Homework Answers

| Direct materials and direct labor variances: | |||||||

| Direct material quantity variance=Standard rate of material*(Actual quantity consumed-Standard quantity) | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Standard rate of material=$ 0.60 per pound | |||||||

| Standard quantity=Actual units produced*standard quantity required per pound | |||||||

| Standard quantity required per pound=Budgeted materials in pounds/Budgeted units to be produced | |||||||

| Budgeted materials in pounds=Budgeted direct materials/Standard rate of material=18000/0.60=30000 pounds | |||||||

| Standard quantity required per pound=30000/12000=2.5 pounds per unit | |||||||

| Standard quantity=10600*2.5=26500 pound | |||||||

| Actual quantity consumed=Actual direct material cost/Actual rate of material | |||||||

| There were no direct material price variance for June. | |||||||

| Hence, Standard rate of material=Actual rate of material=$0.60 per pound | |||||||

| Actual quantity consumed=16400/0.60=27333 pound | |||||||

| Direct material quantity variance=0.60*(27333-26500)=4999.8=500=$ 500 Unfavorable | |||||||

| Direct labor time variance=Standard rate of labor*(Actual hours worked-Standard hours) | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Standard rate of labor=$14 per hour | |||||||

| Standard hours=Actual units produced*Standard hour per unit | |||||||

| Standard hours per unit=standard hours required/Budgeted units to be produced | |||||||

| Standard hours required=Budgeted direct labor cost/Standard rate of labor=11760/14=840 hours | |||||||

| Standard hours per unit=840/12000=0.07 hours | |||||||

| Standard hours=10600*0.07=742 hours | |||||||

| Actual hours worked=Actual direct labor cost/Actual rate of labor | |||||||

| There were no direct labor rate variance for June. | |||||||

| Hence, Standard rate of labor=Actual rate of labor=$14 per hour | |||||||

| Actual hours worked=10700/14=764 hours | |||||||

| Direct labor time variance=14*(764-840)=-1064=$ 1064 Favorable | |||||||

| Flexible overhead budget: | |||||||

| Variable overhead cost per unit=budgeted cost/Budgeted hours of production | |||||||

|

Budgeted cost |

Budgeted hours of production |

Variable overhead cost per unit |

|||||

| a | b | a/b | |||||

| Indirect labor | 131600 | 14000 | 9.4 | ||||

| Power and light | 5740 | 14000 | 0.41 | ||||

| Indirect materials | 36400 | 14000 | 2.6 | ||||

| Fixed overhead cost will remain same at all levels of production | |||||||

| Factory overhead cost budget-Press department | |||||||

| Direct labor hours | 12000 | 14000 | 16000 | ||||

| $ | $ | $ | |||||

| Variable overhead cost: | |||||||

| Indirect labor | 112800 | 131600 | 150400 | ||||

| (12000*9.4) | (14000*9.4) | (16000*9.4) | |||||

| Power and light | 4920 | 5740 | 6560 | ||||

| (12000*0.41) | (14000*0.41) | (16000*0.41) | |||||

| Indirect materials | 31200 | 36400 | 41600 | ||||

| (12000*2.6) | (14000*2.6) | (16000*2.6) | |||||

| Total variable factory overhead | a | 148920 | 173740 | 198560 | |||

| Fixed factory overhead cost: | |||||||

| Supervisory salaries | 60810 | 60810 | 60810 | ||||

| Depreciation of plant and equipment | 38220 | 38220 | 38220 | ||||

| Insurance and property taxes | 24320 | 24320 | 24320 | ||||

| Total fixed factory overhead | b | 123350 | 123350 | 123350 | |||

| Total factory overhead cost | a+b | 272270 | 297090 | 321910 | |||

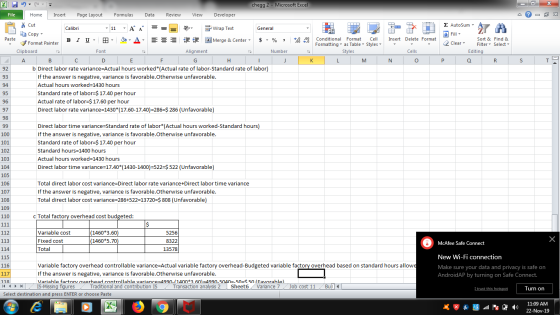

| Factory overhead cost variances: | |||||||

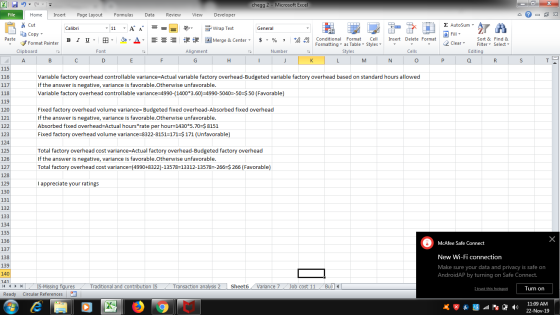

| Variable factory overhead controllable variance=Actual variable factory overhead cost incurred-Budgeted variable factory overhead for 4000 hours | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Budgeted variable factory overhead for 5000 hours=(Budgeted hours)*(standard factory overhead rate per hour-Standard fixed factory overhead rate per hour)=5000*(26-5.25)=$ 103750 | |||||||

| Variable factory overhead controllable variance=100600-103750=-3150=$ 3150 favorable | |||||||

| Fixed factory overhead volume variance=Productive capacity not used*Standard fixed factory overhead rate | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Productive capacity not used=Productive capacity at 100%-Budgeted level of production=8000-5000=3000 hours | |||||||

| Fixed factory overhead volume variance=3000*5.25=15750=$ 15750 Unfavorable | |||||||

| Total factory overhead cost variance=Variable factory overhead controllable variance+Fixed factory overhead volume variance | |||||||

| Total factory overhead cost variance=-3150+15750=12600=$ 12600 Unfavorable | |||||||

| Direct materials,Direct labor and factory overhead cost variance analysis: | |||||||

| a | Direct materials price variance=Actual quantity of material used*(Actual rate of material-Standard rate of material) | ||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Actual material used=7200 lbs. | |||||||

| Standard rate of material=$ 4.70 per pound | |||||||

| Actual rate of material=$ 4.50 per pound | |||||||

| Direct materials price variance=7200*(4.50-4.70)=-1440=$ 1440 (Favorable) | |||||||

| Direct Materials quantity variance=Standard rate of material*(Actual quantity consumed-Standard quantity) | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Standard rate of material=$ 4.70 per pound | |||||||

| Standard quantity=7300 lbs. | |||||||

| Actual material used=7200 lbs. | |||||||

| Material quantity variance=4.70*(7200-7300)=-470=$ 470 (Favorable) | |||||||

| Total direct materials cost variance=Direct materials price variance+Direct materials quantity variance | |||||||

| If the answer is negative, variance is favorable.Otherwise unfavorable. | |||||||

| Total material cost variance=-1440+-470=1910=$ 1910 (Favorable) | |||||||

Add Answer to:

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 10,080 Total $35,280 The standard materials price is $0.60 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,500 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 10,080 Total $35,280 The standard materials price is $0.60 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,500 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 25,200 Total $50,400 The standard materials price is $0.70 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,800 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 25,200 Total $50,400 The standard materials price is $0.70 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,800 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 23,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 23,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $24,150 Direct labor 10,120 Total $34,270 The standard materials price is $0.70 per pound. The standard direct labor rate is $11.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,900 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 21,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 21,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: $36,750 Direct materials 17,640 Direct labor Total $54,390 The standard materials price is $0.70 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $34,400 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 21,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: $36,750 Direct materials 17,640 Direct labor Total $54,390 The standard materials price is $0.70 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $34,400 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 13,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 13,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $19,500 Direct labor 11,830 Total $31,330 The standard materials price is $0.50 per pound. The standard direct labor rate is $13.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: $18,200 Actual direct materials Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 13,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $19,500 Direct labor 11,830 Total $31,330 The standard materials price is $0.50 per pound. The standard direct labor rate is $13.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: $18,200 Actual direct materials Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 26,000...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 26,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $36,400 Direct labor 15,600 Total $52,000 The standard materials price is $0.40 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $32,600 Actual...

3 Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted...

3 Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 14,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $14,000 Direct labor 13,720 Total $27,720 The standard materials price is $0.50 per pound. The standard direct labor rate is $14.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $13,300...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action fig...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $42,000 15,840 Direct labor Total $57,840 The standard materials price is $0.50 per pound. The standard direct labor rate is $11.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials Actual direct...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $42,000 15,840 Direct labor Total $57,840 The standard materials price is $0.50 per pound. The standard direct labor rate is $11.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials Actual direct...

Factory Overhead Cost Variances The following data relate to factory overhead cost for the production of...

Factory Overhead Cost Variances The following data relate to factory overhead cost for the production of 6,000 computers: Actual: Variable factory overhead $170,200 Fixed factory overhead 57,500 Standard: 6,000 hrs. at $35 210,000 If productive capacity of 100% was 10,000 hours and the total factory overhead cost budgeted at the level of 6,000 standard hours was $233,000, determine the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance. The fixed factory overhead rate...

Factory Overhead Cost Variances The following data relate to factory overhead cost for the production of 6,000 computers: Actual: Variable factory overhead $170,200 Fixed factory overhead 57,500 Standard: 6,000 hrs. at $35 210,000 If productive capacity of 100% was 10,000 hours and the total factory overhead cost budgeted at the level of 6,000 standard hours was $233,000, determine the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance. The fixed factory overhead rate...

At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured...

At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $18,000 Direct labor 14,400 Total $32,400 The standard materials price is $0.50 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $16,700 Actual direct labor 13,300 Total $30,000 There...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 10,080 Total $35,280 The standard materials price is $0.60 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,500 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 12,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 10,080 Total $35,280 The standard materials price is $0.60 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,500 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 25,200 Total $50,400 The standard materials price is $0.70 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,800 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $25,200 Direct labor 25,200 Total $50,400 The standard materials price is $0.70 per pound. The standard direct labor rate is $15.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $22,800 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 21,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: $36,750 Direct materials 17,640 Direct labor Total $54,390 The standard materials price is $0.70 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $34,400 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 21,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: $36,750 Direct materials 17,640 Direct labor Total $54,390 The standard materials price is $0.70 per pound. The standard direct labor rate is $12.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials $34,400 Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 13,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $19,500 Direct labor 11,830 Total $31,330 The standard materials price is $0.50 per pound. The standard direct labor rate is $13.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: $18,200 Actual direct materials Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 13,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $19,500 Direct labor 11,830 Total $31,330 The standard materials price is $0.50 per pound. The standard direct labor rate is $13.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: $18,200 Actual direct materials Actual...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $42,000 15,840 Direct labor Total $57,840 The standard materials price is $0.50 per pound. The standard direct labor rate is $11.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials Actual direct...

Direct Materials and Direct Labor Variances At the beginning of June, Kimber Toy Company budgeted 24,000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows: Direct materials $42,000 15,840 Direct labor Total $57,840 The standard materials price is $0.50 per pound. The standard direct labor rate is $11.00 per hour. At the end of June, the actual direct materials and direct labor costs were as follows: Actual direct materials Actual direct...

Factory Overhead Cost Variances The following data relate to factory overhead cost for the production of 6,000 computers: Actual: Variable factory overhead $170,200 Fixed factory overhead 57,500 Standard: 6,000 hrs. at $35 210,000 If productive capacity of 100% was 10,000 hours and the total factory overhead cost budgeted at the level of 6,000 standard hours was $233,000, determine the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance. The fixed factory overhead rate...

Factory Overhead Cost Variances The following data relate to factory overhead cost for the production of 6,000 computers: Actual: Variable factory overhead $170,200 Fixed factory overhead 57,500 Standard: 6,000 hrs. at $35 210,000 If productive capacity of 100% was 10,000 hours and the total factory overhead cost budgeted at the level of 6,000 standard hours was $233,000, determine the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance. The fixed factory overhead rate...

Most questions answered within 3 hours.

-

Write the ionic equations for the first stage of salts

hydrolysis.

Anion, Cation?

Na2S

NiSO4

K2SO4...

asked 20 minutes ago -

suppose there is a normally distributed population with a mean of

250 and a standard deviation...

asked 1 hour ago -

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 2 hours ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 2 hours ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 3 hours ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 3 hours ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 3 hours ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 3 hours ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 3 hours ago -

A 1.3 eV electron has a 10-4 probability of tunneling

through a 2.4 eV potential barrier....

asked 4 hours ago -

What is the one ingredient that is common to being successful

with all stakeholders?

profit

trust...

asked 4 hours ago -

Write an assembly language 32 bit program that reads in lines of

text by a .txt...

asked 4 hours ago