![Customer list Royalty agreement PPE net Customer list [lcogs isales] [lcogs] [ipay]](http://img.homeworklib.com/images/95e9246f-3c9e-41d3-a3d5-af31f40d5ae0.png?x-oss-process=image/resize,w_560)

![[lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2013. Hint: Use negative signs with answers w](http://img.homeworklib.com/images/86c47c93-85c6-45ec-8254-c2b146bc55b0.png?x-oss-process=image/resize,w_560)

![ID) Royalty agreement Goodwill IC] Equity investment [lcogs] Liabilities and stockholders equity $93,459 Ipayl Accounts paya](http://img.homeworklib.com/images/d825f455-551f-4aa9-b7ae-3c82cd400212.png?x-oss-process=image/resize,w_560)

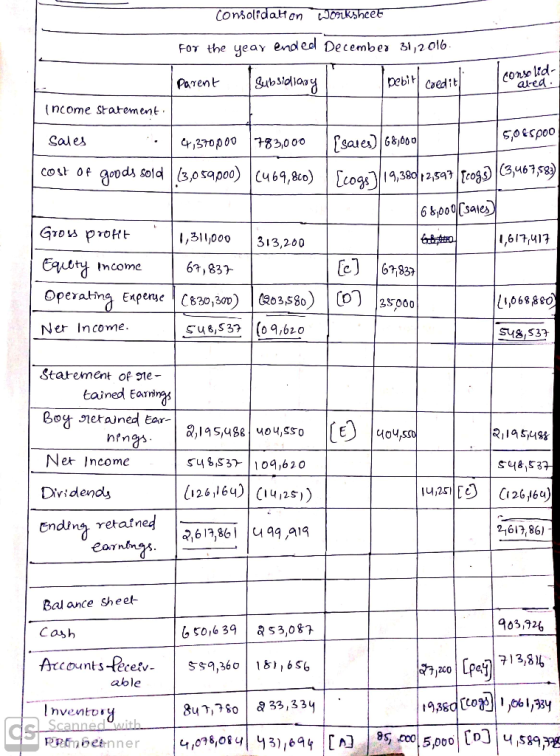

The financial statements of the parent and its subsidiary for the year ended December 31, 2013, follow in part d. below. a. Show the computation to yield the pre-consolidation $71,837 Income (loss) from subsidiary reported by the parent during 2013. Hint: Use negative signs with answers when appropriate. Plus: Less: Income (loss) from subsidiary b. Show the computation to yield the Equity Investment balance of $962,189 reported by the parent at December 31, 2013. Hint: Use negative signs with answers when appropriate. Common stock APIC Retained earnings BOY unamortized AAP BOY deferred profit Income (loss) from subsidiary Dividends

Customer list Royalty agreement PPE net Customer list [lcogs isales] [lcogs] [ipay]

[lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2013. Hint: Use negative signs with answers when appropriate Elimination Entries Sub Parent Consolidated Income statement: $787,000 [Isales] Sales $4,370,000 (469,800) [Icogs] (3,059,000) Cost of goods sold [lcogs] lsales] Gross profit 317,200 1,311,000 Income (loss) from subsidiary 71,837 IC] 203,580) [D] (830,300) Operating expenses $552,537 $113,620 Net income Statement of retained earnings 404,550 E] BOY retained earnings $2,195,488 113,620 Net income 552,537 (130,164) (14,251) Dividends

ID) Royalty agreement Goodwill IC] Equity investment [lcogs] Liabilities and stockholders' equity $93,459 Ipayl Accounts payable $327,313 Other current liabilities 403,228 127,943 Long-term liabilities 2,500,000 261,000 714,495 52,200 [E] Common stock 535,155 65,250 E] APIC 2,617,861 503,919 Retained earnings $7,098,052 $1,103,771

Homework Answers

![Royalty igiecncn o o000 0,00 o ,82 1,099, ccounts payable | 323313 | q3,459 | Cray] | 27,200 Other cuene la- 343,s72 2A43 61,](http://img.homeworklib.com/images/53da0cfe-15d2-4dbd-8cea-23a3a5cf1305.png?x-oss-process=image/resize,w_560)

Add Answer to:

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent c...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired i...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

c. Complete the consolidating entries according to the C-E-A-D-I sequence and complete the consolidation worksheet. Use...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

Consolidation spreadsheet for continuous sale of inventory-Equity method

Consolidation spreadsheet for continuous sale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1. 2016. The purchase price was S600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: The AAP assets with a definite useful life have been amortized as part of the parent's equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to...

Consolidation spreadsheet for continuous sale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1. 2016. The purchase price was S600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: The AAP assets with a definite useful life have been amortized as part of the parent's equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to...

Prepare consolidation spreadsheet for intercompany sale of equipment - Equity method Assume a parent company acquired...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and ...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary’s Stockholders’ Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) [A] Asset Initial Fair Value Useful Life...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $180,000 was assigned to an unrecorded patent owned by the subsidiary that is being amortized over a 10 year period. The [A] Patent asset has been amortized as part of the parent's equity...

Use negative signs with answers in the Consolidated column for Cost of goods sold, Operating expenses...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on January 1, 2012. The purchase price was $1,312,000 in excess of the subsidiary’s book value of Stockholders’ Equity on the acquisition date, and that excess was assigned to the following [A] assets: [A] Asset Original Amount Original Useful Life Property, plant and equipment (PPE), net $300,000 20 years Patent 432,000 12 years Goodwill 580,000 Indefinite $1,312,000 The parent company uses the cost method of...

Prepare consolidation spreadsheet for intercompany sale of equipment- Equity Method Assume a parent company acquired its...

Prepare consolidation spreadsheet for intercompany sale of equipment- Equity Method Assume a parent company acquired its subsidiary on January 1, 2015, at a purchase price that was $222,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $132,000 was assigned to a Customer List that is being amortized over a 10-year period. The remaining $90,000 was assigned to Goodwill. In January of 2018, the wholly owned subsidiary sold Equipment to the...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Most questions answered within 3 hours.

-

Choose an enzyme and tell its function and what substrate it

works on.

asked 16 seconds ago -

a) Given these data for the reaction , write the rate-law

expression.

(Use k for the...

asked 50 seconds ago -

How many moles of oxygen would be consumed during the aerobic

oxidation of one mole of...

asked 1 minute ago -

Compare two countries how the culture

of those country enhances or impedes your understanding of the...

asked 2 minutes ago -

Identify the incorrect statement.

A. An increase in mol does not increase the average force of...

asked 3 minutes ago -

In broadcast authentication, a senderaims to send

oneauthentication code for multiple receivers to verify. Explain

why...

asked 3 minutes ago -

A student studying for a vocabulary test knows the meanings of

16 words from a list...

asked 35 minutes ago -

List the most common organic functional groups that function as

acids or bases. Write an equation...

asked 16 minutes ago -

1) A protein is 435 amino acids long, which of the genes below

COULD NOT code...

asked 18 minutes ago -

What do the phenomena of overshadowing, the CS preexposure

effect, and relative validity of cues have...

asked 46 minutes ago -

Assuming air has a density of 1.17 g/L and .973 atm what is the

average molar...

asked 40 minutes ago -

Developmental Biology! Please answer all the questions

7) Mislocalization of oscar to the side of the...

asked 33 minutes ago