According to contemporary investment theory it is safer to diversify your portfolio by selecting a variety of investments rather than choosing a single investment option. Using the problem solved in class add constraints so that each fund type is used for a minimum of 5% of the total portfolio. (the optimal solution should indicate to total annual return of 17.56%) Complete the same SolverTable by changing beta with the new model that incorporates the new constraints. Describe the differences between the two sets of SolverTable results. What is your conclusion about portfolio diversification as it relates to risk tolerance (changes in the beta)?

this is the question solved in class

Please leave your calculation below

thanks!

Portfolio Selection Problem In this problem you will examine the allocations of investor funds among six categories of mutual funds for the bull market of the late 1990s. To maximize total annual return (unadjusted for risk), investors allocate money across the six fund categories whose average annual returns and betas (risk) are given below. As long as the returns are positive an investor should ensure that 100% of available investment funds are actually invested. Investors also typically make investment choices based on risk tolerance. To begin you will assume that your risk tolerance is very high (no risk is too great). Hint: you should set up a non-binding constraint for risk (beta). In the event of another bull market similar to the late 1990's, you will have a guideline for investment decisions if you find the optimal allocation of investment funds for this historical time period by maximizing total annual return. fter determining the optimal investment strategy for a high risk portfolio, use SolverTable to see if the total annual return and investment strategy change for lower levels of risk (vary beta from .43 to 1.13 in increments of 0.05) 1

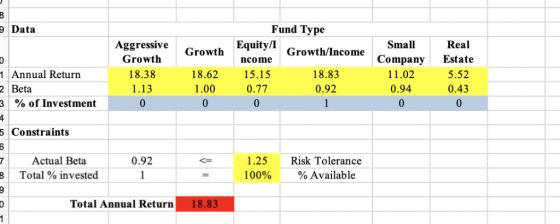

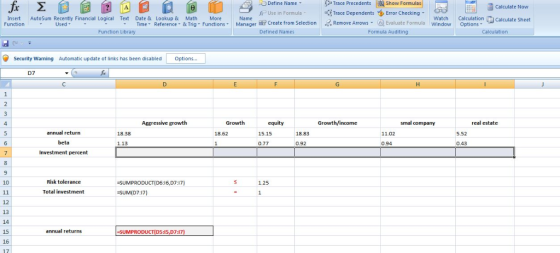

Fund Type 9 Data Aggressive Growth Equity/I Small Real Growth/Income Growth Company Estate ncome 18.38 18.83 11.02 0.94 1 Annual Return 5.52 18.62 15.15 1.13 2 Beta 1.00 0.77 0.92 0.43 3 % of Investment 5 Constraints 1.25 Risk Tolerance Actual Beta 0.92 Total % invested 100% %Available Total Annual Return 18.83

Homework Answers

The Beta(risk) of products range from 0.43 -1.13. An investor should have a risk tolerance of at least 0.43 if he wants to invest in any of these products. The maximum risk due to investment is 1.13

Option 1- Initial question

We need to

- find the percent of investment in each product

- so that we maximize profit

- subject to constraints

Decision variable

xi= the percent of investment ion each product

i=1,2,3,4,5,6

objective

maximize

Profit= 18.38 X1 + 18.62 X2 + 15.15 X3 + 18.83 X4 + 11.02 X5 + 5.52 X6

Constraints

1.13 X1 +1X2+0.77X3+0.92X4+0.94X5+0.43X6 ≤1.25

X1 +X2+X3+X4+X5+X6 = 1

Xi ≥ 0 (non-negativity )

|

Cells |

Name |

Final Value |

Shadow Price |

RHS Value |

Allowable Increase |

Allowable Decrease |

|

D10<=F10 |

Risk tolerance Aggressive growth |

0.92 |

0 |

1.25 |

1E+100 |

0.33 |

- The shadow price is zero – Non-binding constraint. Binding constraints have shadow price e.g. Total investment Aggressive growth

- Se the allowable increase and decrease

1,25 + ( 1E+100) à (huge number)

1.25- 0.33 =0.92

Between risk tolerance values of 0.92 and 1,25 + ( 1E+100), the shadow price of risk tolerance is 0. The constraint is non-binding ie risk tolerance is not a limiting factor of the profit, within this range of value

Option 2- After adding an additional constraint of

Xi ≥ 0.05

|

Cells |

Name |

Final Value |

Shadow Price |

RHS Value |

Allowable Increase |

Allowable Decrease |

|

D10<=F10 |

Risk tolerance Aggressive growth |

0.9035 |

0 |

1.25 |

1E+100 |

0.3465 |

- The shadow price is zero – Non-binding constraint.

- Se the allowable increase and decrease:

0.9035 + ( 1E+100) à (huge number)

0.9035 - 0.3465=0.557

Between risk tolerance values of 0.557 and 0.9035 + (1E+100) the shadow price of risk tolerance is 0. The constraint is non-binding ie risk tolerance is not a limiting factor of the profit, within this range of value

![f Cells 1 OpenSolver Sensitivity Report CBC 2 Worksheet: [may 19.xlsx] Sheet19 Sensitivity 1 3 Report Created: 01-06-2019 09:](http://img.homeworklib.com/images/f7943832-95db-4fdb-b55d-dfdbefd6b9ff.png?x-oss-process=image/resize,w_560)

Comparison

Comparing the two, we find that lower limit of risk tolerance range has increased for the second option. So even if the risk tolerance of investor decreases to a very lower level i.e. he becomes very risk averse, the profit is not going to be affected

So, with portfolio diversification, even an investor with lower risk tolerance can invest and can reap similar profit

Add Answer to:

According to contemporary investment theory it is safer to diversify your portfolio by selecting a variety of investment...

Problem 7-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfol...

Problem 7-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected...

Problem 7-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Problem 2-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfol...

Problem 2-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its dients A dlient who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, whereas the Blue Chip fund has a projected...

Problem 2-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its dients A dlient who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, whereas the Blue Chip fund has a projected...

Question: Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment po...

Question: Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios d... Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $55,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios d...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $55,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 11%, while the Blue Chip fund has a projected annual return...

International investment diversification Personal Finance Problem The economies of the world tend to rise and fall...

International investment diversification Personal Finance Problem The economies of the world tend to rise and fall in cycles that offset each other. International stocks can provide possible diversification for a portfolio heavy on U.S. equities. Because research on foreign companies is usually difficult for individual investors to track on their own, a foreign equity mutual fund offers the investor the expertise of a global fund manager. Foreign-stock funds provide exposure to overseas markets at varying levels of risk. Economic and...

International investment diversification Personal Finance Problem The economies of the world tend to rise and fall in cycles that offset each other. International stocks can provide possible diversification for a portfolio heavy on U.S. equities. Because research on foreign companies is usually difficult for individual investors to track on their own, a foreign equity mutual fund offers the investor the expertise of a global fund manager. Foreign-stock funds provide exposure to overseas markets at varying levels of risk. Economic and...

Q1: Data Portfolio - Investment choices: Stock fund, Money Market (MM) fund 1 unit of Stock fund-...

Please post screenshots of excel file

Q1: Data Portfolio - Investment choices: Stock fund, Money Market (MM) fund 1 unit of Stock fund- $50 1 unit of Stock fund carries 8 units of risk Return on 1 unit of Stock fund: $5 A minimum of 3000 units of MM fund should be in the portfolio. Funds available: $1,200,000 Minimum portfolio return desired (return from stock + return from MM): $60,000 Goal is to minimize total risk. Formulate the problem using:...

Please post screenshots of excel file

Q1: Data Portfolio - Investment choices: Stock fund, Money Market (MM) fund 1 unit of Stock fund- $50 1 unit of Stock fund carries 8 units of risk Return on 1 unit of Stock fund: $5 A minimum of 3000 units of MM fund should be in the portfolio. Funds available: $1,200,000 Minimum portfolio return desired (return from stock + return from MM): $60,000 Goal is to minimize total risk. Formulate the problem using:...

Please walk me through steps to enter into excel! Thank you. 10. An investment advisor at...

Please walk me through steps to enter into excel!

Thank you.

10. An investment advisor at Shore Financial Services wants to develop a model that can be used to allocate investment funds among four alternatives: stocks, bonds, mutual funds, and cash. For the coming investment period, the company developed estimates of the annual rate of return and the associated risk for each alternative. Risk is measured using an index between 0 and 1, with higher risk values denoting more volatility...

Please walk me through steps to enter into excel!

Thank you.

10. An investment advisor at Shore Financial Services wants to develop a model that can be used to allocate investment funds among four alternatives: stocks, bonds, mutual funds, and cash. For the coming investment period, the company developed estimates of the annual rate of return and the associated risk for each alternative. Risk is measured using an index between 0 and 1, with higher risk values denoting more volatility...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Problem 7-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected...

Problem 7-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Problem 2-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its dients A dlient who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, whereas the Blue Chip fund has a projected...

Problem 2-27 Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its dients A dlient who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, whereas the Blue Chip fund has a projected...

International investment diversification Personal Finance Problem The economies of the world tend to rise and fall in cycles that offset each other. International stocks can provide possible diversification for a portfolio heavy on U.S. equities. Because research on foreign companies is usually difficult for individual investors to track on their own, a foreign equity mutual fund offers the investor the expertise of a global fund manager. Foreign-stock funds provide exposure to overseas markets at varying levels of risk. Economic and...

International investment diversification Personal Finance Problem The economies of the world tend to rise and fall in cycles that offset each other. International stocks can provide possible diversification for a portfolio heavy on U.S. equities. Because research on foreign companies is usually difficult for individual investors to track on their own, a foreign equity mutual fund offers the investor the expertise of a global fund manager. Foreign-stock funds provide exposure to overseas markets at varying levels of risk. Economic and...

Please post screenshots of excel file

Q1: Data Portfolio - Investment choices: Stock fund, Money Market (MM) fund 1 unit of Stock fund- $50 1 unit of Stock fund carries 8 units of risk Return on 1 unit of Stock fund: $5 A minimum of 3000 units of MM fund should be in the portfolio. Funds available: $1,200,000 Minimum portfolio return desired (return from stock + return from MM): $60,000 Goal is to minimize total risk. Formulate the problem using:...

Please post screenshots of excel file

Q1: Data Portfolio - Investment choices: Stock fund, Money Market (MM) fund 1 unit of Stock fund- $50 1 unit of Stock fund carries 8 units of risk Return on 1 unit of Stock fund: $5 A minimum of 3000 units of MM fund should be in the portfolio. Funds available: $1,200,000 Minimum portfolio return desired (return from stock + return from MM): $60,000 Goal is to minimize total risk. Formulate the problem using:...

Please walk me through steps to enter into excel!

Thank you.

10. An investment advisor at Shore Financial Services wants to develop a model that can be used to allocate investment funds among four alternatives: stocks, bonds, mutual funds, and cash. For the coming investment period, the company developed estimates of the annual rate of return and the associated risk for each alternative. Risk is measured using an index between 0 and 1, with higher risk values denoting more volatility...

Please walk me through steps to enter into excel!

Thank you.

10. An investment advisor at Shore Financial Services wants to develop a model that can be used to allocate investment funds among four alternatives: stocks, bonds, mutual funds, and cash. For the coming investment period, the company developed estimates of the annual rate of return and the associated risk for each alternative. Risk is measured using an index between 0 and 1, with higher risk values denoting more volatility...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Blair & Rosen, Inc. (B&R) is a brokerage firm that specializes in investment portfolios designed to meet the specific risk tolerances of its clients. A client who contacted B&R this past week has a maximum of $50,000 to invest. B&R's investment advisor decides to recommend a portfolio consisting of two investment funds: an Internet fund and a Blue Chip fund. The Internet fund has a projected annual return of 12%, while the Blue Chip fund has a projected annual return...

Most questions answered within 3 hours.

-

Q1b. Provide an example of how pricing should interact

with the services offered by the retailer.

asked 55 seconds from now -

a mass weighing 8 pounds when attached to a spring, stretches

it 6 inches.the object is...

asked 6 minutes ago -

The following is part of the computer output from a regression

of monthly returns on Waterworks...

asked 10 minutes ago -

Bob Katz is purchasing a new Honda Pilot for $35,000. He is

financing $30,000 with a...

asked 14 minutes ago -

The equity holders of Super Nova, Inc. have 100 million of

equity in the firm. Because...

asked 13 minutes ago -

A sample of 240 observations is selected from a normal

population with a population standard deviation...

asked 29 minutes ago -

Write an (efficient) pseudocode for the implementation of each

of the following function prototypes (proper C...

asked 28 minutes ago -

Klingon Widgets, Inc., purchased new cloaking machinery three

years ago for $5.6 million. The machinery can...

asked 32 minutes ago -

Social work's goal of social betterment implies

A. That social workers should be models of good...

asked 29 minutes ago -

a

12 kg box sits on a horizontal table. a string with tension 30.4 N

pulls...

asked 31 minutes ago -

A circular coil of radius 0.120 m contains a single turn and is

located in a...

asked 43 minutes ago -

help me out

Velocity v = גf, wavelength ג = v/f and

Relative frequency = frequency...

asked 50 minutes ago