Explain the concepts of variance (total risk) and beta (systematic risk) in portfolio theory and the capital asset pricing model. Also explain why according to the capital asset pricing model that tot...

Explain the concepts of variance (total risk) and beta (systematic risk) in portfolio theory and the capital asset pricing model. Also explain why according to the capital asset pricing model that total risk should not be rewarded by the capital market. You may use diagrams in your explanation if you wish.

Homework Answers

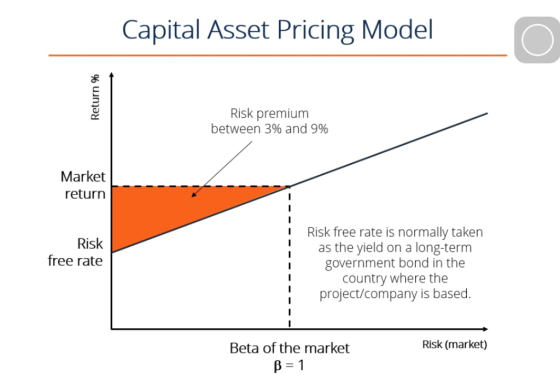

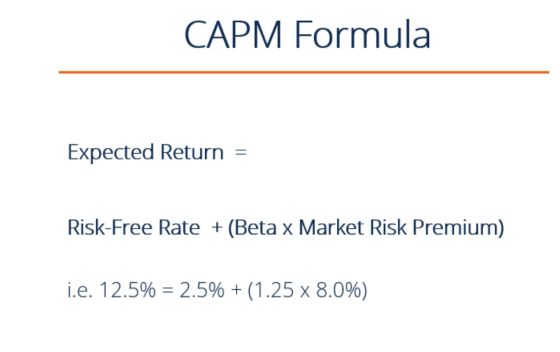

The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between the Expected Return and risk of investing in a security. It shows that the expected return on a security is equal to the risk-free return plus a Risk Premium, which is based on the Beta of that security. Below is an illustration of the CAPM concept.

CAPM Formula and Calculation

CAPM is calculated according to the following formula:

![[Ba x (Rm - Rrf)] Ra Rrf](http://img.homeworklib.com/images/8c12f59b-0439-4fba-9d5b-6d0c8704298b.png?x-oss-process=image/resize,w_560)

Where:

Ra = Expected return on a security

Rrf = Risk-free rate

Ba = Beta of the security

Rm = Expected return of the market

Note: “Risk Premium” = (Rm – Rrf)

The CAPM formula is used for calculating the expected returns of an asset. It is based on the idea of systematic risk (otherwise known as or non-diversifiable risk) and that investors need to be compensated for it in the form of a risk premium. A risk premium is a rate of return greater than the risk-free rate. When investing, investors desire a higher risk premium when taking on more risky investments.

Expected Return

The “Ra” notation above represents the expected return of a capital asset over time, given all of the other variables in the equation. “Expected return” is a long-term assumption about how an investment will play out over its entire life.

Risk-Free Rate

The “Rrf” notation is for the risk-free rate, which is typically equal to the yield on a 10-year US government bond. The risk-free rate should correspond to the country where the investment is being made, and the maturity of the bond should match the time horizon of the investment. Professional convention, however, is to typically use the 10-year rate no matter what, because it’s the most heavily quoted and most liquid bond.

To learn more, check out CFI’s Free Fixed Income Fundamentalscource

Beta

The beta (denoted as “Ba” in the CAPM formula) is a measure of a stock’s risk (volatility of returns) reflected by measuring the fluctuation of its price changes relative to the overall market. In other words, it is the stock’s sensitivity to market risk. For instance, if a company’s beta is equal to 1.5 the security has 150% of the volatility of the market average. However, if the beta is equal to 1, the expected return on a security is equal to the average market return. A beta of -1 means security has a perfect negative correlation with the market.

To learn more: read about Answer beta Vs Equity Beta.

Market Risk Premium

From the above components of CAPM, we can simplify the formula to reduce “expected return of the market minus the risk-free rate” to be simply the “market risk premium”. The market risk premium.represents the additional return over and above the risk-free rate, which is required to compensate investors for investing in a riskier assets Class. Put another way, the more volatile a market or an asset class is, the higher the market risk premium will be.

Video Explanation of CAPM

Below is a short video explanation of how the Capital Asset Pricing Model works and why it’s important for financial modeling and valuation in corporate finance. To learn more, check out CFI’s Finacial Analyst Course

Why CAPM is Important

The CAPM formula is widely used in the finance industry. It is vital in calculating the Weighted Average cost of capital (WACC) as CAPM computes the cost of equity.

WACC is used extensively in financial Model. It can be used to find the net present value (NPV) of the future cash flows of an investment and to further calculate its Enterprise value and finally its equity value.

CAPM Example – Calculation of Expected Return

Let’s calculate the expected return on a stock, using the Capital Asset Pricing Model (CAPM) formula. Suppose the following information about a stock is known:

It trades on the NYSE and its operations are based in the United StatesCurrent yield on a U.S. 10-year treasury is 2.5%The average excess historical annual return for U.S. stocks is 7.5%The beta of the stock is 1.25 (meaning it’s average weekly return is 1.25x as volatile as the S&P500 over the last 2 years)

What is the expected return of the security using the CAPM formula?

Let’s break down the answer using the formula from above in the article:

Expected return = Risk Free Rate + [Beta x Market Return Premium]Expected return = 2.5% + [1.25 x 7.5%]Expected return = 11.9%

Add Answer to:

Explain the concepts of variance (total risk) and beta (systematic risk) in portfolio theory and the capital asset pricing model. Also explain why according to the capital asset pricing model that tot...

Explain the concepts of variance (total risk) and beta (systematic risk) in portfolio theory and the...

Explain the concepts of variance (total risk) and beta (systematic risk) in portfolio theory and the capital asset pricing model. Also explain why according to the capital asset pricing model that total risk should not be rewarded by the capital market. You may use diagrams in your explanation if you wish.

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important?...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Nce theory, the Capital Asset pricing Model postulates a relationship between the ticular stock a...

nce theory, the Capital Asset pricing Model postulates a relationship between the ticular stock and the market return" according to the following model: R,Return on asset i, R Return on the market as a whole, The risk-free rate of return. rp An asset's risk premium is the excess of its return over the risk-free rate, therefore this equation premia fluctuate more than one-for-one with the market are called aggressive assets. 1. Use the data provided to you here below to...

nce theory, the Capital Asset pricing Model postulates a relationship between the ticular stock and the market return" according to the following model: R,Return on asset i, R Return on the market as a whole, The risk-free rate of return. rp An asset's risk premium is the excess of its return over the risk-free rate, therefore this equation premia fluctuate more than one-for-one with the market are called aggressive assets. 1. Use the data provided to you here below to...

Capital Asset Pricing model

a. Fill in the missing values in the table. b. Is the stock of Firm A correctly priced according to the capital-asset-pricing model (CAPM)? What about the stock ofFirm B? Firm C? If these securities are not correctly priced, what is your investment recommendation for someone with a well-diversified portfolio?You have been provided the following data on the securities of three firms, the market portfolio, and the risk-free asset:Security Expected Return Standard Deviation Correlation BetaFirm A 0.13 0.12 ? 0.9Firm...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. Calculate beta for GE. a) Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. Calculate beta for GE. a) Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. a) Calculate beta for GE. Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. a) Calculate beta for GE. Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

One key result of applying the Capital Asset Pricing Model is that the risk and return...

One key result of applying the Capital Asset Pricing Model is that the risk and return of an individual security should be analyzed by how that security affects the risk and return of the portfolio in which it is held. True False Portfolio diversification reduces the impact of market risk on the portfolio. True False Market risk refers to the tendency of a stock to move with the general economy. A stock with aboveaverage market risk will tend to be...

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's...

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

Question 2 (30 points) 2.1 (12 points) State the assumptions of the Capital Asset Pricing Model...

Question 2 (30 points) 2.1 (12 points) State the assumptions of the Capital Asset Pricing Model (CAPM). Explain and, where relevant, demonstrate on a graph the following concepts: (a) Capital Market Equilibrium in CAPM (b) Capital Market Line (c) Expected return for an arbitrary asset j: E(r;) = PRE + B,(E(TM) - PRF). Contrast this with the expected return on an efficient portfolio (d) Systematic and idiosyncratic risk

Question 2 (30 points) 2.1 (12 points) State the assumptions of the Capital Asset Pricing Model (CAPM). Explain and, where relevant, demonstrate on a graph the following concepts: (a) Capital Market Equilibrium in CAPM (b) Capital Market Line (c) Expected return for an arbitrary asset j: E(r;) = PRE + B,(E(TM) - PRF). Contrast this with the expected return on an efficient portfolio (d) Systematic and idiosyncratic risk

Capital Asset Pricing Model Risk-free rate = 5% Return the (stock) Market = 12% Beta =...

Capital Asset Pricing Model Risk-free rate = 5% Return the (stock) Market = 12% Beta = 1.5 Calculate the cost of retained earnings using the Capital Asset Pricing Model.

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

nce theory, the Capital Asset pricing Model postulates a relationship between the ticular stock and the market return" according to the following model: R,Return on asset i, R Return on the market as a whole, The risk-free rate of return. rp An asset's risk premium is the excess of its return over the risk-free rate, therefore this equation premia fluctuate more than one-for-one with the market are called aggressive assets. 1. Use the data provided to you here below to...

nce theory, the Capital Asset pricing Model postulates a relationship between the ticular stock and the market return" according to the following model: R,Return on asset i, R Return on the market as a whole, The risk-free rate of return. rp An asset's risk premium is the excess of its return over the risk-free rate, therefore this equation premia fluctuate more than one-for-one with the market are called aggressive assets. 1. Use the data provided to you here below to...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. Calculate beta for GE. a) Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. Calculate beta for GE. a) Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. a) Calculate beta for GE. Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

Question 3. Capital asset pricing model. (2 points) The expected return on the market portfolio is 9%. The risk free rate is 5%. The variance of the market portfolio returns is 0.08 and the covariance of the market and GE returns is 0.06. a) Calculate beta for GE. Interpret what beta means. b) Calculate the expected return for GE stock, how is it compared to the expected return on the market portfolio? c) If you form a portfolio with 75%...

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

Question 2 (30 points) 2.1 (12 points) State the assumptions of the Capital Asset Pricing Model (CAPM). Explain and, where relevant, demonstrate on a graph the following concepts: (a) Capital Market Equilibrium in CAPM (b) Capital Market Line (c) Expected return for an arbitrary asset j: E(r;) = PRE + B,(E(TM) - PRF). Contrast this with the expected return on an efficient portfolio (d) Systematic and idiosyncratic risk

Question 2 (30 points) 2.1 (12 points) State the assumptions of the Capital Asset Pricing Model (CAPM). Explain and, where relevant, demonstrate on a graph the following concepts: (a) Capital Market Equilibrium in CAPM (b) Capital Market Line (c) Expected return for an arbitrary asset j: E(r;) = PRE + B,(E(TM) - PRF). Contrast this with the expected return on an efficient portfolio (d) Systematic and idiosyncratic risk

Most questions answered within 3 hours.

-

A car drives over the crest of a hill of radius 120m with a

speed of...

asked 1 second ago -

Implementation of a MapReduce-style distributed word count

application

For this assignment, you can use any programming...

asked 7 minutes ago -

In females, the labia swells and the vagin-a lubricates during

which phase of the sexual response...

asked 38 minutes ago -

2. An item costs a retailer $200. If a 30 percent markup is

desired, what should...

asked 40 minutes ago -

Your client, Anita, is hurt in a car accident and comes to you

for some advice....

asked 51 minutes ago -

how many mL of 0.1050 M NaOH is needed to reach a pH of 3.74

when...

asked 47 minutes ago -

QUESTION

Memory retrieval that is easier when the person is in the same

psychological condition during...

asked 50 minutes ago -

The mean annual inflation rate in the UNited States over the

past 98 years in 3.37%...

asked 57 minutes ago -

Design a class Holiday that represents a

holiday during the year. This class has three

private...

asked 1 hour ago -

Problem 1 (Logistic Regression and KNN). In this problem, we

predict Direction using the data Weekly.csv....

asked 1 hour ago -

What is the difference between VNTRs (Variable Number Tandem

Repeats) and STRs (Short Tandem Repeats) used...

asked 1 hour ago -

Fill in

Isotope: 15 O

1. Element name:

2. Atomic number:

3. Mass number:

4. Number...

asked 1 hour ago