Homework Answers

Please refer to below spreadsheets for calculations and answers.

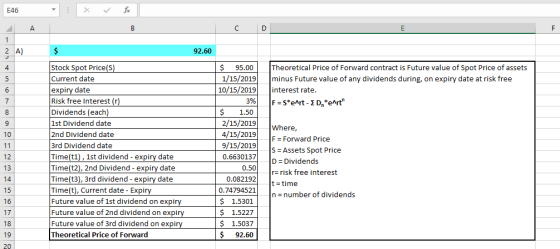

A.

Formula reference-

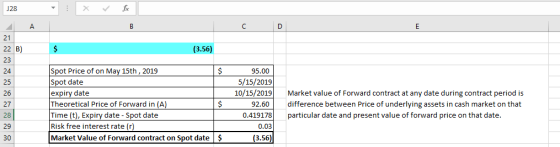

B.

Formula reference -

C.

Formula reference -

D.

Formula Reference -

Add Answer to:

Please use excel to do it!

Consider XYZ stock currently worth S95. On Jan 15h, 2019,...

Please use excel to do it. Consider XYZ stock currently worth $95. On Jan 15, 2019,...

Please use excel to do it.

Consider XYZ stock currently worth $95. On Jan 15, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 1sth, 2019. Assume that the risk-free interest rate will remain at 3.090 p.a. in 2019. Use continuous compounding method...

Please use excel to do it.

Consider XYZ stock currently worth $95. On Jan 15, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 1sth, 2019. Assume that the risk-free interest rate will remain at 3.090 p.a. in 2019. Use continuous compounding method...

Please use EXCEL to do it, Thanks! Consider XYZ stock currently worth $95. On Jan 15th,...

Please use EXCEL to do it, Thanks!

Consider XYZ stock currently worth $95. On Jan 15th, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 151h, 2019. Assume that the risk free interest rate will remain at 3.0% pa. in 2019. Use continuous...

Please use EXCEL to do it, Thanks!

Consider XYZ stock currently worth $95. On Jan 15th, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 151h, 2019. Assume that the risk free interest rate will remain at 3.0% pa. in 2019. Use continuous...

Please use EXCEL to do it, Thanks! Show your answers along with the formula and steps...

Please use EXCEL to do it, Thanks!

Show your answers along with the formula and steps you used for each question Problem 2: A US-based firm expects to pay 1,000,000 for importing goods 90 days later. Thc firm's manager want to hedgc against possible currency risk in the future. The risk-free rate in US is 2% pa and the Euro risk-free rate is 3% pa Both interest rates will remain the same in 90 days. The current spot exchange rate...

Please use EXCEL to do it, Thanks!

Show your answers along with the formula and steps you used for each question Problem 2: A US-based firm expects to pay 1,000,000 for importing goods 90 days later. Thc firm's manager want to hedgc against possible currency risk in the future. The risk-free rate in US is 2% pa and the Euro risk-free rate is 3% pa Both interest rates will remain the same in 90 days. The current spot exchange rate...

Assume that you own a dividend-paying stock currently worth $150. You plan to sell the stock in 2...

Assume that you own a dividend-paying stock currently worth $150. You plan to sell the stock in 250 days. In order to hedge against a possible price decline, you wish to take a short position in a forward contract that expires in 250 days. The risk-free rate is 5.25% per annum (discretely compounding). Over the next 250 days, the stock will pay dividends according to the following schedule: Days to Next Dividend Dividends per Share ($) 30 1.25 120 1.25...

You enter into a 6-month long forward contract on XYZ stock. The forward price is 50....

You enter into a 6-month long forward contract on XYZ stock. The forward price is 50. What is the payoff to your long forward if XYZ stock rises to 53 at 6 months? You enter into a 6-month short forward contract on XYZ stock. The forward price is 50. What is the payoff to your short forward if XYZ stock rises to 51 at 6 months? You purchase a European call option on XYZ stock with strike price 50. What...

You enter into a 6-month long forward contract on XYZ stock. The forward price is 50. What is the payoff to your long forward if XYZ stock rises to 53 at 6 months? You enter into a 6-month short forward contract on XYZ stock. The forward price is 50. What is the payoff to your short forward if XYZ stock rises to 51 at 6 months? You purchase a European call option on XYZ stock with strike price 50. What...

- On 8/15/2019, a 3-year forward contract, expiring 8/15/2022, on a non-dividend-paying stock was entered into...

- On 8/15/2019, a 3-year forward contract, expiring 8/15/2022, on a non-dividend-paying stock was entered into when the stock price was $55 and the risk-free interest rate was 10.8% per annum with continuous compounding. 1 year later, on 8/15/2020, the stock price becomes $58. What is the "delivery" price of the forward contract entered into on 8/15/2019? Round your answer to the nearest 2 decimal points. For example, if your answer is $12.345, then enter "12.35" in the answer box....

Please use EXCEL to do it Show your answers along with the formula and steps you...

Please use EXCEL to do it

Show your answers along with the formula and steps you used for each question Table 1.en January 1,2019 LIBOR so Im days) Problem 3: On January 1, 2019,a US-based lender wishes to hedge against decrease n future interest rates. The lender proposes to hedge against this risk by entering into an FRA with the notional amount of S10 million Use 30/360 day ceent coav ention ลnd simple interest rate 540% 530% s 20% 510%...

Please use EXCEL to do it

Show your answers along with the formula and steps you used for each question Table 1.en January 1,2019 LIBOR so Im days) Problem 3: On January 1, 2019,a US-based lender wishes to hedge against decrease n future interest rates. The lender proposes to hedge against this risk by entering into an FRA with the notional amount of S10 million Use 30/360 day ceent coav ention ลnd simple interest rate 540% 530% s 20% 510%...

Exercise 3. A short forward contract on a dividend-paying stock was entered some time ago. It currently has 9 months to maturity. The stock price and the delivery price is s25 and $24 respectively. T...

Exercise 3. A short forward contract on a dividend-paying stock was entered some time ago. It currently has 9 months to maturity. The stock price and the delivery price is s25 and $24 respectively. The risk-free interest rate with continuous compounding is 8% per annum. The underlying stock is expected to pay a dividend of $2 per share in 2 months and an another dividend of $2 in 6 months. (a) What is the (initial) value of this forward contract?...

Exercise 3. A short forward contract on a dividend-paying stock was entered some time ago. It currently has 9 months to maturity. The stock price and the delivery price is s25 and $24 respectively. The risk-free interest rate with continuous compounding is 8% per annum. The underlying stock is expected to pay a dividend of $2 per share in 2 months and an another dividend of $2 in 6 months. (a) What is the (initial) value of this forward contract?...

5. (a) Explain the differences between a forward contract and an option. [2] (b) An investor...

5. (a) Explain the differences between a forward contract and an option. [2] (b) An investor has taken a short position in a forward contract. If Sy is the price of the underlying stock at maturity and K is the strike, what is the payoff for the investor? Does the investor expect the underlying stock price to increase or decrease? Explain your answer. (2) (c) (i) An investor has just taken a short position in a 6-month forward contract on...

5. (a) Explain the differences between a forward contract and an option. [2] (b) An investor has taken a short position in a forward contract. If Sy is the price of the underlying stock at maturity and K is the strike, what is the payoff for the investor? Does the investor expect the underlying stock price to increase or decrease? Explain your answer. (2) (c) (i) An investor has just taken a short position in a 6-month forward contract on...

4. Forward and Futures Prices A. (6 points) Suppose the stock price is $35 and the...

4. Forward and Futures Prices A. (6 points) Suppose the stock price is $35 and the continuously compounded interest rate is 5%. What is the 6-month forward price, assuming dividends are zero? B. (6 points) If the forward price is $35.50, what is the annualized continuous dividend yield? 5. Forward and Futures Prices Suppose you are a market-maker in S&R index forward contracts. The S&R index spot price is 1100, the risk-free rate is 5%, and the dividend yield on...

4. Forward and Futures Prices A. (6 points) Suppose the stock price is $35 and the continuously compounded interest rate is 5%. What is the 6-month forward price, assuming dividends are zero? B. (6 points) If the forward price is $35.50, what is the annualized continuous dividend yield? 5. Forward and Futures Prices Suppose you are a market-maker in S&R index forward contracts. The S&R index spot price is 1100, the risk-free rate is 5%, and the dividend yield on...

Please use excel to do it.

Consider XYZ stock currently worth $95. On Jan 15, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 1sth, 2019. Assume that the risk-free interest rate will remain at 3.090 p.a. in 2019. Use continuous compounding method...

Please use excel to do it.

Consider XYZ stock currently worth $95. On Jan 15, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 1sth, 2019. Assume that the risk-free interest rate will remain at 3.090 p.a. in 2019. Use continuous compounding method...

Please use EXCEL to do it, Thanks!

Consider XYZ stock currently worth $95. On Jan 15th, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 151h, 2019. Assume that the risk free interest rate will remain at 3.0% pa. in 2019. Use continuous...

Please use EXCEL to do it, Thanks!

Consider XYZ stock currently worth $95. On Jan 15th, 2019, you plan to sell it 9 months later on Oct 15h, 2019 to raise money, but are concerned that the price may have fallen significantly by then. To hedge this risk, you enter into a forward contract to the stock which will mature on Oct 151h, 2019. Assume that the risk free interest rate will remain at 3.0% pa. in 2019. Use continuous...

Please use EXCEL to do it, Thanks!

Show your answers along with the formula and steps you used for each question Problem 2: A US-based firm expects to pay 1,000,000 for importing goods 90 days later. Thc firm's manager want to hedgc against possible currency risk in the future. The risk-free rate in US is 2% pa and the Euro risk-free rate is 3% pa Both interest rates will remain the same in 90 days. The current spot exchange rate...

Please use EXCEL to do it, Thanks!

Show your answers along with the formula and steps you used for each question Problem 2: A US-based firm expects to pay 1,000,000 for importing goods 90 days later. Thc firm's manager want to hedgc against possible currency risk in the future. The risk-free rate in US is 2% pa and the Euro risk-free rate is 3% pa Both interest rates will remain the same in 90 days. The current spot exchange rate...

You enter into a 6-month long forward contract on XYZ stock. The forward price is 50. What is the payoff to your long forward if XYZ stock rises to 53 at 6 months? You enter into a 6-month short forward contract on XYZ stock. The forward price is 50. What is the payoff to your short forward if XYZ stock rises to 51 at 6 months? You purchase a European call option on XYZ stock with strike price 50. What...

You enter into a 6-month long forward contract on XYZ stock. The forward price is 50. What is the payoff to your long forward if XYZ stock rises to 53 at 6 months? You enter into a 6-month short forward contract on XYZ stock. The forward price is 50. What is the payoff to your short forward if XYZ stock rises to 51 at 6 months? You purchase a European call option on XYZ stock with strike price 50. What...

Please use EXCEL to do it

Show your answers along with the formula and steps you used for each question Table 1.en January 1,2019 LIBOR so Im days) Problem 3: On January 1, 2019,a US-based lender wishes to hedge against decrease n future interest rates. The lender proposes to hedge against this risk by entering into an FRA with the notional amount of S10 million Use 30/360 day ceent coav ention ลnd simple interest rate 540% 530% s 20% 510%...

Please use EXCEL to do it

Show your answers along with the formula and steps you used for each question Table 1.en January 1,2019 LIBOR so Im days) Problem 3: On January 1, 2019,a US-based lender wishes to hedge against decrease n future interest rates. The lender proposes to hedge against this risk by entering into an FRA with the notional amount of S10 million Use 30/360 day ceent coav ention ลnd simple interest rate 540% 530% s 20% 510%...

Exercise 3. A short forward contract on a dividend-paying stock was entered some time ago. It currently has 9 months to maturity. The stock price and the delivery price is s25 and $24 respectively. The risk-free interest rate with continuous compounding is 8% per annum. The underlying stock is expected to pay a dividend of $2 per share in 2 months and an another dividend of $2 in 6 months. (a) What is the (initial) value of this forward contract?...

Exercise 3. A short forward contract on a dividend-paying stock was entered some time ago. It currently has 9 months to maturity. The stock price and the delivery price is s25 and $24 respectively. The risk-free interest rate with continuous compounding is 8% per annum. The underlying stock is expected to pay a dividend of $2 per share in 2 months and an another dividend of $2 in 6 months. (a) What is the (initial) value of this forward contract?...

5. (a) Explain the differences between a forward contract and an option. [2] (b) An investor has taken a short position in a forward contract. If Sy is the price of the underlying stock at maturity and K is the strike, what is the payoff for the investor? Does the investor expect the underlying stock price to increase or decrease? Explain your answer. (2) (c) (i) An investor has just taken a short position in a 6-month forward contract on...

5. (a) Explain the differences between a forward contract and an option. [2] (b) An investor has taken a short position in a forward contract. If Sy is the price of the underlying stock at maturity and K is the strike, what is the payoff for the investor? Does the investor expect the underlying stock price to increase or decrease? Explain your answer. (2) (c) (i) An investor has just taken a short position in a 6-month forward contract on...

4. Forward and Futures Prices A. (6 points) Suppose the stock price is $35 and the continuously compounded interest rate is 5%. What is the 6-month forward price, assuming dividends are zero? B. (6 points) If the forward price is $35.50, what is the annualized continuous dividend yield? 5. Forward and Futures Prices Suppose you are a market-maker in S&R index forward contracts. The S&R index spot price is 1100, the risk-free rate is 5%, and the dividend yield on...

4. Forward and Futures Prices A. (6 points) Suppose the stock price is $35 and the continuously compounded interest rate is 5%. What is the 6-month forward price, assuming dividends are zero? B. (6 points) If the forward price is $35.50, what is the annualized continuous dividend yield? 5. Forward and Futures Prices Suppose you are a market-maker in S&R index forward contracts. The S&R index spot price is 1100, the risk-free rate is 5%, and the dividend yield on...

Most questions answered within 3 hours.

-

You are attempting to calculate a firm’s free cash flow to

equity. You know the following...

asked 41 minutes ago -

the following reaction occurs in a balloon containing

N2O2 gas

N2O4(g)=2NO2(g)

will the volume of the...

asked 1 hour ago -

answer the questions throughout this program

public class Day implements Comparable {

Private Boolean atWork;...

asked 1 hour ago -

This is C++ code for parking fee management program

#include <iostream>

#include <iomanip>

using namespace std;...

asked 1 hour ago -

The free energy change for the following reaction at 25 °C, when

[Sn2+] = 1.17 M...

asked 3 hours ago -

An MNE is this kind of industry when competition in one country

is essentially independent of...

asked 4 hours ago -

. For this set of questions, determine what

proportion of a normal distribution is located betweeneach...

asked 5 hours ago -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 6 hours ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 6 hours ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 6 hours ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 7 hours ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 7 hours ago