In the following questions, let Bt denote a Brownian motion with B0 = 0.

Homework Answers

Solution:

given that

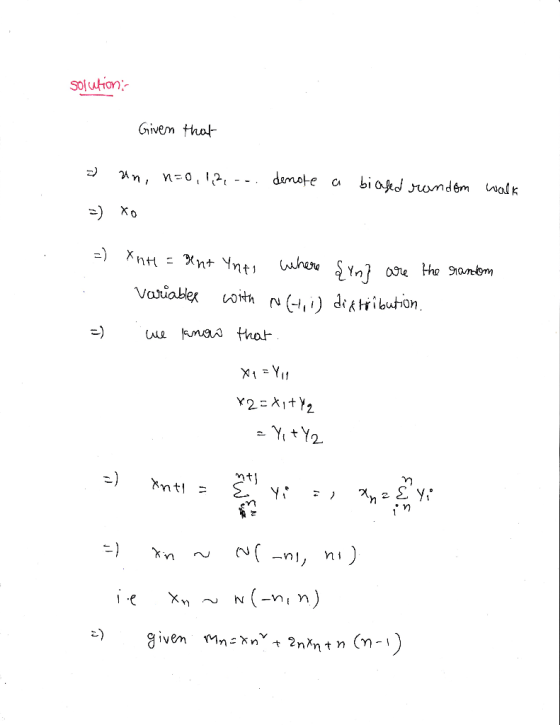

Let Xn, n-0, 1, 2, denote a biased random walk given by X0 0 and Xn+1 = Xn+Yn+1, where {Yn} are i.i.d. random variables.

Add Answer to:

In the following questions, let Bt denote a Brownian motion with B0 = 0.

In the following questions, let Bt denote a Brownian motion with B0 = 0.

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with B0 = 0.

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with B0 = 0.

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and Xo = 1. (a) Write down the SDE for Yt-eatXt, where a is a constant. (b) Find the value of a such that Yt is a martingale, and give the mean and variance of Y, in this case.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and Xo = 1. (a) Write down the SDE for Yt-eatXt, where a is a constant. (b) Find the value of a such that Yt is a martingale, and give the mean and variance of Y, in this case.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and...

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are...

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

In the following questions, let Bt denote a Brownian motion with Bo = 0. (a) Show...

In the following questions, let Bt denote a Brownian motion with Bo = 0. (a) Show that if random variables X and Y are independent then they are 1. uncorrelated, Cov(X, Y) -0. (b) Let X have distribution P(X-1)- P(X 0) P(X- -1)-1/3, and Y-İX . Show that X and Y are uncorrelated, but not independent. (c) Let (X, Y) be a Gaussian vector. Show that if X and Y are uncorrelated then they are independent.

In the following questions, let Bt denote a Brownian motion with Bo = 0. (a) Show that if random variables X and Y are independent then they are 1. uncorrelated, Cov(X, Y) -0. (b) Let X have distribution P(X-1)- P(X 0) P(X- -1)-1/3, and Y-İX . Show that X and Y are uncorrelated, but not independent. (c) Let (X, Y) be a Gaussian vector. Show that if X and Y are uncorrelated then they are independent.

2. Let Bt denote a Brownian motion. Consider the Black-Scholes model for the price of stock St, 2 So-1 and the savings account is given by β,-ea (a) Solve the equation for the price of the stock St a...

2. Let Bt denote a Brownian motion. Consider the Black-Scholes model for the price of stock St, 2 So-1 and the savings account is given by β,-ea (a) Solve the equation for the price of the stock St and show that it is not a (b) Explain what is meant by an Equivalent Martingale Measure (EMM) martingale. State the Girsanov theorem. Give the expression for Bt under the EMM Q, hence derive the expression for St under the EMM, and...

2. Let Bt denote a Brownian motion. Consider the Black-Scholes model for the price of stock St, 2 So-1 and the savings account is given by β,-ea (a) Solve the equation for the price of the stock St and show that it is not a (b) Explain what is meant by an Equivalent Martingale Measure (EMM) martingale. State the Girsanov theorem. Give the expression for Bt under the EMM Q, hence derive the expression for St under the EMM, and...

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n > 0 let Sn denote the partial sumi Let Fn denote the information co...

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n > 0 let Sn denote the partial sumi Let Fn denote the information contained in X1, ,Xn. (1) Verify that Sn nu is a martingale. (2) Assume that μ 0, verify that Sn-nơ2 is a martingale.

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n...

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n > 0 let Sn denote the partial sumi Let Fn denote the information contained in X1, ,Xn. (1) Verify that Sn nu is a martingale. (2) Assume that μ 0, verify that Sn-nơ2 is a martingale.

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n...

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be Brownian motion t 0, let T be the first time Z(t) hits a. a) Show that T, is a random time for Z(t) and for...

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be Brownian motion t 0, let T be the first time Z(t) hits a. a) Show that T, is a random time for Z(t) and for B(t). b) Show P(T, 0o)1. c) Use martingale methods to compute E [e-m] for any θ > 0 r>

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be...

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be Brownian motion t 0, let T be the first time Z(t) hits a. a) Show that T, is a random time for Z(t) and for B(t). b) Show P(T, 0o)1. c) Use martingale methods to compute E [e-m] for any θ > 0 r>

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be...

Let {X(t), 1 2 0} denote a Brownian motion 8.1. Let Y(t) = tx(1/t). (a) What is the distributio...

let {X(t), 1 2 0} denote a Brownian motion 8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion (d) Let Using (c) present an argument that

let {X(t), 1 2 0} denote a Brownian motion

8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion...

let {X(t), 1 2 0} denote a Brownian motion 8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion (d) Let Using (c) present an argument that

let {X(t), 1 2 0} denote a Brownian motion

8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion...

Let Xn is a simple random walk (p = 1/2) on {0, 1, · · · , 100} with absorbing bound- aries. Supp...

Let Xn is a simple random walk (p = 1/2) on {0, 1, · · · , 100} with absorbing bound- aries. Suppose X0 = 50. Let T = min{j : Xj = 0 or 100}. Let Fn denote the information contained in X1,··· ,Xn. (1) Verify that Xn is a martingale. (2) Find P (XT = 100). (3) Let Mn = Xn2 − n. Verify that Mn is also a martingale. (4) It is known that Mn and T...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival probability, P(Un 〉 0, for all n 0, 1, 2, ). Justify your arguments.

Consider a discrete time risk model U-2 + Σ Y" where {Yi) are iid random variables with N(2,1) distribution. Derive the lower bound for the survival...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and Xo = 1. (a) Write down the SDE for Yt-eatXt, where a is a constant. (b) Find the value of a such that Yt is a martingale, and give the mean and variance of Y, in this case.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and...

In the following questions, let Bt denote a Brownian motion with

B0 = 0.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and Xo = 1. (a) Write down the SDE for Yt-eatXt, where a is a constant. (b) Find the value of a such that Yt is a martingale, and give the mean and variance of Y, in this case.

Let Xt be the solution of SDE dX, = 3X, dt + 2XtdBt and...

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

2. Let Xn,n0,1,2,... denote a biased random walk given by Xo 0 and Xn+1 Xn + YTHI, where (X } are 1.1.d. random variables with N(-1,1) distribution. Show that Mn X22n Xn (n -1) is a martingale.

In the following questions, let Bt denote a Brownian motion with Bo = 0. (a) Show that if random variables X and Y are independent then they are 1. uncorrelated, Cov(X, Y) -0. (b) Let X have distribution P(X-1)- P(X 0) P(X- -1)-1/3, and Y-İX . Show that X and Y are uncorrelated, but not independent. (c) Let (X, Y) be a Gaussian vector. Show that if X and Y are uncorrelated then they are independent.

In the following questions, let Bt denote a Brownian motion with Bo = 0. (a) Show that if random variables X and Y are independent then they are 1. uncorrelated, Cov(X, Y) -0. (b) Let X have distribution P(X-1)- P(X 0) P(X- -1)-1/3, and Y-İX . Show that X and Y are uncorrelated, but not independent. (c) Let (X, Y) be a Gaussian vector. Show that if X and Y are uncorrelated then they are independent.

2. Let Bt denote a Brownian motion. Consider the Black-Scholes model for the price of stock St, 2 So-1 and the savings account is given by β,-ea (a) Solve the equation for the price of the stock St and show that it is not a (b) Explain what is meant by an Equivalent Martingale Measure (EMM) martingale. State the Girsanov theorem. Give the expression for Bt under the EMM Q, hence derive the expression for St under the EMM, and...

2. Let Bt denote a Brownian motion. Consider the Black-Scholes model for the price of stock St, 2 So-1 and the savings account is given by β,-ea (a) Solve the equation for the price of the stock St and show that it is not a (b) Explain what is meant by an Equivalent Martingale Measure (EMM) martingale. State the Girsanov theorem. Give the expression for Bt under the EMM Q, hence derive the expression for St under the EMM, and...

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n > 0 let Sn denote the partial sumi Let Fn denote the information contained in X1, ,Xn. (1) Verify that Sn nu is a martingale. (2) Assume that μ 0, verify that Sn-nơ2 is a martingale.

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n...

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n > 0 let Sn denote the partial sumi Let Fn denote the information contained in X1, ,Xn. (1) Verify that Sn nu is a martingale. (2) Assume that μ 0, verify that Sn-nơ2 is a martingale.

3. Suppose X1,X2, are independent identically distributed random variables with mean μ and variance σ2. Let So = 0 and for n...

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be Brownian motion t 0, let T be the first time Z(t) hits a. a) Show that T, is a random time for Z(t) and for B(t). b) Show P(T, 0o)1. c) Use martingale methods to compute E [e-m] for any θ > 0 r>

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be...

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be Brownian motion t 0, let T be the first time Z(t) hits a. a) Show that T, is a random time for Z(t) and for B(t). b) Show P(T, 0o)1. c) Use martingale methods to compute E [e-m] for any θ > 0 r>

t2s points). Let B(t) be Brownian motion and let zu) with drift u0. For any B()+ ut be...

let {X(t), 1 2 0} denote a Brownian motion 8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion (d) Let Using (c) present an argument that

let {X(t), 1 2 0} denote a Brownian motion

8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion...

let {X(t), 1 2 0} denote a Brownian motion 8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion (d) Let Using (c) present an argument that

let {X(t), 1 2 0} denote a Brownian motion

8.1. Let Y(t) = tx(1/t). (a) What is the distribution of Y(t)? (b) Compute Cov(Y(s), Y()) (c) Argue that {Y(t), t 2 0] is also Brownian motion...

Most questions answered within 3 hours.

-

The mean cost of domestic airfares in the United States rose to

an all-time high of...

asked 4 minutes ago -

1.Magazine Luiza is a Brazilian retail chain for consumer

electronics. The company currently has 100 stores...

asked 3 minutes ago -

What is the molarity of ZnCl2 that forms when 25.0 g of zinc

completely reacts with...

asked 5 minutes ago -

For independent X and Y, we have probability density function

for them where pdf of X...

asked 15 minutes ago -

The decomposition of SO2Cl2 is first order in SO2Cl2 and has a

rate constant of 1.42...

asked 12 minutes ago -

How do I convert from volume percent to mole percent in the

distillation lab? ethy acetate...

asked 18 minutes ago -

8. An air-plane has an effective wing surface area of 14.0 m²

that is generating the...

asked 19 minutes ago -

A railroad worker was a person who worked on setting and moving

railroad tracks. In securing...

asked 18 minutes ago -

using RECURSIVE Functions in Java, create a public static String

doubleLetters (String word)

For ex) that...

asked 25 minutes ago -

With a $16 Trillion national ebt, and projected annual budget

eficits in excess of $1 Trillion...

asked 39 minutes ago -

A machine shop owner wishes to assign each of three machinists

(labeled 1, 2, and 3)...

asked 53 minutes ago -

Regarding language development, which of the following

statements is FALSE?

Babies are able to cry from...

asked 52 minutes ago