As of July 1, 2018, the City of Saratoga Springs decided to purchase a privately operated...

As of July 1, 2018, the City of Saratoga Springs

decided to purchase a privately operated swimming pool and to

create a Swimming Pool (Enterprise) Fund. During the year, the

following transactions occurred:

(a) A permanent contribution of $600,000 was received from the

General Fund.

(b) Revenue Bonds were sold at par in the amount of

$1,200,000.

(c) Purchased for cash several items, the cost breakdown was: land,

$300,000; building, $400,000, land improvement, $400,000;

equipment, $200,000; supplies, $150,000.

(d) Charges for services amounted to $600,000, all received in

cash.

(e) Cash expenses included: salaries, $200,000; utilities,

$100,000; interest (paid on 6/30/09), $72,000.

(f) Supplies were consumed in the amount of $120,000.

(g) Depreciation was recorded for: building, $20,000, land

improvement, $20,000; equipment, $20,000.

(h) The books were closed. Close all accounts to Net Assets.

Required:

1. Record the above transactions in general journal form (on the

books of the swimming pool fund).

2. Prepare, in good form, a Statement of Revenues, Expenses, and

Changes in Fund Net Assets for the City of Saratoga Springs

Swimming Pool Fund for the Year Ended June 30, 2019.

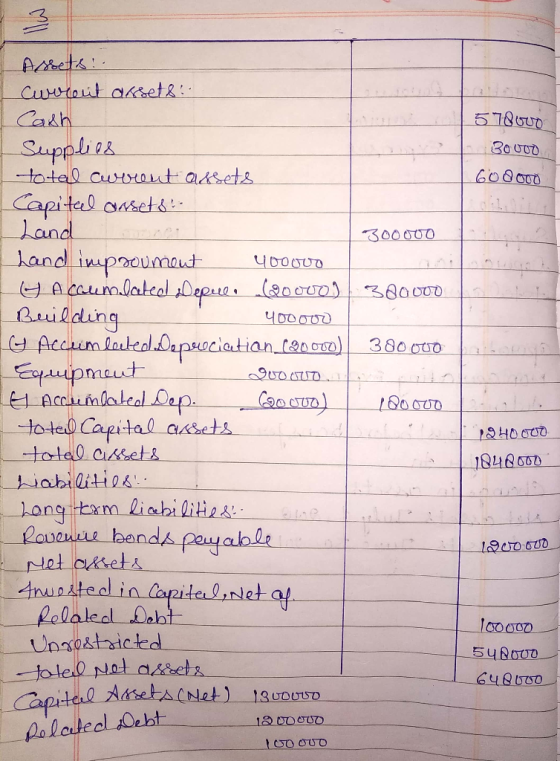

3. Prepare, in good form, a Statement of Fund Net Assets for the

City of Saratoga Springs Swimming Pool Fund as of June 30,

2019.

4. Prepare, in good form, a Statement of Cash Flows for the City of

Saratoga Springs Swimming Pool Fund for the Year Ended June 30,

2019. Assume all of the revenue bonds payable are for

capital-related acquisitions and that the transfer was to establish

working capital (i.e. a non-capital-related purpose).

Homework Answers

So here is the answer of that question ,hope it will help you in your work , for any further queries just comment below ,will be right back to you ..

Add Answer to:

As of July 1, 2018, the City of Saratoga Springs

decided to purchase a privately operated...

. As of July 1, 2018, the City of Saratoga Springs decided to purchase a privately...

. As of July 1, 2018, the City of Saratoga Springs decided to purchase a privately operated swimming pool and to construct a Swimming Pool (Enterprise) Fund. During the year, the following transactions occurred: (a) A permanent contribution of $600,000 was received from the General Fund. (b) Revenue Bonds were sold at par in the amount of $1,200,000. (c) Purchased for cash several items, the cost breakdown was: land, $300,000; building, $400,000, land improvement, $400,000; equipment, $200,000; supplies, $150,000. (d)...

Use the following to answer the next six questions: During the fiscal year ended December 31,...

Use the following to answer the next six questions: During the fiscal year ended December 31, 2017. the City of Johnstown issued 6% genera obligation serial bonds in the amount of $2.000.000 at 102 ($2.040,000) and used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was transferred to a debt service fund. The $20.000 left in the capital projects fund at the end of the project was later transferred to the debt service fund. The bonds...

Use the following to answer the next six questions: During the fiscal year ended December 31, 2017. the City of Johnstown issued 6% genera obligation serial bonds in the amount of $2.000.000 at 102 ($2.040,000) and used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was transferred to a debt service fund. The $20.000 left in the capital projects fund at the end of the project was later transferred to the debt service fund. The bonds...

The following information is available for the preparation of the government-wide financial statements of the City...

The following information is available for the preparation of the government-wide financial statements of the City of Sunbury as of June 30, 2017: Accounts payable, business-type activities $340,000 Accounts payable, governmental activities 610,000 Capital assets, net, business-type activities 10,400,000 Capital assets, net, governmental activities 10,800,000 Cash and cash equivalents, business-type activities 1,700,000 Cash and cash equivalents, governmental activities 1,800,000 Inventories, business-type activities 600,000 Net assets, restricted for debt service, business-type activities 640,000 Net assets, restricted for debt service, governmental activities...

The City of Milltown maintains its books so as to prepare fund accounting statements and records...

The City of Milltown maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets as of the beginning of the year, which had not been recorded, were as follows: Land $ 7,820,000 Buildings 32,355,000 Improvements Other Than Buildings 14,690,000 Equipment 11,554,000 Accumulated Depreciation, Capital Assets 24,300,000 During...

The following information is available for the preparation of the government-wide financial statements for the City...

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2017 Cash and cash equivalents, governmental activities $ 380,000 Cash and cash equivalents, business-type activities 800,000 Receivables, governmental activities 450.000 Receivables, business-type activities 1.330.000 Inventories, business-type activities 520,000 Capital assets, net, governmental activities 13,500,000 Capital assets, net, business-type activities 7.100.000 Accounts payable, governmental activities 650.000 Accounts payable, business-type activities 559,000 General obligation bonds, governmental activities 7,800,000 Revenue...

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2017 Cash and cash equivalents, governmental activities $ 380,000 Cash and cash equivalents, business-type activities 800,000 Receivables, governmental activities 450.000 Receivables, business-type activities 1.330.000 Inventories, business-type activities 520,000 Capital assets, net, governmental activities 13,500,000 Capital assets, net, business-type activities 7.100.000 Accounts payable, governmental activities 650.000 Accounts payable, business-type activities 559,000 General obligation bonds, governmental activities 7,800,000 Revenue...

Question 7 Banjo Ltd acquired 100% of Wellington Ltd on 1 July 2018. The balance sheet of Wellington Ltd on that date wa...

Question 7 Banjo Ltd acquired 100% of Wellington Ltd on 1 July 2018. The balance sheet of Wellington Ltd on that date was as follows: Balance sheet at 1 July 2018 NZ$ NZ$ Machinery at cost 560,000 Share capital 400,000 Investment property 400,000 General reserve 200,000 Receivables 100,000 Retained earnings 600,000 Cash 140,000 1,200,000 1,200,000 The balance sheet of Wellington Ltd as at 30 June 2019 is as follows: Balance sheet as at 30 June 2019 NZ$ NZ$ Machinery —...

The City of Williamsport maintains its books in order to prepare fund accounting statements and prepares...

The City of Williamsport maintains its books in order to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide financial statements. General fixed assets, as of the beginning of the year, which had not been recorded, were as follows: Land $45,500,000 Buildings 540,000,000 Improvements other than buildings 107,500,000 Equipment 175,000,000 Accumulated depreciation: capital assets 175,300,000 During the year, expenditures for capital outlays amounted to $12,350,000. Of that amount, $8,100,000 was for buildings; $1,500,000 was for improvements...

The Following is the June 30, 2019, statement of net position for the City of Bay...

The Following is the June 30, 2019, statement of net position for the City of Bay Lake Water Utility Fund. CITY OF BAY LAKE Water Utility Fund Statement of Fund Net Position June 30, 2019 Assets Current assets: Cash and investments $ 1,774,824 Accounts receivable (net of $13,365 provision for uncollectible accounts) 306,824 Accrued utility revenue 499,600 Due from General Fund 29,288 Interest receivable 81,936 Total current assets 2,692,472 Restricted assets: Cash 9,192 Capital assets: Land $ 1,780,753 Buildings (net...

The following information is available for the preparation of the government-wide financial statements for the City...

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2020: Cash and cash equivalents, governmental activities $ 540,000 Cash and cash equivalents, business-type activities 1,136,000 Receivables, governmental activities 642,000 Receivables, business-type activities 1,893,000 Inventories, business-type activities 744,000 Capital assets, net, governmental activities 19,311,000 Capital assets, net, business-type activities 10,156,000 Accounts payable, governmental activities 925,000 Accounts payable, business-type activities 799,000 General obligation bonds, governmental activities 11,147,000 Revenue...

The following information is extracted from the City of Lucas’ government-wide statement of net position at...

The following information is extracted from the City of Lucas’ government-wide statement of net position at December 31, 2019: Capital assets $2,000,000 Accumulated depreciation, capital assets $1,600,000 Annual depreciation rate on capital assets 10% Bonds payable -0- The following information is extracted from the city's governmental funds statement of revenues, expenditures, and changes in fund balances for the year ended December 31, 2020. Expenditures—capital outlay (General Fund) $40,000 Expenditures—capital outlay (Capital Projects Fund) ...

Use the following to answer the next six questions: During the fiscal year ended December 31, 2017. the City of Johnstown issued 6% genera obligation serial bonds in the amount of $2.000.000 at 102 ($2.040,000) and used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was transferred to a debt service fund. The $20.000 left in the capital projects fund at the end of the project was later transferred to the debt service fund. The bonds...

Use the following to answer the next six questions: During the fiscal year ended December 31, 2017. the City of Johnstown issued 6% genera obligation serial bonds in the amount of $2.000.000 at 102 ($2.040,000) and used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was transferred to a debt service fund. The $20.000 left in the capital projects fund at the end of the project was later transferred to the debt service fund. The bonds...

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2017 Cash and cash equivalents, governmental activities $ 380,000 Cash and cash equivalents, business-type activities 800,000 Receivables, governmental activities 450.000 Receivables, business-type activities 1.330.000 Inventories, business-type activities 520,000 Capital assets, net, governmental activities 13,500,000 Capital assets, net, business-type activities 7.100.000 Accounts payable, governmental activities 650.000 Accounts payable, business-type activities 559,000 General obligation bonds, governmental activities 7,800,000 Revenue...

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2017 Cash and cash equivalents, governmental activities $ 380,000 Cash and cash equivalents, business-type activities 800,000 Receivables, governmental activities 450.000 Receivables, business-type activities 1.330.000 Inventories, business-type activities 520,000 Capital assets, net, governmental activities 13,500,000 Capital assets, net, business-type activities 7.100.000 Accounts payable, governmental activities 650.000 Accounts payable, business-type activities 559,000 General obligation bonds, governmental activities 7,800,000 Revenue...

Most questions answered within 3 hours.

-

The pH of a sample of water from a river is 5.0. A

sample of effluent from...

asked 37 minutes ago -

At the beginning of the period, the Fabricating Department

budgeted direct labor of $136,500 and equipment...

asked 1 hour ago -

Please answer all

____ 28. Rent control is usually

justified on the grounds that it protects...

asked 1 hour ago -

PARTS A-D HAVE BEEN ANSWERED. WAS TOLD TO REPOST. ONLY ANSWER

PARTS E and F.

A...

asked 1 hour ago -

2) You are given the task of finding a representation for a

circle in a drawing...

asked 2 hours ago -

STUDY QUESTION: Does use of diet drug fen-phen

(fenfluramine-phentermine) cause valvular heart disease?

HINT: Valvular heart...

asked 2 hours ago -

1. An object weighing 40 N rests on a surface. The coefficient

of friction is 0.35....

asked 3 hours ago -

Investor company owns 35% of investee company voting stock and

accounts for the investment under the...

asked 4 hours ago -

The number of major faults on a randomly chosen 1 km stretch of

highway has a...

asked 5 hours ago -

Consider the competitive environment of Starbuck's, Progressive

Insurance, a manufacturing firm with low turnover, or a...

asked 5 hours ago -

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 7 hours ago -

A business executive has the option to invest money in two

plans: Plan A guarantees that...

asked 10 hours ago