Linear statistical models

For ridge regression, we choose parameter estimators b which minimise

where

Show that these estimators are given by

Homework Answers

Add Answer to:

Linear statistical models For ridge regression, we choose parameter estimators b which minimise where is a constant penalty parameter. Show that these estimators are given by 7n i=1 We were unable...

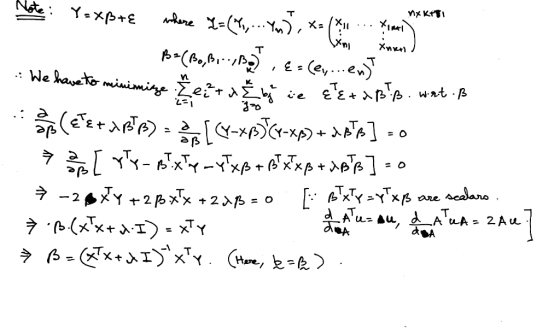

5. For ridge regression, we choose parameter estimators b which minimise i-1 j-0 where λ is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regressio...

5. For ridge regression, we choose parameter estimators b which minimise i-1 j-0 where λ is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter 0.5. In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that it is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise i-1 j-0 where λ is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter 0.5. In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that it is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise j-0 where A is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regres...

5. For ridge regression, we choose parameter estimators b which minimise j-0 where A is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter λ-0.5 In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that t is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise j-0 where A is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter λ-0.5 In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that t is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

Let Y = Xβ + ε be the linear model where X be an n ×...

Let Y = Xβ + ε be the linear model where X be an n × p matrix with orthonormal columns (columns of X are orthogonal to each other and each column has length 1) Let be the least-squares estimate of β, and let be the ridge regression estimate with tuning parameter λ. Prove that for each j, . Note: The ridge regression estimate is given by: The least squares estimate is given by: We were unable to transcribe this...

We have a regression equation: I) (restricted form , ) We want to do a Ramsey-Reset...

We have a regression equation: I) (restricted form , ) We want to do a Ramsey-Reset test and form the alternative hypothesis that the true functional form of the regression is: II) But in our econometrics class it is said that due to the inclusion of in the alternative form (unrestricted form) we say that this regression can not be estimated and its estimators can not be found. It is said that the reason behind it is multicollinearity and by...

1. Use (where is the 4x4 identity matrix) to show that a) with C a constant....

1. Use

(where

is the 4x4 identity matrix) to show that

a)

with C a constant. Calculate C

b)

with D a constant. Calculate D

c)

{74,7"} = 294V14 We were unable to transcribe this imageWilly d y = Cy! with many = Dga We were unable to transcribe this image

1. Use

(where

is the 4x4 identity matrix) to show that

a)

with C a constant. Calculate C

b)

with D a constant. Calculate D

c)

{74,7"} = 294V14 We were unable to transcribe this imageWilly d y = Cy! with many = Dga We were unable to transcribe this image

1. After having estimated a regression model , we wish to forecast the value of given a new ob...

1. After having estimated a regression model , we wish to forecast the value of given a new observation . We can consider two types of predictions: forecasting the conditional mean of , or forecasting the actual value of . What is true about the variances of these predictions? Var[conditional mean] > Var[actual value]. Var[conditional mean] = Var[actual value]. Var[conditional mean] < Var[actual value]. Var[conditional mean] may be larger than Var[actual value] in some data sets and smaller in others....

4. We have n statistical units. For unit i, we have (x; yi), for i 1,2,...,n. We used the least squares line to obtain the estimated regression line bobi . (a) Show that the centroid (z, y) is a poin...

4. We have n statistical units. For unit i, we have (x; yi), for i 1,2,...,n. We used the least squares line to obtain the estimated regression line bobi . (a) Show that the centroid (z, y) is a point on the least squares line, where x-(1/n) Σ-Χί and у-(1/ n) Σ|-1 yi. (Hint: Evaluate the line at x x.) (b) In the suggested exercises, we showed that e,-0 and where e is the ith residual, that is e -y...

4. We have n statistical units. For unit i, we have (x; yi), for i 1,2,...,n. We used the least squares line to obtain the estimated regression line bobi . (a) Show that the centroid (z, y) is a point on the least squares line, where x-(1/n) Σ-Χί and у-(1/ n) Σ|-1 yi. (Hint: Evaluate the line at x x.) (b) In the suggested exercises, we showed that e,-0 and where e is the ith residual, that is e -y...

Consider the linear differential equation , with given matrix. Provide an example of for which the Lyapunov condition for the stability of the origin is satisfied and show the consequences on the O...

Consider the linear differential equation , with given matrix. Provide an example of for which the Lyapunov condition for the stability of the origin is satisfied and show the consequences on the ODE solutions. We were unable to transcribe this imagenxn We were unable to transcribe this image nxn

We were unable to transcribe this imageWe were unable to transcribe this imageUse the regression line to estimate the number of trials it would take to leam these tricks if a dolphin received...

We were unable to transcribe this imageWe were unable to transcribe this imageUse the regression line to estimate the number of trials it would take to leam these tricks if a dolphin received five treats per trick. Y for X _ 5 would be The head dolphin trainer wants to save money by cutting down on the number of treats the dolphins get. She has asked you to use the least-squares regression line to predict how fast the dolphins can...

We were unable to transcribe this imageWe were unable to transcribe this imageUse the regression line to estimate the number of trials it would take to leam these tricks if a dolphin received five treats per trick. Y for X _ 5 would be The head dolphin trainer wants to save money by cutting down on the number of treats the dolphins get. She has asked you to use the least-squares regression line to predict how fast the dolphins can...

5. For ridge regression, we choose parameter estimators b which minimise i-1 j-0 where λ is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter 0.5. In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that it is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise i-1 j-0 where λ is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter 0.5. In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that it is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise j-0 where A is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter λ-0.5 In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that t is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

5. For ridge regression, we choose parameter estimators b which minimise j-0 where A is a constant penalty parameter. (a) Show that these estimators are given by (b) Calculate the ridge regression estimates for the data from Q2 with penalty parameter λ-0.5 In order to avoid penalising some parameters unfairly, we must first scale every predictor variable so that t is standardised (mean 0, variance 1), and centre the response variable (mean 0), in which case an intercept parameter...

1. Use

(where

is the 4x4 identity matrix) to show that

a)

with C a constant. Calculate C

b)

with D a constant. Calculate D

c)

{74,7"} = 294V14 We were unable to transcribe this imageWilly d y = Cy! with many = Dga We were unable to transcribe this image

1. Use

(where

is the 4x4 identity matrix) to show that

a)

with C a constant. Calculate C

b)

with D a constant. Calculate D

c)

{74,7"} = 294V14 We were unable to transcribe this imageWilly d y = Cy! with many = Dga We were unable to transcribe this image

4. We have n statistical units. For unit i, we have (x; yi), for i 1,2,...,n. We used the least squares line to obtain the estimated regression line bobi . (a) Show that the centroid (z, y) is a point on the least squares line, where x-(1/n) Σ-Χί and у-(1/ n) Σ|-1 yi. (Hint: Evaluate the line at x x.) (b) In the suggested exercises, we showed that e,-0 and where e is the ith residual, that is e -y...

4. We have n statistical units. For unit i, we have (x; yi), for i 1,2,...,n. We used the least squares line to obtain the estimated regression line bobi . (a) Show that the centroid (z, y) is a point on the least squares line, where x-(1/n) Σ-Χί and у-(1/ n) Σ|-1 yi. (Hint: Evaluate the line at x x.) (b) In the suggested exercises, we showed that e,-0 and where e is the ith residual, that is e -y...

We were unable to transcribe this imageWe were unable to transcribe this imageUse the regression line to estimate the number of trials it would take to leam these tricks if a dolphin received five treats per trick. Y for X _ 5 would be The head dolphin trainer wants to save money by cutting down on the number of treats the dolphins get. She has asked you to use the least-squares regression line to predict how fast the dolphins can...

We were unable to transcribe this imageWe were unable to transcribe this imageUse the regression line to estimate the number of trials it would take to leam these tricks if a dolphin received five treats per trick. Y for X _ 5 would be The head dolphin trainer wants to save money by cutting down on the number of treats the dolphins get. She has asked you to use the least-squares regression line to predict how fast the dolphins can...

Most questions answered within 3 hours.

-

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 47 minutes ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 49 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 48 minutes ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 1 hour ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 1 hour ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 1 hour ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 1 hour ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 1 hour ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 1 hour ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 1 hour ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 1 hour ago -

Calculate the expected value, the variance, and the standard

deviation of the given random variable X....

asked 2 hours ago