0.08)2 +

0.50 x (0.08 - 0.08)2 + 0.20 x (0.02 -

0.08)2]1/2

= [(0.30 x 0.0016) + (0.20 x 0.0036)]1/2

= (0.00048 + 0.00072)1/2 = 0.00121/2

= 0.0346 or

3.46%

Standard Deviation of Portfolio = [0.30 x (0.11 -

0.086)2 + 0.50 x (0.09 - 0.086)2 + 0.20 x

(0.4 - 0.086)2]1/2

= [(0.30 x 0.0006) + (0.50 x 0.0000) + (0.20 x

0.0021)]1/2

= (0.0002 + 0.0000 + 0.0004)1/2 =

0.00061/2

= 0.0246 or

2.46%

The benefit of the

portfolio over Asset M alone is an increase in return of 0.6% and a

simultaneous reduction in total risk of 1%.

Find the return of each 50/50 portfolio in the three

different states of the economy.

Return of Portfolio M and N in Boom = 1/2 (12%) + 1/2 (19%) =

15.50%

Return of Portfolio M and N in Normal = 1/2 (8%) + 1/2 (11%) =

9.50%

Return of Portfolio M and N in Recession = 1/2 (2%) + 1/2 (-2%) =

0.00%

Return of Portfolio M and O in Boom = 1/2 (12%) + 1/2 (2%) =

7.00%

Return of Portfolio M and O in Normal = 1/2 (8%) + 1/2 (8%) =

8.00%

Return of Portfolio M and O in Recession = 1/2 (2%) + 1/2 (12%) =

7.00%

Return of Portfolio N and O in Boom = 1/2 (19%) + 1/2 (2%) =

10.50%

Return of Portfolio N and O in Normal = 1/2 (11%) + 1/2 (8%) =

9.50%

Return of Portfolio N and O in Recession = 1/2 (-2%) + 1/2 (12%) =

5.00%

Find the expected returns of each individual asset and each

50/50 combination.

Expected Return on Asset M = 0.30 x (12%) + 0.50 x (8%) + 0.20 x

(2%)

E(rM) = 3.6% + 4.0% + 0.4% = 8%

Expected Return on Asset N = 0.30 x (19%) + 0.50 x (11%) + 0.20 x

(-2%)

E(rN) = 5.7% + 5.5% - 0.4% = 10.8%

Expected Return on Asset O = 0.30 x (2%) + 0.50 x (8%) + 0.20 x

(12%)

E(rO) = 0.6% + 4.0% + 2.4% = 7%

Expected Return on Portfolio MN = 0.30 x (15.5%) + 0.50 x (9.5%) +

0.20 x (0%)

E(rMN) = 4.65% + 4.75% + 0.0% = 9.4%

Expected Return on Portfolio MO = 0.30 x (7%) + 0.50 x (8%) + 0.20

x (7%)

E(rMO) = 2.1% + 4.0% + 1.4% = 7.5%

Expected Return on Portfolio NO = 0.30 x (10.5%) + 0.50 x (9.5%) +

0.20 x (5%)

E(rNO) = 3.15% + 4.75% + 1.0% = 8.9%

Find the standard deviation of each asset and each 50/50

portfolio.

Standard Deviation of Asset M = [0.30 x (0.12 - 0.08)2 +

0.50 x (0.08 - 0.08)2 + 0.20 x (0.02 -

0.08)2]1/2

= [(0.30 x 0.0016) + (0.20 x 0.0036)]1/2

= (0.00048 + 0.00072)1/2 = 0.00121/2

= 0.0346 or

3.46%

![Standard Deviation of Asset N [0.30 × (0.19-0.108)? + 0.50 × (0.1 1-0. 108)?+ 0.20 × (-0.02-0. 108)]12 [0.30 x 0.00670.50 x 0](http://img.homeworklib.com/images/3f4bc397-5cbf-4eeb-b981-dbcfdc232b2d.png?x-oss-process=image/resize,w_560)

If Sally chose a 50/50 split between Asset M and O, the benefit is a decrease in total risk to only a half percent (0.5%).

Add Answer to:

What is the standard deviation of Asset M and of the portfolio equally invested in assets M, N, a...

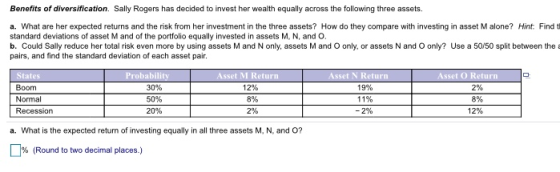

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three...

Benefits of diversification.

Sally Rogers has decided to invest her wealth equally across the

following three assets.

a. What are her expected returns and the risk from her

investment in the three assets? How do they compare with investing

in asset M alone?

Hint: Find the standard deviations of asset M and of the

portfolio equally invested in assets M, N, and O.

b. Could Sally reduce her total risk even more by using assets

M and N only, assets...

Benefits of diversification.

Sally Rogers has decided to invest her wealth equally across the

following three assets.

a. What are her expected returns and the risk from her

investment in the three assets? How do they compare with investing

in asset M alone?

Hint: Find the standard deviations of asset M and of the

portfolio equally invested in assets M, N, and O.

b. Could Sally reduce her total risk even more by using assets

M and N only, assets...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: E. a. What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint. Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and 0. b. Could Sally reduce her total risk even more by using assets M and N only,...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: E. a. What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint. Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and 0. b. Could Sally reduce her total risk even more by using assets M and N only,...

please help stuck a. What are her expected returns and the risk from her investment in the three assets? How do they compare with invessing in asset M alone? Hint Find the standard...

please help stuck

a. What are her expected returns and the risk from her investment in the three assets? How do they compare with invessing in asset M alone? Hint Find the standard deviations of asset M and of the portiolio equally investe assets M, N, and O b. Could Sally reduce her total risk even more by using assets M and N only, assets M and O only, or assets N and O only? Use a 50/50 spit between...

please help stuck

a. What are her expected returns and the risk from her investment in the three assets? How do they compare with invessing in asset M alone? Hint Find the standard deviations of asset M and of the portiolio equally investe assets M, N, and O b. Could Sally reduce her total risk even more by using assets M and N only, assets M and O only, or assets N and O only? Use a 50/50 spit between...

t udio Hop P8-24 (similar to) Benefits of diversification Sally Rogers has decided to invest her...

t udio Hop P8-24 (similar to) Benefits of diversification Sally Rogers has decided to invest her w ith equally across the following trees What we her expected retums and the risk from her investment in the vee assets? How do they compare with investing in asset Malone? Hint Find the standard deviations of asset Mand of the portfolio equally invested in assets M, N and O. b. Could Bally reduce her total risk even more by using assets M and...

t udio Hop P8-24 (similar to) Benefits of diversification Sally Rogers has decided to invest her w ith equally across the following trees What we her expected retums and the risk from her investment in the vee assets? How do they compare with investing in asset Malone? Hint Find the standard deviations of asset Mand of the portfolio equally invested in assets M, N and O. b. Could Bally reduce her total risk even more by using assets M and...

Sally Rogers has decided to invest her wealth equally across the following three assets: What are...

Sally Rogers has decided to invest her wealth equally across the following three assets: What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? (round to two decimal places)...

Sally Rogers has decided to invest her wealth equally across the following three assets. What are...

Sally Rogers has decided to invest her wealth equally across the following three assets. What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset Malone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. States Probability Asset M Return Asset N Return Asset O Return Boom 25% 14% 25% 6% Normal 45% 12% 16% 12% Recession...

What are her expected returns and the risk from her investment in the three assets? How...

What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: ? M alone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? %...

What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: ? M alone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? %...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? 11.66% (Round...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? 11.66% (Round...

8. Calculate the PORTFOLIO Expected Return and standard deviation of a 60/40 Portfolio of Asset A...

8. Calculate the PORTFOLIO Expected Return and standard deviation of a 60/40 Portfolio of Asset A and asset B. ASSET A 60% ASSET B 40% Return in State Return in State R (A) R(B) PORTFOLIO Rport in Sate S R(P)i Deviation R(P)i Pr Portfolio (Deviation Portfolio 2 State S Squared Dev*Pr Pr State P 0.4 0.6 E(R) E(R) Portfolio Portfolio Var Portfolio sd - 9. Compare the Risk-Return of the two stocks ALONE and the joint risk in the portfolio...

8. Calculate the PORTFOLIO Expected Return and standard deviation of a 60/40 Portfolio of Asset A and asset B. ASSET A 60% ASSET B 40% Return in State Return in State R (A) R(B) PORTFOLIO Rport in Sate S R(P)i Deviation R(P)i Pr Portfolio (Deviation Portfolio 2 State S Squared Dev*Pr Pr State P 0.4 0.6 E(R) E(R) Portfolio Portfolio Var Portfolio sd - 9. Compare the Risk-Return of the two stocks ALONE and the joint risk in the portfolio...

What is the expected return and standard deviation of a portfolio consisting of $4200 invested in...

What is the expected return and standard deviation of a portfolio consisting of $4200 invested in a risk-free asset with an 6.9-percent rate of return, and $1400 invested in a risky security with a 18.9-percent rate of return and a 23.9-percent standard deviation?

Benefits of diversification.

Sally Rogers has decided to invest her wealth equally across the

following three assets.

a. What are her expected returns and the risk from her

investment in the three assets? How do they compare with investing

in asset M alone?

Hint: Find the standard deviations of asset M and of the

portfolio equally invested in assets M, N, and O.

b. Could Sally reduce her total risk even more by using assets

M and N only, assets...

Benefits of diversification.

Sally Rogers has decided to invest her wealth equally across the

following three assets.

a. What are her expected returns and the risk from her

investment in the three assets? How do they compare with investing

in asset M alone?

Hint: Find the standard deviations of asset M and of the

portfolio equally invested in assets M, N, and O.

b. Could Sally reduce her total risk even more by using assets

M and N only, assets...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: E. a. What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint. Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and 0. b. Could Sally reduce her total risk even more by using assets M and N only,...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: E. a. What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint. Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and 0. b. Could Sally reduce her total risk even more by using assets M and N only,...

please help stuck

a. What are her expected returns and the risk from her investment in the three assets? How do they compare with invessing in asset M alone? Hint Find the standard deviations of asset M and of the portiolio equally investe assets M, N, and O b. Could Sally reduce her total risk even more by using assets M and N only, assets M and O only, or assets N and O only? Use a 50/50 spit between...

please help stuck

a. What are her expected returns and the risk from her investment in the three assets? How do they compare with invessing in asset M alone? Hint Find the standard deviations of asset M and of the portiolio equally investe assets M, N, and O b. Could Sally reduce her total risk even more by using assets M and N only, assets M and O only, or assets N and O only? Use a 50/50 spit between...

t udio Hop P8-24 (similar to) Benefits of diversification Sally Rogers has decided to invest her w ith equally across the following trees What we her expected retums and the risk from her investment in the vee assets? How do they compare with investing in asset Malone? Hint Find the standard deviations of asset Mand of the portfolio equally invested in assets M, N and O. b. Could Bally reduce her total risk even more by using assets M and...

t udio Hop P8-24 (similar to) Benefits of diversification Sally Rogers has decided to invest her w ith equally across the following trees What we her expected retums and the risk from her investment in the vee assets? How do they compare with investing in asset Malone? Hint Find the standard deviations of asset Mand of the portfolio equally invested in assets M, N and O. b. Could Bally reduce her total risk even more by using assets M and...

What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: ? M alone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? %...

What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: ? M alone? Hint: Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? %...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? 11.66% (Round...

Benefits of diversification. Sally Rogers has decided to invest her wealth equally across the following three assets: What are her expected returns and the risk from her investment in the three assets? How do they compare with investing in asset M alone? Hint Find the standard deviations of asset M and of the portfolio equally invested in assets M, N, and O. What is the expected return of investing equally in all three assets M, N, and O? 11.66% (Round...

8. Calculate the PORTFOLIO Expected Return and standard deviation of a 60/40 Portfolio of Asset A and asset B. ASSET A 60% ASSET B 40% Return in State Return in State R (A) R(B) PORTFOLIO Rport in Sate S R(P)i Deviation R(P)i Pr Portfolio (Deviation Portfolio 2 State S Squared Dev*Pr Pr State P 0.4 0.6 E(R) E(R) Portfolio Portfolio Var Portfolio sd - 9. Compare the Risk-Return of the two stocks ALONE and the joint risk in the portfolio...

8. Calculate the PORTFOLIO Expected Return and standard deviation of a 60/40 Portfolio of Asset A and asset B. ASSET A 60% ASSET B 40% Return in State Return in State R (A) R(B) PORTFOLIO Rport in Sate S R(P)i Deviation R(P)i Pr Portfolio (Deviation Portfolio 2 State S Squared Dev*Pr Pr State P 0.4 0.6 E(R) E(R) Portfolio Portfolio Var Portfolio sd - 9. Compare the Risk-Return of the two stocks ALONE and the joint risk in the portfolio...

Most questions answered within 3 hours.

-

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 21 minutes ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 44 minutes ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 1 hour ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 1 hour ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 1 hour ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 1 hour ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 2 hours ago -

Consider the following reaction: C 2H 2( g) + 2H 2( g) C 2H 6(

g)...

asked 2 hours ago -

Consider a 1.0 L buffer containing 0.092 mol L-1 HCOOH and 0.100

mol L-1 HCOO-. What...

asked 2 hours ago -

Koch Realty has owned a vacant land with a FMV of

$775,000 and an adjusted basis...

asked 2 hours ago -

It is estimated 29% of all adults in United States invest in

stocks and that 85%...

asked 2 hours ago -

What does a 2-sided p value of 0.04 mean? (I am not asking if it

is...

asked 2 hours ago