Homework Answers

Add Answer to:

8. Let X,.. , Xn be a random sampl le from a uniform(O, 0) distributio n....

3. Suppose that Xi,.... Xn is a random sample from a uniform distribution over [0,0) That...

3. Suppose that Xi,.... Xn is a random sample from a uniform distribution over [0,0) That is, 0 elsewhere Also suppose that the prior distribution of θ is a Pareto distribution with density 0 elsewhere where θ0 > 0 and α > 1. (a) Determine (b) Show , θ > max(T1 , . . . ,Zn,%) and hence deduce the posterior density of θ given x, . . . ,Zn is (c) Compute the mean of the posterior distribution and...

3. Suppose that Xi,.... Xn is a random sample from a uniform distribution over [0,0) That is, 0 elsewhere Also suppose that the prior distribution of θ is a Pareto distribution with density 0 elsewhere where θ0 > 0 and α > 1. (a) Determine (b) Show , θ > max(T1 , . . . ,Zn,%) and hence deduce the posterior density of θ given x, . . . ,Zn is (c) Compute the mean of the posterior distribution and...

Specifically, suppose that Xi, X2, .., Xn denote n payments, modeled as iid random variables with...

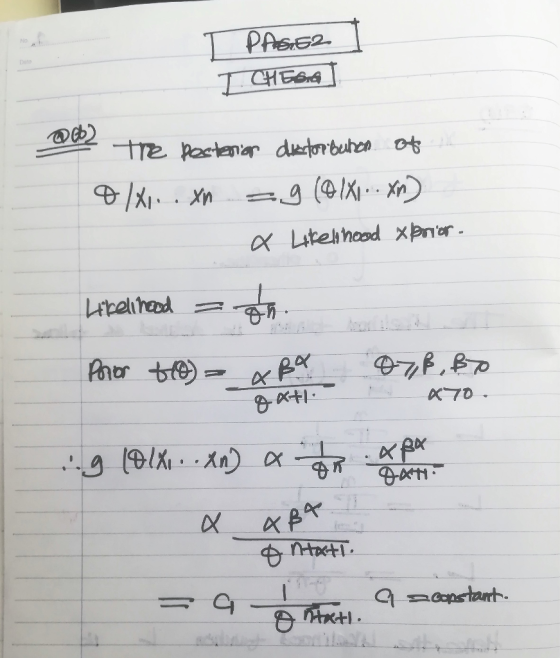

Specifically, suppose that Xi, X2, .., Xn denote n payments, modeled as iid random variables with common Weibull pdf 0, otherwise, where m > 0 is known and θ is unknown. In turn, suppose that θ ~ IG(α, β), that is, θ has an inverted gamma (prior) pdf 0, otherwise (a) Prove that the inverted gamma IG(α, β) prior is a conjugate prior for the Weibull family above. (b) Suppose that m-2, α-05, and β-2. Here are n-10 insurance payments...

Specifically, suppose that Xi, X2, .., Xn denote n payments, modeled as iid random variables with common Weibull pdf 0, otherwise, where m > 0 is known and θ is unknown. In turn, suppose that θ ~ IG(α, β), that is, θ has an inverted gamma (prior) pdf 0, otherwise (a) Prove that the inverted gamma IG(α, β) prior is a conjugate prior for the Weibull family above. (b) Suppose that m-2, α-05, and β-2. Here are n-10 insurance payments...

Problem 3.1 Suppose that XI, X2,... Xn is a random sample of size n is to...

Problem 3.1 Suppose that XI, X2,... Xn is a random sample of size n is to be taken from a Bermoulli distribution for which the value of the parameter θ is unknown, and the prior distribution of θ is a Beta(α,β) distribution. Represent the mean of this prior distribution as μο=α/(α+p). The posterior distribution of θ is Beta =e+ ΣΧ, β.-β+n-ΣΧ.) a) Show that the mean of the posterior distribution is a weighted average of the form where yn and...

Problem 3.1 Suppose that XI, X2,... Xn is a random sample of size n is to be taken from a Bermoulli distribution for which the value of the parameter θ is unknown, and the prior distribution of θ is a Beta(α,β) distribution. Represent the mean of this prior distribution as μο=α/(α+p). The posterior distribution of θ is Beta =e+ ΣΧ, β.-β+n-ΣΧ.) a) Show that the mean of the posterior distribution is a weighted average of the form where yn and...

3. Let Xi, , Xn be a random sample from a Poisson distribution with p.m.f Assume...

3. Let Xi, , Xn be a random sample from a Poisson distribution with p.m.f Assume the prior distribution of Of λ is is an exponential with mean 1, i.e. the prior pdi g(A) e-λ, λ > 0 Note that the exponential distribution is a special gamma distribution; and a general gamma distribution with parameters α > 0 and β > 0 has the pd.f. h(A; α, β)-16(. otherwise Also the mean of a gamma random variable with the pd.f.h(Χα,...

3. Let Xi, , Xn be a random sample from a Poisson distribution with p.m.f Assume the prior distribution of Of λ is is an exponential with mean 1, i.e. the prior pdi g(A) e-λ, λ > 0 Note that the exponential distribution is a special gamma distribution; and a general gamma distribution with parameters α > 0 and β > 0 has the pd.f. h(A; α, β)-16(. otherwise Also the mean of a gamma random variable with the pd.f.h(Χα,...

Let X1, . . . , Xn be a random sample following Gamma(2, β) for some...

Let X1, . . . , Xn be a random sample following Gamma(2, β) for some unknown parameter β > 0. (i) Now let’s think like a Bayesian. Consider a prior distribution of β ∼ Gamma(a, b) for some a, b > 0. Derive the posterior distribution of β given (X1, . . . , Xn) = (x1,...,xn). (j) What is the posterior Bayes estimator of β assuming squared error loss?

Let the random sample X1, . . . , Xn be taken from the Binomial distribution...

Let the random sample X1, . . . , Xn be taken from the Binomial distribution with parameter θ, which is unknown and must be estimated. Let the prior distribution of θ be the beta distribution with known parameters α > 0 and β > 0. Find the Bayes risk and the Bayes estimator using squared error loss. estimator of θ.

Let Xi,..,Xn be a random sample from a population with pdf 0, x 0 is unknown. (a) Show that the G...

Please answer the following question and show every step. Thank

you.

Let Xi,..,Xn be a random sample from a population with pdf 0, x<0, where θ > 0 is unknown. (a) Show that the Gamma(a, b) prior with pdf 0, θ < 0. is a conjugate prior for θ (a > 0 and b > 0 are known constants). (b) Find the Bayes estimator of θ under square error loss. (c) Find the Bayes estimator of (2π-10)1/2 under square error...

Please answer the following question and show every step. Thank

you.

Let Xi,..,Xn be a random sample from a population with pdf 0, x<0, where θ > 0 is unknown. (a) Show that the Gamma(a, b) prior with pdf 0, θ < 0. is a conjugate prior for θ (a > 0 and b > 0 are known constants). (b) Find the Bayes estimator of θ under square error loss. (c) Find the Bayes estimator of (2π-10)1/2 under square error...

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co Let Xi, c〉0. Xn be i.i.d. from the Pareto di...

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co Let Xi, c〉0. Xn be i.i.d. from the Pareto di...

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

1. Let X1, ..., Xn be a random sample from a distribution with the pdf le-x/0,...

1. Let X1, ..., Xn be a random sample from a distribution with the pdf le-x/0, x > 0, N = (0,00). (a) Find the maximum likelihood estimator of 0. (b) Find the method of moments estimator of 0. (c) Are the estimators in a) and b) unbiased? (d) What is the variance of the estimators in a) and b)? (e) Suppose the observed sample is 2.26, 0.31, 3.75, 6.92, 9.10, 7.57, 4.79, 1.41, 2.49, 0.59. Find the maximum likelihood...

1. Let X1, ..., Xn be a random sample from a distribution with the pdf le-x/0, x > 0, N = (0,00). (a) Find the maximum likelihood estimator of 0. (b) Find the method of moments estimator of 0. (c) Are the estimators in a) and b) unbiased? (d) What is the variance of the estimators in a) and b)? (e) Suppose the observed sample is 2.26, 0.31, 3.75, 6.92, 9.10, 7.57, 4.79, 1.41, 2.49, 0.59. Find the maximum likelihood...

3. Suppose that Xi,.... Xn is a random sample from a uniform distribution over [0,0) That is, 0 elsewhere Also suppose that the prior distribution of θ is a Pareto distribution with density 0 elsewhere where θ0 > 0 and α > 1. (a) Determine (b) Show , θ > max(T1 , . . . ,Zn,%) and hence deduce the posterior density of θ given x, . . . ,Zn is (c) Compute the mean of the posterior distribution and...

3. Suppose that Xi,.... Xn is a random sample from a uniform distribution over [0,0) That is, 0 elsewhere Also suppose that the prior distribution of θ is a Pareto distribution with density 0 elsewhere where θ0 > 0 and α > 1. (a) Determine (b) Show , θ > max(T1 , . . . ,Zn,%) and hence deduce the posterior density of θ given x, . . . ,Zn is (c) Compute the mean of the posterior distribution and...

Specifically, suppose that Xi, X2, .., Xn denote n payments, modeled as iid random variables with common Weibull pdf 0, otherwise, where m > 0 is known and θ is unknown. In turn, suppose that θ ~ IG(α, β), that is, θ has an inverted gamma (prior) pdf 0, otherwise (a) Prove that the inverted gamma IG(α, β) prior is a conjugate prior for the Weibull family above. (b) Suppose that m-2, α-05, and β-2. Here are n-10 insurance payments...

Specifically, suppose that Xi, X2, .., Xn denote n payments, modeled as iid random variables with common Weibull pdf 0, otherwise, where m > 0 is known and θ is unknown. In turn, suppose that θ ~ IG(α, β), that is, θ has an inverted gamma (prior) pdf 0, otherwise (a) Prove that the inverted gamma IG(α, β) prior is a conjugate prior for the Weibull family above. (b) Suppose that m-2, α-05, and β-2. Here are n-10 insurance payments...

Problem 3.1 Suppose that XI, X2,... Xn is a random sample of size n is to be taken from a Bermoulli distribution for which the value of the parameter θ is unknown, and the prior distribution of θ is a Beta(α,β) distribution. Represent the mean of this prior distribution as μο=α/(α+p). The posterior distribution of θ is Beta =e+ ΣΧ, β.-β+n-ΣΧ.) a) Show that the mean of the posterior distribution is a weighted average of the form where yn and...

Problem 3.1 Suppose that XI, X2,... Xn is a random sample of size n is to be taken from a Bermoulli distribution for which the value of the parameter θ is unknown, and the prior distribution of θ is a Beta(α,β) distribution. Represent the mean of this prior distribution as μο=α/(α+p). The posterior distribution of θ is Beta =e+ ΣΧ, β.-β+n-ΣΧ.) a) Show that the mean of the posterior distribution is a weighted average of the form where yn and...

3. Let Xi, , Xn be a random sample from a Poisson distribution with p.m.f Assume the prior distribution of Of λ is is an exponential with mean 1, i.e. the prior pdi g(A) e-λ, λ > 0 Note that the exponential distribution is a special gamma distribution; and a general gamma distribution with parameters α > 0 and β > 0 has the pd.f. h(A; α, β)-16(. otherwise Also the mean of a gamma random variable with the pd.f.h(Χα,...

3. Let Xi, , Xn be a random sample from a Poisson distribution with p.m.f Assume the prior distribution of Of λ is is an exponential with mean 1, i.e. the prior pdi g(A) e-λ, λ > 0 Note that the exponential distribution is a special gamma distribution; and a general gamma distribution with parameters α > 0 and β > 0 has the pd.f. h(A; α, β)-16(. otherwise Also the mean of a gamma random variable with the pd.f.h(Χα,...

Please answer the following question and show every step. Thank

you.

Let Xi,..,Xn be a random sample from a population with pdf 0, x<0, where θ > 0 is unknown. (a) Show that the Gamma(a, b) prior with pdf 0, θ < 0. is a conjugate prior for θ (a > 0 and b > 0 are known constants). (b) Find the Bayes estimator of θ under square error loss. (c) Find the Bayes estimator of (2π-10)1/2 under square error...

Please answer the following question and show every step. Thank

you.

Let Xi,..,Xn be a random sample from a population with pdf 0, x<0, where θ > 0 is unknown. (a) Show that the Gamma(a, b) prior with pdf 0, θ < 0. is a conjugate prior for θ (a > 0 and b > 0 are known constants). (b) Find the Bayes estimator of θ under square error loss. (c) Find the Bayes estimator of (2π-10)1/2 under square error...

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

Let Xi, c〉0. Xn be i.i.d. from the Pareto distribution Pa(θ.e), θ 〉 0 Derive a ÙNIP test of size α for testing Ho : θ-Bo, c co versus 0, C > Co

1. Let X1, ..., Xn be a random sample from a distribution with the pdf le-x/0, x > 0, N = (0,00). (a) Find the maximum likelihood estimator of 0. (b) Find the method of moments estimator of 0. (c) Are the estimators in a) and b) unbiased? (d) What is the variance of the estimators in a) and b)? (e) Suppose the observed sample is 2.26, 0.31, 3.75, 6.92, 9.10, 7.57, 4.79, 1.41, 2.49, 0.59. Find the maximum likelihood...

1. Let X1, ..., Xn be a random sample from a distribution with the pdf le-x/0, x > 0, N = (0,00). (a) Find the maximum likelihood estimator of 0. (b) Find the method of moments estimator of 0. (c) Are the estimators in a) and b) unbiased? (d) What is the variance of the estimators in a) and b)? (e) Suppose the observed sample is 2.26, 0.31, 3.75, 6.92, 9.10, 7.57, 4.79, 1.41, 2.49, 0.59. Find the maximum likelihood...

Most questions answered within 3 hours.

-

MAN3240 Organizational Behavior

In one to two paragraphs

6.) How can understanding emotions make me more...

asked 7 minutes ago -

Identify one individual who, in your opinion, is an excellent

leader. List the qualities that this...

asked 4 minutes ago -

For the data set shown below, complete parts (a) through (d)

below. x 3 4 5...

asked 10 minutes ago -

A university administrator working in student housing wants to

determine if the percentage of students residing...

asked 24 minutes ago -

3). Describe human population growth that has occurred in the

past 400 years. Use terms learned...

asked 21 minutes ago -

A

projectile is blue at a target. The distance from the point of

impact to the...

asked 46 minutes ago -

Given a 32 bit processor, with 2 MB of physical RAM split into 512

frames. What...

asked 36 minutes ago -

What were the main rulings in the Supreme Court cases which are

Morgan v. Virginia (1946)...

asked 35 minutes ago -

write a five paragraph essay on how setting,

specifically culture, influences the actions of

the characters...

asked 27 minutes ago -

JAVA

Provide a simple code sample of Merge sort

asked 38 minutes ago -

Discounting cash flows involves:

A. taking the cash discount offered on a trade merchandise

B. estimating...

asked 45 minutes ago -

A solid wood door 1.00 m wide and 2.00 m high is hinged along

one side...

asked 45 minutes ago