The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year.

1)Using the binomial tree, compute the price at time 0 of a one-year European put option on 100 shares of stock with a strike price of $115 per share.

Homework Answers

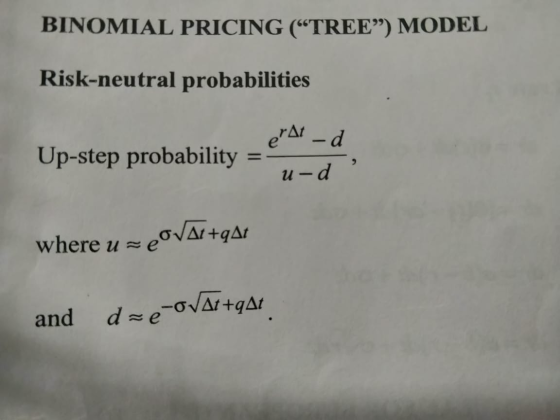

For a Binomial Model, The value of a Put option under the risk neutral probability measure is defined as the Discounted value of the expected payoff.

Or

Put option value Pt= e-rt * EQ[Payoff(XT)]

Here, u= Up step factor

d= Down step factor

q= up step probability(as defined above)

The following Put price has been computed on excel:

| sd | 20% | dt= | 0.33 | |||||||||

| Rf | 5% | u | 1.122401 | =EXP(B23*SQRT(E23)) | Share Price | |||||||

| Spot Price(St) | 115.00 | d | 0.890947 | =1/E24 | Payoff | |||||||

| Strike(K) | 115 | q | 0.543777 | =(EXP(B24*E23)-E25)/(E24-E25) | ||||||||

| t=0 | t=1 | t=2 | t=3 | |||||||||

| Formulas | ||||||||||||

| 162.608 | =F35*$E$24 | |||||||||||

| 0 | =MAX($B$26-G33,0) | |||||||||||

| 144.8751 | =E37*$E$24 | |||||||||||

| 0 | =EXP(-$B$24*$E$23)*(G34*$E$26+G38*(1-$E$26)) | |||||||||||

| 129.0761 | 129.0761 | =F39*$E$24 | ||||||||||

| 2.524719 | 0 | =MAX($B$26-G37,0) | ||||||||||

| 115.00 | 115 | =E41*$E$24 | ||||||||||

| Pt= | 7.091836 | 5.626959 | =EXP(-$B$24*$E$23)*(G38*$E$26+G42*(1-$E$26)) | |||||||||

| 102.4589 | 102.4589 | =F43*$E$24 | ||||||||||

| 12.79667 | 12.54107 | =MAX($B$26-G41,0) | ||||||||||

| 91.28551 | =E41*$E$25 | |||||||||||

| 21.81371 | =EXP(-$B$24*$E$23)*(G42*$E$26+G46*(1-$E$26)) | |||||||||||

| 81.33057 | =F43*$E$25 | |||||||||||

| 33.66943 | =MAX($B$26-G45,0) | |||||||||||

The price for put on 1 share is Pt= 7.091836.

Therefore price for Put on 100 shares is Pt=709.1836.

Add Answer to:

The spot price per share is $115 and the risk free rate is 5%

per annum...

. The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual...

. The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work. 1.Using the binomial tree, compute the price at time 0 of a one-year European call option...

The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work. How would you hedge a long position in the American put option at time 0?

The spot price per share is $115 and the risk free rate is 5% per annum...

The spot price per share is $115 and the risk free rate is 5% per annum on a continuously compounded basis. The annual volatility is 20% and the stock does not pay any dividend. All options have a one-year maturity. In answering the questions below use a binomial tree with three steps. Each step should be one-third of a year. Show your work. Compute u, d, as well as p for the standard binomial model.

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to be 0.30 and its dividend yield is 0.03. The continuously-compounded, risk-free interest rate equals 0.06. Consider a $95-strike European put option on the above stock with three months to expiration. Using a one-period forward binomial tree, find the price of this put option. (a) $3.97 (b) $4.38 (c) $4.70 (d) $4.97 (e) None of the above.

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to...

The current price of a continuous-dividend-paying stock is $100 per share. Its volatility is given to be 0.30 and its dividend yield is 0.03. The continuously-compounded, risk-free interest rate equals 0.06. Consider a $95-strike European put option on the above stock with three months to expiration. Using a one-period forward binomial tree, find the price of this put option. (a) $3.97 (b) $4.38 (c) $4.70 (d) $4.97 (e) None of the above.

Find the fair value of an European call option and an American put option using the...

Find the fair value of an European call option and an American put option using the incoherent and coherent binomial option tree if the underlying asset pays dividend of 4 PLN in one and half month. The initial stock price is 60 PLN, the strike price of 58 PLN is expiring at the end of the third month, the continuously compounded risk-free interest rate is 10% per annum, and the stock volatility is 20%.

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4%...

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

Consider a European put option on a currency. The exchange rate is $1.20 per unit of...

Consider a European put option on a currency. The exchange rate is $1.20 per unit of the foreign currency, the strike price is $1.25, the time to maturity is one year, the domestic risk-free rate is 0% per annum, and the foreign risk-free rate is 5% per annum. The volatility of the exchange rate is 0.25. What is the value of this put option according to a one-step binomial tree?

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

A stock index is currently 1 ,500. Its volatility is 18%. The risk-free rate is 4% per annum (continuously compounded) for all maturities and the dividend yield on the index is 2.5% Calculate values for u, d, and p when a 6-month time step is used. What is the value a 12-month American put option with a strike price of 1,480 given by a two-step binomial tree.

Most questions answered within 3 hours.

-

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 1 hour ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 2 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 3 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 4 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 5 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 5 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 5 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 5 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 5 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 5 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 5 hours ago -

Would CuCO3 aqueous salt combined with calcium chloride

form a solid precipitate? If so, what would...

asked 5 hours ago