On January 1, 2017, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in...

On January 1, 2017, Boston Enterprises issues bonds that have a

$3,400,000 par value, mature in 20 years, and pay 9% interest

semiannually on June 30 and December 31. The bonds are sold at

par.

1. How much interest will Boston pay (in cash) to

the bondholders every six months?

2. Prepare journal entries to record (a) the

issuance of bonds on January 1, 2017; (b) the first interest

payment on June 30, 2017; and (c) the second interest payment on

December 31, 2017.

3. Prepare the journal entry for issuance assuming

the bonds are issued at (a) 98 and (b) 102.

Homework Answers

Accounting: Accounting is a process of recording the transactions, classifying them in a specific manner, and then the process of summarizing and analyzing is carried out to interpret the results. It is a process of preserving the accounts.

Financial accounting is a process of preparing reports to provide all financial information to both the internal and external users of an organization. The financial statements that are prepared under the financial accounting are examined by independent certified public accountants, at the year-end, who would express their opinion on the fairness of the reports shown by a company.

Transaction: Transaction is an act of buying or selling goods or rendering any service that is reliably measured in terms of money.

Journal entry: Journal entry is the recording of transactions in a systematic manner as they occur. Thus, it is a summary of all the transactions which has debit and credit aspects recorded chronologically.

Bonds: Bonds are promises that are made between two or more persons legally. Bonds are issued by the companies for raising their capital balance. Interest is received at regular intervals by a purchaser.

Bonds payable: Bonds payable is a long-term legal agreement issued by a company to several bondholders. Bondholders are entitled to receive a specified interest on the bonds bought by them. Bonds payable is a long-term liability, and therefore reported under long-term liabilities section in the balance sheet.

Bonds issued at discount: When the selling price of the bond is less than the face value represented in the bond, then the bond is said to be issued at discount.

Bonds issued at premium: When the selling price of the bond is higher than the face value represented in the bond, then the bond is said to be issued at premium.

Interest expense: This is a non-operating expense, and it will be shown on the income statement. Generally, this expense is considered as an amount incurred by the company for using the other resources like borrowing loan from bank or purchasing a note and so on.

Golden rules of accounting:

Rules for debit and credit:

When assets increase, debit them; when assets decrease, credit them.

When liabilities increase, credit them; when liabilities decrease, debit them.

When stockholders’ equity increases, credit it; when stockholders’ equity decreases, debit it.

When expenses and losses increase, debit them; when expenses and losses decrease, credit them.

When incomes and gains increase, credit them; when incomes and gains decrease, debit them.

1)

Calculate the interest paid by “B” to the bondholders:

Therefore, the interest paid by “B” to the bondholders for every six months is $153,000.

Working notes:

Calculate the semi-annual interest rate:

Therefore, the semi-annual interest rate is 4.50%.

2.a)

Prepare the journal entry to record the issuance of bonds on January 1, 2017:

Therefore, the cash account is debited and the bonds payable is credited for $3,400,000.

2.b)

Prepare the journal entry to record the issuance of bond at par:

Therefore, the bonds interest expense is debited and the cash account is credited for $153,000.

2.c)

Prepare the journal entry to record the second interest payment on December 31, 2017:

Therefore, the bonds’ interest expense is debited and the cash account is credited for $153,000.

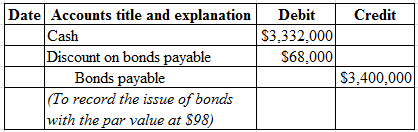

3.a)

Prepare the journal entry to record bond issued at $98:

Therefore, the cash account is debited for $3,332,000, discount on bonds payable is $68,000, and bonds payable is credited for 3,400,000.

Working notes:

Calculate the issue of bonds for $98.

Therefore, the bonds issued for cash is $3,468,000.

Calculate the discount on bonds payable:

Therefore, the discount on bonds payable is $68,000.

3.b)

Prepare the journal entry to record bond issued at $102:

Therefore, the cash account is debited for $3,468,000, premium on bonds payable is credited for $68,000, and bonds payable is credited for 3,400,000.

Working notes:

Calculate the issue of bonds for $102.

Therefore, the bonds issued for cash is $3,468,000.

Calculate the discount on bonds payable:

Therefore, the discount on bonds payable is $68,000.

Ans: Part 1The interest paid by “B” to the bondholders for every six months is $153,000.

Part 2.a

Add Answer to:

On January 1, 2017, Boston Enterprises issues bonds that have a

$3,400,000 par value, mature in...

On January 1, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in 20...

On January 1, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, 2017, Boston Enterprises issues bonds that have a $1,700,000 par value, mature in...

On January 1, 2017, Boston Enterprises issues bonds that have a $1,700,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017; and (c) the second interest payment...

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in...

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017; and (c) the second interest payment...

On January 1, 2017, Boston Enterprises issues bonds that have a $1,750,000 par value, mature in...

On January 1, 2017, Boston Enterprises issues bonds that have a $1,750,000 par value, mature in 20 years, and pay 10% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017; and (c) the second interest...

On January 1, Boston Enterprises issues bonds that have a $1,350,000 par value, mature in 20...

On January 1, Boston Enterprises issues bonds that have a $1,350,000 par value, mature in 20 years, and pay 8% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $1,350,000 par value, mature in 20 years, and pay 8% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $1,500,000 par value, mature in 20...

On January 1, Boston Enterprises issues bonds that have a $1,500,000 par value, mature in 20 years, and pay 6% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $1,600,000 par value, mature in 20...

On January 1, Boston Enterprises issues bonds that have a

$1,600,000 par value, mature in 20 years, and pay 8% interest

semiannually on June 30 and December 31. The bonds are sold at

par.

1. How much interest will Boston pay (in cash) to

the bondholders every six months?

2. Prepare journal entries to record (a) the

issuance of bonds on January 1, (b) the first interest payment on

June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a

$1,600,000 par value, mature in 20 years, and pay 8% interest

semiannually on June 30 and December 31. The bonds are sold at

par.

1. How much interest will Boston pay (in cash) to

the bondholders every six months?

2. Prepare journal entries to record (a) the

issuance of bonds on January 1, (b) the first interest payment on

June 30, and (c) the second interest payment on December 31....

1. 2. Check my Brussels Enterprises issues bonds at par dated January 1, 2019, that have...

1.

2.

Check my Brussels Enterprises issues bonds at par dated January 1, 2019, that have a $3,400,000 par value, mature in four years, and pay 9% interest semiannually on June 30 and December 31. 1. Record the entry for the issuance of bonds for cash on January 1. 2 Record the entry for the first semiannual interest payment and the second semiannual interest payment. 3. Record the entry for the maturity of the bonds on December 31, 2022 (assume...

1.

2.

Check my Brussels Enterprises issues bonds at par dated January 1, 2019, that have a $3,400,000 par value, mature in four years, and pay 9% interest semiannually on June 30 and December 31. 1. Record the entry for the issuance of bonds for cash on January 1. 2 Record the entry for the first semiannual interest payment and the second semiannual interest payment. 3. Record the entry for the maturity of the bonds on December 31, 2022 (assume...

On January 2017, Boston Enterprises issues bonds that have a $250.000 par value, mature in 20...

On January 2017, Boston Enterprises issues bonds that have a $250.000 par value, mature in 20 years, and pay 6% interest semiannually on June 30 and December 31 The bonds are sold at pat 1. How much interest will Boston pay in cash to the bondholders every six months? 2. Prepare yournal entries to record in the issuance of bonds on January 1, 2017, the first interest payment on June 30, 2017, and (c) the second interest payment on December...

On January 2017, Boston Enterprises issues bonds that have a $250.000 par value, mature in 20 years, and pay 6% interest semiannually on June 30 and December 31 The bonds are sold at pat 1. How much interest will Boston pay in cash to the bondholders every six months? 2. Prepare yournal entries to record in the issuance of bonds on January 1, 2017, the first interest payment on June 30, 2017, and (c) the second interest payment on December...

need help answering the questions ...thanks On January 1, 2017, Boston Enterprises issues bonds that have...

need help answering the questions ...thanks

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017;...

need help answering the questions ...thanks

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017;...

On January 1, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $3,400,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $1,350,000 par value, mature in 20 years, and pay 8% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a $1,350,000 par value, mature in 20 years, and pay 8% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, (b) the first interest payment on June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a

$1,600,000 par value, mature in 20 years, and pay 8% interest

semiannually on June 30 and December 31. The bonds are sold at

par.

1. How much interest will Boston pay (in cash) to

the bondholders every six months?

2. Prepare journal entries to record (a) the

issuance of bonds on January 1, (b) the first interest payment on

June 30, and (c) the second interest payment on December 31....

On January 1, Boston Enterprises issues bonds that have a

$1,600,000 par value, mature in 20 years, and pay 8% interest

semiannually on June 30 and December 31. The bonds are sold at

par.

1. How much interest will Boston pay (in cash) to

the bondholders every six months?

2. Prepare journal entries to record (a) the

issuance of bonds on January 1, (b) the first interest payment on

June 30, and (c) the second interest payment on December 31....

1.

2.

Check my Brussels Enterprises issues bonds at par dated January 1, 2019, that have a $3,400,000 par value, mature in four years, and pay 9% interest semiannually on June 30 and December 31. 1. Record the entry for the issuance of bonds for cash on January 1. 2 Record the entry for the first semiannual interest payment and the second semiannual interest payment. 3. Record the entry for the maturity of the bonds on December 31, 2022 (assume...

1.

2.

Check my Brussels Enterprises issues bonds at par dated January 1, 2019, that have a $3,400,000 par value, mature in four years, and pay 9% interest semiannually on June 30 and December 31. 1. Record the entry for the issuance of bonds for cash on January 1. 2 Record the entry for the first semiannual interest payment and the second semiannual interest payment. 3. Record the entry for the maturity of the bonds on December 31, 2022 (assume...

On January 2017, Boston Enterprises issues bonds that have a $250.000 par value, mature in 20 years, and pay 6% interest semiannually on June 30 and December 31 The bonds are sold at pat 1. How much interest will Boston pay in cash to the bondholders every six months? 2. Prepare yournal entries to record in the issuance of bonds on January 1, 2017, the first interest payment on June 30, 2017, and (c) the second interest payment on December...

On January 2017, Boston Enterprises issues bonds that have a $250.000 par value, mature in 20 years, and pay 6% interest semiannually on June 30 and December 31 The bonds are sold at pat 1. How much interest will Boston pay in cash to the bondholders every six months? 2. Prepare yournal entries to record in the issuance of bonds on January 1, 2017, the first interest payment on June 30, 2017, and (c) the second interest payment on December...

need help answering the questions ...thanks

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017;...

need help answering the questions ...thanks

On January 1, 2017, Boston Enterprises issues bonds that have a $1,200,000 par value, mature in 20 years, and pay 9% interest semiannually on June 30 and December 31. The bonds are sold at par. 1. How much interest will Boston pay (in cash) to the bondholders every six months? 2. Prepare journal entries to record (a) the issuance of bonds on January 1, 2017; (b) the first interest payment on June 30, 2017;...

Most questions answered within 3 hours.

-

2) You are given the task of finding a representation for a

circle in a drawing...

asked 37 minutes ago -

STUDY QUESTION: Does use of diet drug fen-phen

(fenfluramine-phentermine) cause valvular heart disease?

HINT: Valvular heart...

asked 29 minutes ago -

1. An object weighing 40 N rests on a surface. The coefficient

of friction is 0.35....

asked 1 hour ago -

Investor company owns 35% of investee company voting stock and

accounts for the investment under the...

asked 2 hours ago -

The number of major faults on a randomly chosen 1 km stretch of

highway has a...

asked 3 hours ago -

Consider the competitive environment of Starbuck's, Progressive

Insurance, a manufacturing firm with low turnover, or a...

asked 4 hours ago -

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 5 hours ago -

A business executive has the option to invest money in two

plans: Plan A guarantees that...

asked 8 hours ago -

Hello, can someone please help me answer this question?

How much heat is absorbed by a...

asked 8 hours ago -

. A marketing researcher conducted a survey of 25 shoppers

randomly selected at the local mall...

asked 8 hours ago -

Create an comprehensive response to the

following:

Antimicrobial agents work on a multitude of microbes (bacteria,...

asked 8 hours ago -

6.13 LAB: Step counter. Section 6.3.

A pedometer treats walking 2,000 steps as walking 1 mile....

asked 8 hours ago