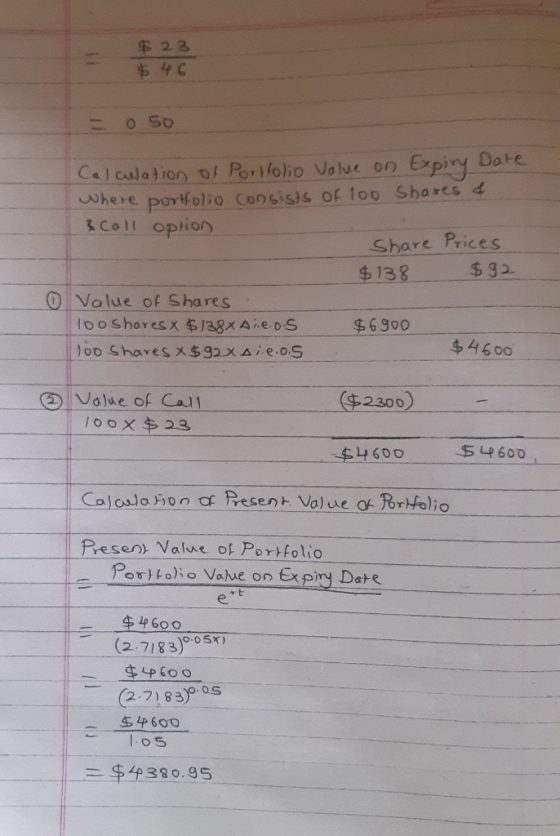

. The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual...

. The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work.

1.Using the binomial tree, compute the price at time 0 of a one-year European call option on 100 shares of stock with a strike price of $115 per share and show that put-call parity holds.

Homework Answers

Add Answer to:

. The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual...

The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. 1)Using the binomial tree, compute the price at time 0 of a one-year European put option on 100 shares of...

The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work. How would you hedge a long position in the American put option at time 0?

The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work. Compute u, d, as well as p for the standard binomial model.

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

15: Interest rates are 10% per annum continuously compounded. The price of the stock is currently...

15: Interest rates are 10% per annum continuously compounded. The price of the stock is currently $100 per share. In one year the price will be either $125 per share or $75 per share. Using a one period Binomial Tree Model as outlined in Section 75, find the value, now, of the call option with exercise price of 100. What is the hedge ratio? Now calculate the answers for exercise prices of 90 and 110.

15: Interest rates are 10% per annum continuously compounded. The price of the stock is currently $100 per share. In one year the price will be either $125 per share or $75 per share. Using a one period Binomial Tree Model as outlined in Section 75, find the value, now, of the call option with exercise price of 100. What is the hedge ratio? Now calculate the answers for exercise prices of 90 and 110.

1a) The current price of a stock is $43, and the continuously compounded risk-free rate is...

1a) The current price of a stock is $43, and the continuously compounded risk-free rate is 7.5%. The stock pays a continuous dividend yield of 1%. A European call option with a exercise price of $35 and 9 months until expiration has a current value of $11.08. What is the value of a European put option written on the stock with the same exercise price and expiration date as the call? Answers: a. $5.17 b. $3.08 c. $1.49 d. $2.50...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to be 0.30 and its dividend yield is 0.03. The continuously-compounded, risk-free interest rate equals 0.06. Consider a $95-strike European put option on the above stock with three months to expiration. Using a one-period forward binomial tree, find the price of this put option. (a) $3.97 (b) $4.38 (c) $4.70 (d) $4.97 (e) None of the above.

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to be 0.30 and its dividend yield is 0.03. The continuously-compounded, risk-free interest rate equals 0.06. Consider a $95-strike European put option on the above stock with three months to expiration. Using a one-period forward binomial tree, find the price of this put option. (a) $3.97 (b) $4.38 (c) $4.70 (d) $4.97 (e) None of the above.

15: Interest rates are 10% per annum continuously compounded. The price of the stock is currently $100 per share. In one year the price will be either $125 per share or $75 per share. Using a one period Binomial Tree Model as outlined in Section 75, find the value, now, of the call option with exercise price of 100. What is the hedge ratio? Now calculate the answers for exercise prices of 90 and 110.

15: Interest rates are 10% per annum continuously compounded. The price of the stock is currently $100 per share. In one year the price will be either $125 per share or $75 per share. Using a one period Binomial Tree Model as outlined in Section 75, find the value, now, of the call option with exercise price of 100. What is the hedge ratio? Now calculate the answers for exercise prices of 90 and 110.

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Most questions answered within 3 hours.

-

For the following reaction, 0.128 moles of

potassium hydrogen sulfateare mixed with

0.504 moles of potassium...

asked 2 hours ago -

1. What is the present value of $400, three years in the future

if the interest...

asked 3 hours ago -

The labor force minus the number of employed equals the number

of unemployed.

a. True

b....

asked 5 hours ago -

Determine the mass in units of grams [g] of 0.49 moles [mol]

of a new fictitious...

asked 5 hours ago -

A horizontal mass of M=5kg is on a spring and stretched to

x=0.5m when released from...

asked 7 hours ago -

26 of 50

"I have worked at the Arizona Humane Society for ten years, and

have...

asked 7 hours ago -

Compare and contrast zero based budgeting and incremental (or

base year) budgeting.

asked 7 hours ago -

4 pts 10. Which of the following hypothesis would be MOST

difficult to test experimentally? Group...

asked 7 hours ago -

A business owner makes 1,000 items a day. Each day he or she

contributes eight hours...

asked 7 hours ago -

A

circular loop in the plane of a paper lies inca0.65 T magnetic

field pointing into...

asked 7 hours ago -

A business owner is trying to decide whether to buy, rent, or

lease office space and...

asked 7 hours ago -

Thermal Storage Solar heating of a house is much more efficient

if there is a way...

asked 7 hours ago