On August 1, Terry issued a $1,600,000, semi-annual, 6 year, 4.5% bond. The market rate for similar bonds on that day was 5.0%. Terry uses the effective interest method to record the amortization or premiums and discounts. Terry’s management has decided to report net bonds on the balance sheet, instead of reporting the bond and its premium or discount separately. No entries have yet been made for the bond. Terry’s management would like to know the effect of the sale on the following ratios:

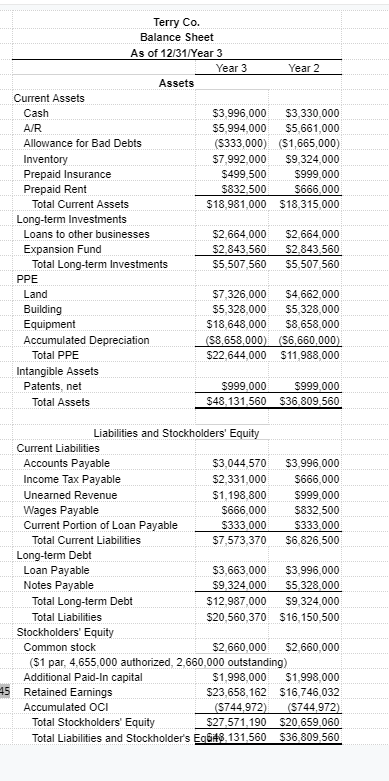

•Debt to Equity Ratio (Total Liabilities / Total Equity)

•Current Ratio

•ROA

1. Calculate each of the three (3) ratios before you make any adjustments

2. Make the appropriate journal entries, if any, to account for the new bond and any accrued interest (including any necessary changes to income tax expense)

3 Make any necessary changes to the financial statements

4. Calculate the three (3) ratios after you make any adjustments

5.What do you think investors’ reaction will be to management’s decision to issue a new bond? In other words, based on your changes to the financial statements and the change in the ratios, do you think investors will be happy with the decision to issue the new debt? Why or why not?

6.Terry’s CFO has been concerned about the issuance of this bond. The company really doesn’t need the additional cash at the moment, despite some vague plans to expand in the near future. The rest of the management team, on the other hand, felt that the additional cash would allow them to repurchase shares and pay a larger dividend for the period, both of which would help to calm investors’ fears after all of the changes that needed to be made to the financial statements this period. Provide two (2) arguments that the CFO could have used to try to talk his colleagues out of issuing the bond

Homework Answers

| 1 | Calculation of ratio | ||||

| a | Debt to equity | ||||

| 1 | Debt | 12987000 | |||

| 2 | Equity | 27571190 | |||

| Debt to equity(1/2) | 0.471035164 | ||||

| b | Current Ratio | ||||

| 1 | Current Asset | 18981000 | |||

| 2 | current Liablity | 7573370 | |||

| Current Ratio(1/2) | 2.50628188 | ||||

| c | ROA | ||||

| 1 | Net Income | 7112130 | |||

| 2 | Total Asset | 48131560 | |||

| ROA(1/2) | 0.147764377 | ||||

| 2 | Journal Entry for new bond | ||||

| Working | |||||

| Term | Cash Outflow | Discount rate | present value of bond | ||

| 1 | 36,000 | 0.98 | 0.97560976 | 35,122 | |

| 2 | 36,000 | 0.98 | 0.9518144 | 34,265 | |

| 3 | 36,000 | 0.98 | 0.92859941 | 33,430 | |

| 4 | 36,000 | 0.98 | 0.90595064 | 32,614 | |

| 5 | 36,000 | 0.98 | 0.88385429 | 31,819 | |

| 6 | 36,000 | 0.98 | 0.86229687 | 31,043 | |

| 7 | 36,000 | 0.98 | 0.84126524 | 30,286 | |

| 8 | 36,000 | 0.98 | 0.82074657 | 29,547 | |

| 9 | 36,000 | 0.98 | 0.80072836 | 28,826 | |

| 10 | 36,000 | 0.98 | 0.7811984 | 28,123 | |

| 11 | 36,000 | 0.98 | 0.76214478 | 27,437 | |

| 12 | 1,636,000 | 0.98 | 0.74355589 | 1,216,457 | |

| 1,558,969 | |||||

| Premium on the bond | |||||

| 1 | Issue Price | 1,600,000 | |||

| 2 | Market Price | 1,558,969 | |||

| 3 | Premium | 41,031 | |||

| Journal Entry | |||||

| Bank A/c | Dr | 1600000 | |||

| Premium on issue | Cr | 41031 | |||

| 4.5% bond payable | Cr | 1558969 | |||

| 3 | Financial Statements | ||||

| income statement | |||||

| Net Income | 7112130 | ||||

| Premium on issue | 41031 | ||||

| Corrected Net income | 7153161 | ||||

| Balance Sheet | |||||

| Total asset | 48131560 | ||||

| Add Cash | 1600000 | ||||

| Corrected total asset | 49731560 | ||||

| Total Liablities | 48131560 | ||||

| Add change in retained Earnings | 41031 | ||||

| Add 4.5% Bond payable | 1558969 | ||||

| Corrected total liablities | 49731560 | ||||

| 4 | Changed ratios | ||||

| a | Debt to equity | ||||

| 1 | Debt | 14545969 | |||

| 2 | Equity | 27530159 | |||

| Debt to equity(1/2) | 0.528364874 | ||||

| b | Current Ratio | ||||

| 1 | Current Asset | 18981000 | |||

| 2 | current Liablity | 7573370 | |||

| Current Ratio(1/2) | 2.50628188 | ||||

| c | ROA | ||||

| 1 | Net Income | 7153161 | |||

| 2 | Total Asset | 49731560 | |||

| ROA(1/2) | 0.143835444 | ||||

| 5 | Arguments | ||||

| a | The debt equity ratio has changed .47 to .52,which is not good | ||||

| b | The Company has enough on cash in hand to buy back shares as well as payout dividend | ||||

Add Answer to:

On August 1, Terry issued a $1,600,000, semi-annual, 6 year, 4.5% bond. The market rate for...

Using the money from their recent bond issue, Terry’s management has decided to declare an additional...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management has decided to declare an additional...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Information: Using the money from their recent bond issue, Terry’s management has decided to declare an...

Information: Using the money from their recent bond issue, Terry’s management has decided to declare an additional $562,500 dividend. The date of declaration is December 30, Year 3. The date of record will be January 15, Year 4, and the date of payment will be January 30, Year 4. As an additional signal to the market, Terry’s management repurchased 205,000 shares of Terry’s common stock on December 15, Year 3 for $8.00 a share. Terry’s management would like to know...

Information: Using the money from their recent bond issue, Terry’s management has decided to declare an...

Information:

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share. Tax rate is 25%...

Information:

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share. Tax rate is 25%...

Information: • On August 1, Terry issued a $1,600,000, semi-annual, 6 year, 4.5% bond. The market...

Information: • On August 1, Terry issued a $1,600,000, semi-annual, 6 year, 4.5% bond. The market rate for similar bonds on that day was 5.0%. Terry uses the effective interest method to record the amortization or premiums and discounts. Terry’s management has decided to report net bonds on the balance sheet, instead of reporting the bond and its premium or discount separately. No entries have yet been made for the bond. Terry’s management would like to know the effect of...

Terry has three main classifications of employees: management, designers, and production workers. In order to retain...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

****Only Need 6 & 7 answered **** Terry has three main classifications of employees: management, designers,...

****Only Need 6 & 7 answered ****

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little...

****Only Need 6 & 7 answered ****

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little...

Terry has three main classifications of employees: management, designers, and production workers. In order to retain...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management, designers, and production workers. In order to retain...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Information: Terry has three main classifications of employees: management, designers, and production workers. In order to...

Information:

Terry has three main classifications of employees: management,

designers, and production workers. In

order to retain their qualified design (or research) staff,

Terry has offered them a small defined benefit

pension if they remain with the company until their retirement.

Terry’s management team has been

provided with a 401(k) (despite numerous complaints from the

management team that they also

deserve a pension). Since the production team traditionally

turns over very quickly with little adverse

effect on the company, Terry...

Information:

Terry has three main classifications of employees: management,

designers, and production workers. In

order to retain their qualified design (or research) staff,

Terry has offered them a small defined benefit

pension if they remain with the company until their retirement.

Terry’s management team has been

provided with a 401(k) (despite numerous complaints from the

management team that they also

deserve a pension). Since the production team traditionally

turns over very quickly with little adverse

effect on the company, Terry...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share.

Terry’s management would like to know the...

Information:

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share. Tax rate is 25%...

Information:

Using the money from their recent bond issue, Terry’s management

has decided to declare an additional $562,500 dividend. The date of

declaration is December 30, Year 3. The date of record will be

January 15, Year 4, and the date of payment will be January 30,

Year 4.

As an additional signal to the market, Terry’s management

repurchased 205,000 shares of Terry’s common stock on December 15,

Year 3 for $8.00 a share. Tax rate is 25%...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

****Only Need 6 & 7 answered ****

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little...

****Only Need 6 & 7 answered ****

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Terry has three main classifications of employees: management,

designers, and production workers. In order to retain their

qualified design (or research) staff, Terry has offered them a

small defined benefit pension if they remain with the company until

their retirement. Terry’s management team has been provided with a

401(k) (despite numerous complaints from the management team that

they also deserve a pension). Since the production team

traditionally turns over very quickly with little adverse effect on

the company, Terry does...

Information:

Terry has three main classifications of employees: management,

designers, and production workers. In

order to retain their qualified design (or research) staff,

Terry has offered them a small defined benefit

pension if they remain with the company until their retirement.

Terry’s management team has been

provided with a 401(k) (despite numerous complaints from the

management team that they also

deserve a pension). Since the production team traditionally

turns over very quickly with little adverse

effect on the company, Terry...

Information:

Terry has three main classifications of employees: management,

designers, and production workers. In

order to retain their qualified design (or research) staff,

Terry has offered them a small defined benefit

pension if they remain with the company until their retirement.

Terry’s management team has been

provided with a 401(k) (despite numerous complaints from the

management team that they also

deserve a pension). Since the production team traditionally

turns over very quickly with little adverse

effect on the company, Terry...

Most questions answered within 3 hours.

-

A solid, uniform disk of radius 0.250 m and mass 53.7 kg rolls

down a ramp...

asked 1 hour ago -

Given the following table of high speed internet access vs.

annual home income:

Home Income

%...

asked 2 hours ago -

A baseball batter hits a 0.145kg baseball straight up into the

air. The baseball leaves the...

asked 2 hours ago -

An FM modulator is tested using

single-tone baseband signal with frequency of 50kHz and a sprectrum...

asked 3 hours ago -

Write the ionic equations for the first stage of salts

hydrolysis.

Anion, Cation?

Na2S

NiSO4

K2SO4...

asked 4 hours ago -

suppose there is a normally distributed population with a mean of

250 and a standard deviation...

asked 5 hours ago -

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 6 hours ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 6 hours ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 7 hours ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 7 hours ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 7 hours ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 7 hours ago