Consider an option strategy where the investor simultaneously buys one call with an exercise price of...

Consider an option strategy where the investor simultaneously buys one call with an exercise

price of $120 and sells one call with an exercise price of $110 both with the same expiration

date. Calculate the payoff of the strategy when spot price of the underlying is less than $110,

between $110 and $120, and greater than $120 at expiration. Draw a payoff diagram for this

strategy. What is the bet being made with this strategy?

Homework Answers

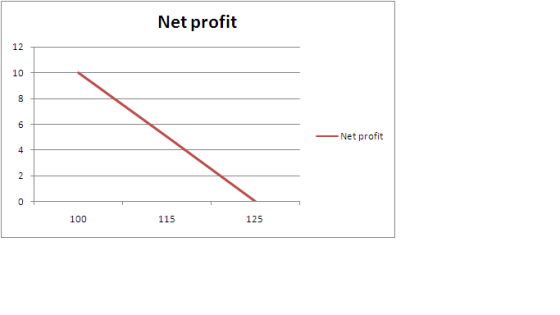

Table showing Payoff

| Price as on expiry |

Profit on call option bought ( Strike price 120$) Assuming premium paid to be 10$ |

Profit on call option Sold (Strike price 110$) Assuming premium received to be 20$ |

Net profit |

| 100 | -10 | 20 | 10 |

| 115 | -10 | 15 | 5 |

| 125 | -5 | 5 | 0 |

Call options gives the buyer right to buy the underlying share at specified price in future. This right is received by paying premium to the seller of call. Here it is assumed that call option with strike price of $110 is trading at 20$ and Call option with strike price 120$ is trading at 10$

Profit Diagram

by this strategy one is expecting that price of stock will remain below $120 by the expiry. Trader is bearish on the stock

Add Answer to:

Consider an option strategy where the investor simultaneously buys one call with an exercise price of...

Consider an option strategy where the investor simultaneously buys one call with an exercise price of...

Consider an option strategy where the investor simultaneously buys one call with an exercise price of $100, sells two calls with an exercise price of $110 and buys one call with an exercise price of $120 all with the same expiration date. Calculate the payoff of the strategy when spot price of the underlying is less than $100, between $100 and $110, between $110 and $120, and greater than $120 at expiration. Draw a payoff diagram for this strategy. What...

A long straddle is an option strategy in which the investor buys a call option and...

A long straddle is an option strategy in which the investor buys a call option and a put option with the same strike price and the same expiration date. If the strike is $40/share and the premiums for the call and the put are $4/share and $3/share respectively. Draw the profit loss diagram for the long straddle strategy. Repeat problem 1 for a short straddle (i.e. write a call and write a put).

To apply Bull Spread strategy, an investor buys for $3 a three-month call with a strike...

To apply Bull Spread strategy, an investor buys for $3 a three-month call with a strike price of $30 and sells for $1 a three-month call with a strike price of $35. The payoff from this bull spread strategy is $5 if the stock price is above $35 and zero if it is below $30. Please consider the different stock prices at expiration date to conduct a profit analysis and draw profit diagram.

Consider a European call option on €62,500 with an exercise price of $1.50/€. You pay an...

Consider a European call option on €62,500 with an exercise price of $1.50/€. You pay an option premium of $0.10/€ for the call option today. a. If the $-€ spot exchange rate is $1.62/€ on the contract expiration date, would you exercise the call option (buy € at the exercise price at expiration)? What would be the option payoff and profit? b. If the $-€ spot exchange rate is $1.45/€ on the contract expiration date, would you exercise the call...

An investor purchases a call option with an exercise price of $55 for $2.60. The same...

An investor purchases a call option with an exercise price of $55 for $2.60. The same investor sells a call on the same security with an exercise price of $60 for $1.40. What is the payoff of the investor's strategy?

1. Consider a call option selling for $ 4 in which the exercise price is $50....

1. Consider a call option selling for $ 4 in which the exercise price is $50. A) Determine the value at expiration and the profit for a buyer under the following outcomes: i. The price of the underlying at expiration is $55 ii. The price of the underlying at expiration is $51 iii. The price of the underlying at expiration is $48 B) Determine the value at expiration and the profit for a seller under the following outcomes: i. The...

An investor purchases a call option with an exercise price of $55 for $2.60. The same...

An investor purchases a call option with an exercise price of $55 for $2.60. The same investor sells a call on the same security with an exercise price of $60 for $1.40. Draw the payoff graph of the stock price.

30. An investor constructs a long straddle by buying an April $30 call for $4 and...

30. An investor constructs a long straddle by buying an April $30 call for $4 and buying an April put $30 for $3. If the price of the underlying shares is $27 at expiration, what is the profit on the position? a. -$4 b. -$2 c. $2 d. $3 31. Consider an option strategy where an investor buys one call option with an exercise price of $55 for $7, sells two call options with an exercise price of $60 for...

30. An investor constructs a long straddle by buying an April $30 call for $4 and buying an April put $30 for $3. If the price of the underlying shares is $27 at expiration, what is the profit on the position? a. -$4 b. -$2 c. $2 d. $3 31. Consider an option strategy where an investor buys one call option with an exercise price of $55 for $7, sells two call options with an exercise price of $60 for...

QUESTION 19 Kenny Silver, CFA, is estimating the price of a call option. The call has...

QUESTION 19 Kenny Silver, CFA, is estimating the price of a call option. The call has an exercise price of $100 and a remaining time to expiration of 273 days. The spot price of the underlying stock is $93.25 and a put of the same underlying stock, exercise price and remaining time to expiration is currently priced at $6.50. Assuming a risk-free rate of 8% and a 365-day period, the call option’s arbitrage-free price is a. $5.34 b. $7.66 c....

28 You are considering a strategy that buys a call and shorts a put on the...

28 You are considering a strategy that buys a call and shorts a put on the same stock with the same strike price and expiration date. To replicate the payoff of this strategy, you could also 1) Short the call and purchase the underlying stock at the strike price. 2) Short the underlying stock and lend PV(strike price). 3) Buy the underlying stock and borrow PV(strike price). 4) Long the put and short the underlying stock at the strike price....

28 You are considering a strategy that buys a call and shorts a put on the same stock with the same strike price and expiration date. To replicate the payoff of this strategy, you could also 1) Short the call and purchase the underlying stock at the strike price. 2) Short the underlying stock and lend PV(strike price). 3) Buy the underlying stock and borrow PV(strike price). 4) Long the put and short the underlying stock at the strike price....

30. An investor constructs a long straddle by buying an April $30 call for $4 and buying an April put $30 for $3. If the price of the underlying shares is $27 at expiration, what is the profit on the position? a. -$4 b. -$2 c. $2 d. $3 31. Consider an option strategy where an investor buys one call option with an exercise price of $55 for $7, sells two call options with an exercise price of $60 for...

30. An investor constructs a long straddle by buying an April $30 call for $4 and buying an April put $30 for $3. If the price of the underlying shares is $27 at expiration, what is the profit on the position? a. -$4 b. -$2 c. $2 d. $3 31. Consider an option strategy where an investor buys one call option with an exercise price of $55 for $7, sells two call options with an exercise price of $60 for...

28 You are considering a strategy that buys a call and shorts a put on the same stock with the same strike price and expiration date. To replicate the payoff of this strategy, you could also 1) Short the call and purchase the underlying stock at the strike price. 2) Short the underlying stock and lend PV(strike price). 3) Buy the underlying stock and borrow PV(strike price). 4) Long the put and short the underlying stock at the strike price....

28 You are considering a strategy that buys a call and shorts a put on the same stock with the same strike price and expiration date. To replicate the payoff of this strategy, you could also 1) Short the call and purchase the underlying stock at the strike price. 2) Short the underlying stock and lend PV(strike price). 3) Buy the underlying stock and borrow PV(strike price). 4) Long the put and short the underlying stock at the strike price....

Most questions answered within 3 hours.

-

What mechanisms Drive speciation??

(I.e. what was Dawins theory on the orgin of species, and how...

asked 19 minutes ago -

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 1 hour ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 2 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 3 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 5 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 5 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 5 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 5 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 5 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 5 hours ago -

The cliché we use quite a lot in finance is: there is a need to

maximize...

asked 5 hours ago -

In class we discussed the addition of HCl to alpha pinene. Would

you expect one or...

asked 5 hours ago