-

Prepare entry S to eliminate stockholders' equity accounts of subsidiary.

-

2

Prepare entry A to recognize allocations determined above in connection with acquisition-date fair values.

-

3

Prepare entry I to eliminate intra-entity dividend declarations recorded by parent as income.

-

4

Prepare entry E to recognize 2017 amortization expense.

-

5

Prepare entry *C to convert parent company figures to equity method by recognizing subsidiary's increase in book value for prior year [$117,500 net income less $15,000 dividend declaration] and excess amortizations for that period [$11,710].

-

6

Prepare entry S to eliminate beginning of year stockholders' equity accounts of subsidiary. The retained earnings balance has been adjusted for 2017 net income and dividends.

-

7

Prepare entry A to recognize allocations relating to investment—balances shown here are as of the beginning of the current year [original allocation less excess amortizations for the prior period].

-

8

Prepare entry I to eliminate intra-entity dividend declarations recorded by parent as income.

-

9

Prepare entry E to recognize 2018 amortization expense.

Homework Answers

| Answer: (Two years of consolidation entries. Parent uses equity method.) | |||

| Fair Value Allocation and Annual Amortization: | |||

| Acquisition fair value (consideration transferred) | $816,280 | ||

| Book value (assets minus liabilities or total stockholders'equity) | ($709,650) | ||

| Excess fair value over bookvalue | $106,630 | ||

|

Excess fair value assigned to specific accounts based on individual fair values |

Life | Annual Excess Amortizations | |

| Long Term Liabilities | $29,280 | 4 | $7,320 |

| Equipment | $21,950 | 5 | $4,390 |

| Total assigned to specific accounts | $51,230 | ||

| Goodwill | $55,400 | Indefinite | $0 |

| Total | $106,630 | $11,710 | |

| Consolidation Entries as of December 31, 2017 | |||

| Debit | Credit | ||

| Entry S | |||

| Common Stock at Abernethy | $250,000 | ||

| Additional Paid in Capital | $50,000 | ||

| Retained Earnings as on 01/01/2017 | $409,650 | ||

| To Investment in Abernethy | $709,650 | ||

| (To eliminate stockholders' equity accounts of subsidiary) | |||

| Entry A | |||

| Long Term Liabilities | $29,280 | ||

| Equipment | $21,950 | ||

| Goodwill | $55,400 | ||

| To Investment in Abernethy | $106,630 | ||

| (To recognize allocations attributed to fair value of specific accounts at acquisition date with residual fair value recognized as goodwill). | |||

| Entry I | |||

| Equity in Subsidiary Earnings | $105,790 | ||

| To Investment in Abernethy | $105,790 | ||

| (To eliminate $117,500 income accrual for 2017 less $11,710 amortization recorded by parent using equity method) | |||

| Investment in Abernethy | $15,000 | ||

| To DividendsPaid | $15,000 | ||

| (To eliminate inter-company dividend transfers) | |||

| Entry E | |||

| Depreciation expense | $4,390 | ||

| Interest Expense | $7,320 | ||

| To Equipment | $4,390 | ||

| To Long Term Liabilities | $7,320 | ||

| (To record current year amortization expense) | |||

| Consolidation Entries as of December 31, 2018 | |||

| Entry S | |||

| Common Stock at Abernethy | $250,000 | ||

| Additional Paid in Capital | $50,000 | ||

| Retained Earnings as on 1/1/18 | $512,150 | ||

| To Investment in Abernethy | $812,150 | ||

| (To eliminate beginning stockholders' equity of subsidiary and the Retained Earnings account has been adjusted for 2017 income and dividends.) | |||

| Entry *C is not required because the equity method has been applied. | |||

| Entry A | |||

| Long Term Liabilities | $21,960 | ||

| Equipment | $17,560 | ||

| Goodwill | $55,400 | ||

| To Investment in Abernethy | $94,920 | ||

| (To recognize allocations relating to investment and balances shownhere are as of beginning of current year [original allocation less excess amortizations for the prior period]) | |||

| Entry I | |||

| Equity in Subsidiary Earnings | $159,540 | ||

| To Investment in Abernethy | $159,540 | ||

| (To eliminate $171,250 income accrual less $ 11,710 amortization recorded by parent during 2018 using equity method) | |||

| Entry D | |||

| Investment in Abernethy | $55,000 | ||

| To Dividends Paid | $55,000 | ||

| (To eliminate intercompany dividend transfers) | |||

| Entry E | |||

| Depreciation expense | $4,390 | ||

| Interest Expense | $7,320 | ||

| To Equipment | $4,390 | ||

| To Long Term Liabilities | $7,320 | ||

| (To record current year amortization expense) | |||

Add Answer to:

Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2

Prepare entry A to recognize...

Questions: 1. Prepare entry S to eliminate stockholders' equity accounts of subsidiary. 2. Prepare entry A...

Questions:

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize allocations attributed to fair

value of specific accounts at acquisition date with residual fair

value recognized as goodwill.

3. Prepare entry I to eliminate $122,500 income accrual for 2017

less $11,000 amortization recorded by parent using equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E to recognize current year amortization

expense.

6. Prepare entry S to...

Questions:

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize allocations attributed to fair

value of specific accounts at acquisition date with residual fair

value recognized as goodwill.

3. Prepare entry I to eliminate $122,500 income accrual for 2017

less $11,000 amortization recorded by parent using equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E to recognize current year amortization

expense.

6. Prepare entry S to...

1 Prepare entry S to eliminate stockholders' equity accounts of subsidiary. 2 Prepare entry A to...

1

Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method.

4

Prepare entry D to eliminate intra-entity dividend

transfers.

5

Prepare entry E.

6

Prepare entry *C.

7

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1

Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method.

4

Prepare entry D to eliminate intra-entity dividend

transfers.

5

Prepare entry E.

6

Prepare entry *C.

7

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1. Prepare entry S to eliminate stockholders' equity accounts of subsidiary. 2. Prepare entry A to...

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3. Prepare entry I to eliminate intra-entity income accrual for

the current year based on the parent's usage of the partial equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E.

6. Prepare entry *C.

7. Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3. Prepare entry I to eliminate intra-entity income accrual for

the current year based on the parent's usage of the partial equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E.

6. Prepare entry *C.

7. Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

Tasks: Prepare entry A to recognize allocations determined above in connection with acquisition-date fair values. Prepare...

Tasks:

Prepare entry A to recognize allocations determined above in

connection with acquisition-date fair values.

Prepare entry I to eliminate intra-entity dividend declarations

recorded by parent as income.

Prepare entry E to recognize 2017 amortization expense.

Prepare entry *C to convert parent company figures to equity

method by recognizing subsidiary's increase in book value for prior

year [$104,500 net income less $13,000 dividend declaration] and

excess amortizations for that period [$11,800].

Prepare entry A to recognize allocations relating to

investment—balances...

Tasks:

Prepare entry A to recognize allocations determined above in

connection with acquisition-date fair values.

Prepare entry I to eliminate intra-entity dividend declarations

recorded by parent as income.

Prepare entry E to recognize 2017 amortization expense.

Prepare entry *C to convert parent company figures to equity

method by recognizing subsidiary's increase in book value for prior

year [$104,500 net income less $13,000 dividend declaration] and

excess amortizations for that period [$11,800].

Prepare entry A to recognize allocations relating to

investment—balances...

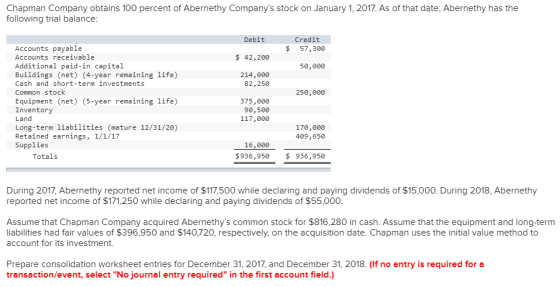

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that...

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that date, Abernethy has the following trial balance: Debit Credit Accounts payable $ 52,400 Accounts receivable $ 48,600 Additional paid-in capital 50,000 Buildings (net) (4-year remaining life) 179,000 Cash and short-term investments 61,250 Common stock 250,000 Equipment (net) (5-year remaining life) 260,000 Inventory 121,500 Land 105,000 Long-term liabilities (mature 12/31/20) 174,500 Retained earnings, 1/1/17 264,650 Supplies 16,200 Totals $ 791,550 $ 791,550 During 2017, Abernethy...

Tasks: Prepare entry A to recognize goodwill portion of the original acquisition fair value. Prepare entry...

Tasks:

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method

Prepare entry D to eliminate intra-entity dividend transfers

Prepare entry E

Prepare entry *C.

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained earnings balance has

been adjusted for 2017 income and dividends

Prepare entry A to recognize original...

Tasks:

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method

Prepare entry D to eliminate intra-entity dividend transfers

Prepare entry E

Prepare entry *C.

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained earnings balance has

been adjusted for 2017 income and dividends

Prepare entry A to recognize original...

Problem 3-20 (LO 3-3b) Chapman Company obtains 100 percent of Abernethy Company's stock on January 1,...

Problem 3-20 (LO 3-3b) Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017. As of that date, Abernethy has the following trial balance Debit Credit Accounts payable $ 52,800 Accounts receivable $ 49,500 Additional paid in capital 50,000 Buildings (net) (4-year remaining life) 174,000 Cash and short-term investments 84,000 Common stock 250,000 Equipment (net) (5.year remaining life) 315,000 Inventory 137,500 Land 90,500 Long-term liabilities (mature 12/31/20) 188,500 Retained earnings, 1/1/17 323,600 Supplies 14,400 Totals $864,900 $...

Problem 3-20 (LO 3-3b) Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017. As of that date, Abernethy has the following trial balance Debit Credit Accounts payable $ 52,800 Accounts receivable $ 49,500 Additional paid in capital 50,000 Buildings (net) (4-year remaining life) 174,000 Cash and short-term investments 84,000 Common stock 250,000 Equipment (net) (5.year remaining life) 315,000 Inventory 137,500 Land 90,500 Long-term liabilities (mature 12/31/20) 188,500 Retained earnings, 1/1/17 323,600 Supplies 14,400 Totals $864,900 $...

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that...

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that date, Abernethy has the following trial balance: Debit Credit Accounts payable $ 58,900 Accounts receivable $ 41,500 Additional paid-in capital 50,000 Buildings (net) (4-year remaining life) 211,000 Cash and short-term investments 70,750 Common stock 250,000 Equipment (net) (5-year remaining life) 430,000 Inventory 139,000 Land 121,500 Long-term liabilities (mature 12/31/20) 174,000 Retained earnings, 1/1/17 498,450 Supplies 17,600 Totals $ 1,031,350 $ 1,031,350 During 2017, Abernethy...

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that...

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2017. As of that date, Abernethy has the following trial balance: Debit Credit Accounts payable $ 52,400 Accounts receivable $ 48,600 Additional paid-in capital 50,000 Buildings (net) (4-year remaining life) 179,000 Cash and short-term investments 61,250 Common stock 250,000 Equipment (net) (5-year remaining life) 260,000 Inventory 121,500 Land 105,000 Long-term liabilities (mature 12/31/20) 174,500 Retained earnings, 1/1/17 264,650 Supplies 16,200 Totals $ 791,550 $ 791,550 During 2017, Abernethy...

Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017 As of that da...

Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017 As of that date, Abernethy has the following trial balance Accounts payable Accounts receivable 5 56,780 s 43,800 Additional paid-in capital Buildings (net) (4-year remaining life) Cash and short-term investments Common stock Equipment (net) (s-year remaining life) Inventory Land Long-term liabilities (mature 12/31/20) Retained earnings, 1/1/17 Supplies 5e,869 143,000 80,250 250,8e 295,00 110,580 112,600 171,e00 268,750 11,988 Totals 796,450796,450 During 2017, Abernethy reported net income of $122.500...

Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017 As of that date, Abernethy has the following trial balance Accounts payable Accounts receivable 5 56,780 s 43,800 Additional paid-in capital Buildings (net) (4-year remaining life) Cash and short-term investments Common stock Equipment (net) (s-year remaining life) Inventory Land Long-term liabilities (mature 12/31/20) Retained earnings, 1/1/17 Supplies 5e,869 143,000 80,250 250,8e 295,00 110,580 112,600 171,e00 268,750 11,988 Totals 796,450796,450 During 2017, Abernethy reported net income of $122.500...

Questions:

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize allocations attributed to fair

value of specific accounts at acquisition date with residual fair

value recognized as goodwill.

3. Prepare entry I to eliminate $122,500 income accrual for 2017

less $11,000 amortization recorded by parent using equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E to recognize current year amortization

expense.

6. Prepare entry S to...

Questions:

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize allocations attributed to fair

value of specific accounts at acquisition date with residual fair

value recognized as goodwill.

3. Prepare entry I to eliminate $122,500 income accrual for 2017

less $11,000 amortization recorded by parent using equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E to recognize current year amortization

expense.

6. Prepare entry S to...

1

Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method.

4

Prepare entry D to eliminate intra-entity dividend

transfers.

5

Prepare entry E.

6

Prepare entry *C.

7

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1

Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method.

4

Prepare entry D to eliminate intra-entity dividend

transfers.

5

Prepare entry E.

6

Prepare entry *C.

7

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3. Prepare entry I to eliminate intra-entity income accrual for

the current year based on the parent's usage of the partial equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E.

6. Prepare entry *C.

7. Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

1. Prepare entry S to eliminate stockholders' equity accounts of

subsidiary.

2. Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

3. Prepare entry I to eliminate intra-entity income accrual for

the current year based on the parent's usage of the partial equity

method.

4. Prepare entry D to eliminate intra-entity dividend

transfers.

5. Prepare entry E.

6. Prepare entry *C.

7. Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained...

Tasks:

Prepare entry A to recognize allocations determined above in

connection with acquisition-date fair values.

Prepare entry I to eliminate intra-entity dividend declarations

recorded by parent as income.

Prepare entry E to recognize 2017 amortization expense.

Prepare entry *C to convert parent company figures to equity

method by recognizing subsidiary's increase in book value for prior

year [$104,500 net income less $13,000 dividend declaration] and

excess amortizations for that period [$11,800].

Prepare entry A to recognize allocations relating to

investment—balances...

Tasks:

Prepare entry A to recognize allocations determined above in

connection with acquisition-date fair values.

Prepare entry I to eliminate intra-entity dividend declarations

recorded by parent as income.

Prepare entry E to recognize 2017 amortization expense.

Prepare entry *C to convert parent company figures to equity

method by recognizing subsidiary's increase in book value for prior

year [$104,500 net income less $13,000 dividend declaration] and

excess amortizations for that period [$11,800].

Prepare entry A to recognize allocations relating to

investment—balances...

Tasks:

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method

Prepare entry D to eliminate intra-entity dividend transfers

Prepare entry E

Prepare entry *C.

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained earnings balance has

been adjusted for 2017 income and dividends

Prepare entry A to recognize original...

Tasks:

Prepare entry A to recognize goodwill portion of the original

acquisition fair value.

Prepare entry I to eliminate intra-entity income accrual for the

current year based on the parent's usage of the partial equity

method

Prepare entry D to eliminate intra-entity dividend transfers

Prepare entry E

Prepare entry *C.

Prepare entry S to eliminate beginning of year stockholders'

equity accounts of subsidiary—the retained earnings balance has

been adjusted for 2017 income and dividends

Prepare entry A to recognize original...

Problem 3-20 (LO 3-3b) Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017. As of that date, Abernethy has the following trial balance Debit Credit Accounts payable $ 52,800 Accounts receivable $ 49,500 Additional paid in capital 50,000 Buildings (net) (4-year remaining life) 174,000 Cash and short-term investments 84,000 Common stock 250,000 Equipment (net) (5.year remaining life) 315,000 Inventory 137,500 Land 90,500 Long-term liabilities (mature 12/31/20) 188,500 Retained earnings, 1/1/17 323,600 Supplies 14,400 Totals $864,900 $...

Problem 3-20 (LO 3-3b) Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017. As of that date, Abernethy has the following trial balance Debit Credit Accounts payable $ 52,800 Accounts receivable $ 49,500 Additional paid in capital 50,000 Buildings (net) (4-year remaining life) 174,000 Cash and short-term investments 84,000 Common stock 250,000 Equipment (net) (5.year remaining life) 315,000 Inventory 137,500 Land 90,500 Long-term liabilities (mature 12/31/20) 188,500 Retained earnings, 1/1/17 323,600 Supplies 14,400 Totals $864,900 $...

Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017 As of that date, Abernethy has the following trial balance Accounts payable Accounts receivable 5 56,780 s 43,800 Additional paid-in capital Buildings (net) (4-year remaining life) Cash and short-term investments Common stock Equipment (net) (s-year remaining life) Inventory Land Long-term liabilities (mature 12/31/20) Retained earnings, 1/1/17 Supplies 5e,869 143,000 80,250 250,8e 295,00 110,580 112,600 171,e00 268,750 11,988 Totals 796,450796,450 During 2017, Abernethy reported net income of $122.500...

Chapman Company obtains 100 percent of Abernethy Company's stock on January 1, 2017 As of that date, Abernethy has the following trial balance Accounts payable Accounts receivable 5 56,780 s 43,800 Additional paid-in capital Buildings (net) (4-year remaining life) Cash and short-term investments Common stock Equipment (net) (s-year remaining life) Inventory Land Long-term liabilities (mature 12/31/20) Retained earnings, 1/1/17 Supplies 5e,869 143,000 80,250 250,8e 295,00 110,580 112,600 171,e00 268,750 11,988 Totals 796,450796,450 During 2017, Abernethy reported net income of $122.500...

Most questions answered within 3 hours.

-

An important news announcement is transmitted by radio waves to

people who are 65 km away,...

asked 13 minutes ago -

On June 30, 2021, Rosetta Granite purchased equipment for

$130,000. The estimated useful life of the...

asked 12 minutes ago -

. If you were the CEO of Agricole, would you pursue an

acquisition target in the...

asked 12 minutes ago -

(a) We define standard Gibbs energy change, G0 =

H0 – TS0, what is the relationship...

asked 13 minutes ago -

If the barometric pressure is 107.4 kPa, what is the pressure in

kPa of the gas...

asked 33 minutes ago -

A resonance tube can be used to measure the speed of sound in

air. A tuning...

asked 27 minutes ago -

Lourdes LLC. keeps a $100 change fund in its cash register. At

the end of the...

asked 32 minutes ago -

State the operation or control mechanism of TRIAC, DIAC, UJT, PUT,

GTO and IGBT.

asked 34 minutes ago -

Generator An AC generator supplies an rms voltage of 220 V at

50.0 Hz. It is...

asked 37 minutes ago -

Cars enter a car wash at a mean rate of 2 cars per half an hour....

asked 49 minutes ago -

Write SQL queries to answer the following question: A. Which

students are enrolled in Database and...

asked 1 hour ago -

Required:

How was Dell computer working capital policy as a competitive

advantage? Write at least 200...

asked 44 minutes ago