Cane company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively....

Cane company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 100,000 units of each product. Its unit costs for each product at this level of activity are given below:

Alpha Beta

Direct Materials $30 $12

Direct Labor 20 15

Variable manufacturing overhead 7 5

Traceable fixed manufacturing overhead 16 18

Variable selling expenses 12 8

Common fixed expenses 15 10

Total cost per unit $100 $68

The company considers its traceable fixed manufacturing overhead to be avoidable, whereas its common fixed expenses are deemed unavoidable and have been allocated to products based on sales dollars.

Required to Answer:

1. What is the total amount of traceable fixed manufacturing overhead for the Alpha product line and for the Beta product line?

2. What if the company's total amount of common fixed expenses?

3. Assume that Cane expects to produce and sell 80,000 Alphas during the current year. One of Cane's sales representatives has found a new customer that is willing to buy 10,000 additional Alphas for a price of $80 per unit. If Cane accepts the customer's offer, how much will its profits increase or decrease?

4. Assume that Cane expects to produce and sell 90,000 Betas during the current year. One of Cane's sales representatives has found a new customer that is willing to buy 5,000 additional Betas for a price of $39 per unit. If Cane accepts the customer's offer, how much will its profits increase or decrease?

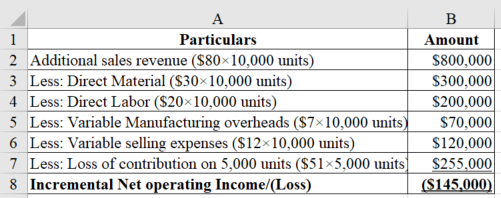

5. Assume that Cane expects to produce and sell 95,000 Alphas during the current year. One of Cane's sale representatives has found a new customer willing to buy 10,000 additional Alphas for a price of $80 per unit. If Cane accepts the customer's offer, it will decrease Alpha sales to regular customers by 5,000 units. Should Cane accept this special order?

6. Assume that Cane produces and sells 90,000 Betas per year. If Cane discontinues the Beta product line, how much will profits increase or decrease?

7. Assume that Cane produces and sells 40,000 Betas per year. If Cane discontinues the Beta product line, how much will profits increase or decrease?

8. Assume that Cane normally produces and sells 60,000 Betas and 80,000 Alphas per year. If Cane discontinues the Beta product line, its sales representatives could increase sales of Alpha by 15,000 units. If Cane discontinues the Beta product line, how much would profits increase or decrease?

9. Assume that Cane expects to produce and sell 80,000 Alphas during the current year. A supplier has offered to manufacture and deliver 80,000 Alphas to Cane for a price of $80 per unit. If Cane buys 80,000 units from the supplier instead of making those units, how much will those profits increase or decrease?

10. Assume that Cane expects to produce and sell 50,000 Alphas during the current year. A supplier has offered to manufacture and deliver 50,000 Alphas to Cane for a price of $80 per unit. If Cane buys 50,000 units from the supplier instead of making those units, how much will profits increaseor decrease?

Homework Answers

Cost: The concept of cost in management accounting refers to the amount paid or amount sacrificed to obtain something. The value of all the costs will have to be determined in monetary values. There are various types of costs in cost accounting. Therefore, identification of the costs is a significant task in management decision making.

Direct Material Cost: Direct material costs include cost of raw materials that are used in production or manufacture of a product. Direct material costs are easily identifiable cost of materials that have been used in the production process.

Direct Labor Cost: Cost of labor that is directly attributable to the process of manufacturing is termed as direct labor cost. It includes wages, taxes related to payment of wages and cost of other benefits for employees borne by the company.

Manufacturing overheads: Costs that are incurred in the factory, other than direct material and direct labor costs are termed as manufacturing overheads. Overhead are costs which are required to run a business but cannot be directly linked or attributed any specific product, activity or service. There are two types of overheads costs, Fixed overheads cost and variable overheads cost.

Variable expenses: The variable expenses are directly linked to the production process. The variable cost per unit remains constant. The total variable cost variates with the production level or activity level. These are considered direct costs which are relevant for the decision-making process. Direct material per unit, labor cost per unit etc. are the examples of variable expenses.

Fixed expenses: Fixed expenses are one-time expenses. Fixed expenses do not variate with the level of production activity. Fixed expenses incur even when there is no production. Fixed expenses remain constant throughout the production process, irrespective of the level of production activity. Fixed cost per unit variates with production level but total fixed cost remains constant. Depreciation, rent etc. are the examples of fixed expenses.

Incremental Cost: Incremental cost refers to the increase in total cost when there is an increase in production activity or any other activity base.

Incremental Profit: The increase in profit by selling extra units is termed as incremental profit.

Relevant Cost: The cost that is related to specific decision. A cost forms to be relevant cost when it is specifically incurred on manufacture or production of the respective product or else it is avoidable cost.

1.

Calculate the total amount of traceable fixed manufacturing overheads as follows:

Thus, the total amount of traceable fixed manufacturing overheads for Alpha & Beta are $1,600,000 and $1,800,000.

2.

Calculate the total amount of common fixed expenses as follows:

Thus, the total amount of common fixed manufacturing overhead for Alpha & Beta is $1,500,000 and $1,000,000 respectively.

3.

Calculate the increase or decrease in profit as follows:

Thus, total increase in profit will be $110,000.

Working note:

Calculate the amount of variable manufacturing expenses as follows:

4.

Calculate the increase or decrease in profits as follows:

Calculate the increase or decrease in profits using spreadsheet formulas as given below:

Thus, total decrease in profit if offer is accepted will be $5,000.

Working note:

Calculate the amount of variable cost per unit as follows:

Calculate the amount of variable manufacturing cost using spreadsheet formulas as given below:

5.

Calculate the net operating income for determining whether the special order should be accepted or not is as follows:

Calculate the net operating income using spreadsheet formulas as given below:

Working note:

Calculation of loss of contribution per unit is as follows:

6.

Calculate the increase/decrease in profit as follows:

7.

Calculate the increase/decrease in profit as follows:

8.

Calculate the total decrease in profit as follows:

9.

Calculate the profit when product is manufactured in-house as follows:

Calculate the amount of profit when product is purchased from supplier as follows:

Calculate the increase/(decrease) in profit when A is purchased from supplier as follows:

10.

Calculate the profit when product is manufactured in-house as follows:

Calculate the amount of profit when product is purchased from supplier as follows:

Calculate the increase/(decrease) in profit when A is purchased from supplier as follows:

The total amount of traceable fixed manufacturing overheads for Alpha & Beta are $1,600,000 and $1,800,000 respectively.

Add Answer to:

Cane company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $180 and $145, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $180 and $145, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 118,000 units of each product. Its unit costs for each product at this level of activity are given below: Alpha Beta Direct materials $ 36 $ 24 Direct labor 32 27 Variable manufacturing overhead 19 17 Traceable fixed manufacturing overhead 27 30...

Cane Company manufactures two products called Alpha and Beta that sell for $150 and $105, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $150 and $105, respectively. Each product uses only one type of raw material that costs $5 per pound. The company has the capacity to annually produce 107,000 units of each product. Its unit costs for each product at this level of activity are given below:AlphaBeta Direct materials$30$10 Direct labor2520 Variable manufacturing overhead1210 Traceable fixed manufacturing overhead2123 Variable selling expenses1713 Common fixed expenses2015 Total cost per unit$125$91The company considers its traceable fixed manufacturing overhead to be...

Cane Company manufactures two products called Alpha and Beta that sell for $240 and $162, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $240 and $162, respectively. Each product uses only one type of raw material that costs $5 per pound. The company has the capacity to annually produce 131,000 units of each product. Its unit costs for each product at this level of activity are given below: Alpha Beta Direct materials $ 35 $ 15 Direct labor 48 23 Variable manufacturing overhead 27 25 Traceable fixed manufacturing overhead 35 38...

Cane Company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 100,000 units of each product. Its average cost per unit for each product at this level of activity are given below: AlphaBeta Direct materials $30 $12 Direct labor 20 15 Variable manufacturing overhead 7 5 Traceable fixed manufacturing overhead 16 18 Variable selling expenses 12 8 Common fixed expenses 15 10 Total cost...

Cane Company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $120 and $80, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 100,000 units of each product. Its average cost per unit for each product at this level of activity are given below: Alpha Beta Direct materials $ 30 $ 12 Direct labor 20 15 Variable manufacturing overhead 7 5 Traceable fixed manufacturing overhead...

Cane Company manufactures two products called Alpha and Beta that sell for $ 150 and $ 105, respectively

Cane Company manufactures two products called Alpha and Beta that sell for $ 150 and $ 105, respectively. Each product uses only one type of raw material that costs $ 5 per pound. The company has the capacity to annually produce 107,000 units of each product. Its average cost per unit for each product at this level of activity are given below:The company considers its traceable fixed manufacturing overhead to be avoidable, whereas its common fixed expenses are unavoidable and...

Cane Company manufactures two products called Alpha and Beta that sell for $ 150 and $ 105, respectively. Each product uses only one type of raw material that costs $ 5 per pound. The company has the capacity to annually produce 107,000 units of each product. Its average cost per unit for each product at this level of activity are given below:The company considers its traceable fixed manufacturing overhead to be avoidable, whereas its common fixed expenses are unavoidable and...

Cane Company manufactures two products called Alpha and Betathat sell for $135 and $95, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $135 and $95, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 105,000 units of each product. Its unit costs for each product at this level of activity are given below:AlphaBeta Direct materials$30$18 Direct labor2316 Variable manufacturing overhead108 Traceable fixed manufacturing overhead1921 Variable selling expenses1511 Common fixed expenses1813 Total cost per unit$115$87The company considers its traceable fixed manufacturing overhead to be...

Cane Company manufactures two products called Alpha and Beta that sell for $205 and $164, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $205 and $164, respectively. Each product uses only one type of raw material that costs $8 per pound. The company has the capacity to annually produce 127,000 units of each product. Its unit costs for each product at this level of activity are given below: Alpha Beta Direct materials $ 40 $ 24 Direct labor 37 30 Variable manufacturing overhead 24 22 Traceable fixed manufacturing overhead 32 35...

Cane Company manufactures two products called alpha and beta that sell for $140 and $100, respectively....

Cane Company manufactures two products called alpha and beta that sell for $140 and $100, respectively. Each product uses only one type of raw material that costs $8 per pound. The company has the capacity to annually produce 106,000 units of each product. Its average cost per unit for each product at this level of activity are given below: Alpha/Beta Direct materials $32/16 Direct Labor $24/19 Variable Manufacturing Overhead $10/9 Traceable fixed manufacturing overhead $20/22 Variable selling expenses $16/12 common...

Cane Company manufactures two products called Alpha and Beta that sell for $170 and $130, respectively....

Cane Company manufactures two products called Alpha and Beta that sell for $170 and $130, respectively. Each product uses only one type of raw material that costs $6 per pound. The company has the capacity to annually produce 116,000 units of each product. Its average cost per unit for each product at this level of activity are given below: Alpha Beta Direct materials $ 30 $ 18 Direct labor 30 25 Variable manufacturing overhead 20 15 Traceable fixed manufacturing overhead...

Most questions answered within 3 hours.

-

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 8 minutes ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 32 minutes ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 1 hour ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 1 hour ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 2 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 3 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 4 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 4 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 4 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 5 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 5 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 5 hours ago