Spot $ 0.8221 30-day forward $ 0.8542 90-day forward $ 0.8559 180-day forward $ 0.8606 What...

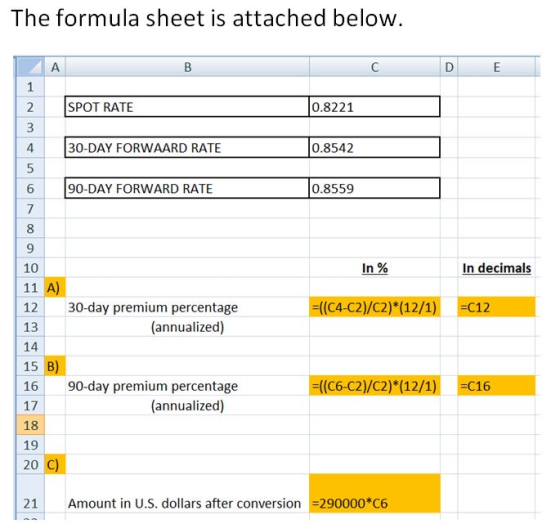

Spot $ 0.8221 30-day forward $ 0.8542 90-day forward $ 0.8559 180-day forward $ 0.8606 What was the 30-day forward premium (or discount) percentage? What was the 90-day forward premium (or discount) percentage? Suppose you executed a 90-day forward contract to exchange 290,000 Swiss francs into U.S. dollars. How many dollars would you get 90 days hence? so for the first question I got 0.544, this was obviously wrong and I know it wont allow me to answer the remaining questions, can you show me how to work these out please?

Homework Answers

Add Answer to:

Spot $ 0.8221 30-day forward $ 0.8542 90-day forward $ 0.8559

180-day forward $ 0.8606 What...

The Wall Street Journal reported the following spot and forward rates for the Swiss franc ($/SF)....

The Wall Street Journal reported the following spot and forward rates for the Swiss franc ($/SF). Spot $ 0.8215 30-day forward $ 0.8530 90-day forward $ 0.8553 180-day forward $ 0.8600 a. Was the Swiss franc selling at a discount or premium in the forward market? Discount Premium b. What was the 30-day forward premium (or discount) percentage? (Do not round intermediate calculations. Input your answer as a percent rounded to 2 decimal places.) c. What was the 90-day forward...

3.1) Assume that 90-day U.S. securities have a 2.4% (rh) annualized interest rate whereas 90-day Swiss...

3.1) Assume that 90-day U.S. securities have a 2.4% (rh) annualized interest rate whereas 90-day Swiss securities have a 3%(rf) annualized interest rate. In the spot market, 1 U.S. dollar can be exchanged for 1.15 Swiss francs. If interest rate parity holds, what is the 90-day forward rate exchange between U.S. and Swiss francs? is the Swiss franc selling at a premium or discount on the forward rate?

Spot Question 2 Given below are spot and forward rates expressed in US dollars per unit...

Spot Question 2 Given below are spot and forward rates expressed in US dollars per unit of the Euro and £ Rates 1.5393 1.6030 30 days forward 1.5406 1.6006 60 days forward 1.5425 1.6000 90 days 1.5431 1.5945 180 days 1.5478 1.5859 Required: i. Is the 90-day forward € quoted at a discount or at a premium? ii. Is the 90-day forward contract in pound trading at a discount or at premium? iii. Relative to the pound is the 180...

Spot Question 2 Given below are spot and forward rates expressed in US dollars per unit of the Euro and £ Rates 1.5393 1.6030 30 days forward 1.5406 1.6006 60 days forward 1.5425 1.6000 90 days 1.5431 1.5945 180 days 1.5478 1.5859 Required: i. Is the 90-day forward € quoted at a discount or at a premium? ii. Is the 90-day forward contract in pound trading at a discount or at premium? iii. Relative to the pound is the 180...

Table 11.4. Forward Exchange Rates Switzerland (Franc) 30-day Forward 90-day Forward 180-day Forward U.S. Dollar Equivalent...

Table 11.4. Forward Exchange Rates Switzerland (Franc) 30-day Forward 90-day Forward 180-day Forward U.S. Dollar Equivalent Wednesday Tuesday .6598 .6590 .6592 .6585 .6585 .6578 .6577 .6572 10. Consider Table 11.4. If one were to buy francs for immediate delivery, on Tuesday the dollar cost of each franc would be: a. $0.6598 b. $1.5156 c. $0.6590 d. $1.5175 11. Consider Table 11.4. If one were to buy dollars for immediate delivery, on Tuesday the franc cost of each dollar would be:...

Table 11.4. Forward Exchange Rates Switzerland (Franc) 30-day Forward 90-day Forward 180-day Forward U.S. Dollar Equivalent Wednesday Tuesday .6598 .6590 .6592 .6585 .6585 .6578 .6577 .6572 10. Consider Table 11.4. If one were to buy francs for immediate delivery, on Tuesday the dollar cost of each franc would be: a. $0.6598 b. $1.5156 c. $0.6590 d. $1.5175 11. Consider Table 11.4. If one were to buy dollars for immediate delivery, on Tuesday the franc cost of each dollar would be:...

If the spot rate of the British pound is $2.2, and the 180-day forward rate is...

If the spot rate of the British pound is $2.2, and the 180-day forward rate is $2.25, what is the annualized premium or discount? (1pt) 3.

If the spot rate of the British pound is $2.2, and the 180-day forward rate is $2.25, what is the annualized premium or discount? (1pt) 3.

The SF/$ spot exchange rate is SF1.26/$ and the 180-day forward exchange rate is SF1.32/$. What...

The SF/$ spot exchange rate is SF1.26/$ and the 180-day forward exchange rate is SF1.32/$. What is the forward premium or discount? If you are a Switzerland based exporter expecting $500,000 dollar receivables in 6 months, would you hedge your dollar receivables using a forward contract? How?

180-day U.S. interest rate 180-day Fijian interest rate 180-day forward rate of Fijian dollar (F$) Spot...

180-day U.S. interest rate 180-day Fijian interest rate 180-day forward rate of Fijian dollar (F$) Spot rate of Fijian dollar Expected spot rate of Fijian dollar in 90 days 49% 596 $0.49 $0.48 $0.47 Assume that Monte Christo Corporation in the U.S. will receive 500,000 Fijian dollars in 180 days. What is value of the receivable if Monte Christo implements a forward hedge? a. $240,000 b. $245,000 c. $235,000 d. None of these choices are correct.

180-day U.S. interest rate 180-day Fijian interest rate 180-day forward rate of Fijian dollar (F$) Spot rate of Fijian dollar Expected spot rate of Fijian dollar in 90 days 49% 596 $0.49 $0.48 $0.47 Assume that Monte Christo Corporation in the U.S. will receive 500,000 Fijian dollars in 180 days. What is value of the receivable if Monte Christo implements a forward hedge? a. $240,000 b. $245,000 c. $235,000 d. None of these choices are correct.

The spot and 90‑day forward rates for the euro are $1.3320/€ and $1.3402/€, respectively. The euro...

The spot and 90‑day forward rates for the euro are $1.3320/€ and $1.3402/€, respectively. The euro is said to be selling at a forward__________ (annualized %). a. Premium 1.4% b. Premium 2.46% c. Discount 1.4% d. Discount 2.46%

The spot and 30-day forward rates for the Swiss franc are $0.9075 and $0.9120 respectively. The...

The spot and 30-day forward rates for the Swiss franc are $0.9075 and $0.9120 respectively. The Swiss franc is said to be selling at an annualized forward ______

The spot rate on the London market is £0.5500/$, while the 90-day forward rate is £0.5579/$....

The spot rate on the London market is £0.5500/$, while the 90-day forward rate is £0.5579/$. What is the annualized forward premium or discount on the British pound? (Round answer to 2 decimal places, e.g. 17.54%. Use 360 days for calculation.) Please write out the equation. I am trying to teach myself.

Spot Question 2 Given below are spot and forward rates expressed in US dollars per unit of the Euro and £ Rates 1.5393 1.6030 30 days forward 1.5406 1.6006 60 days forward 1.5425 1.6000 90 days 1.5431 1.5945 180 days 1.5478 1.5859 Required: i. Is the 90-day forward € quoted at a discount or at a premium? ii. Is the 90-day forward contract in pound trading at a discount or at premium? iii. Relative to the pound is the 180...

Spot Question 2 Given below are spot and forward rates expressed in US dollars per unit of the Euro and £ Rates 1.5393 1.6030 30 days forward 1.5406 1.6006 60 days forward 1.5425 1.6000 90 days 1.5431 1.5945 180 days 1.5478 1.5859 Required: i. Is the 90-day forward € quoted at a discount or at a premium? ii. Is the 90-day forward contract in pound trading at a discount or at premium? iii. Relative to the pound is the 180...

Table 11.4. Forward Exchange Rates Switzerland (Franc) 30-day Forward 90-day Forward 180-day Forward U.S. Dollar Equivalent Wednesday Tuesday .6598 .6590 .6592 .6585 .6585 .6578 .6577 .6572 10. Consider Table 11.4. If one were to buy francs for immediate delivery, on Tuesday the dollar cost of each franc would be: a. $0.6598 b. $1.5156 c. $0.6590 d. $1.5175 11. Consider Table 11.4. If one were to buy dollars for immediate delivery, on Tuesday the franc cost of each dollar would be:...

Table 11.4. Forward Exchange Rates Switzerland (Franc) 30-day Forward 90-day Forward 180-day Forward U.S. Dollar Equivalent Wednesday Tuesday .6598 .6590 .6592 .6585 .6585 .6578 .6577 .6572 10. Consider Table 11.4. If one were to buy francs for immediate delivery, on Tuesday the dollar cost of each franc would be: a. $0.6598 b. $1.5156 c. $0.6590 d. $1.5175 11. Consider Table 11.4. If one were to buy dollars for immediate delivery, on Tuesday the franc cost of each dollar would be:...

If the spot rate of the British pound is $2.2, and the 180-day forward rate is $2.25, what is the annualized premium or discount? (1pt) 3.

If the spot rate of the British pound is $2.2, and the 180-day forward rate is $2.25, what is the annualized premium or discount? (1pt) 3.

180-day U.S. interest rate 180-day Fijian interest rate 180-day forward rate of Fijian dollar (F$) Spot rate of Fijian dollar Expected spot rate of Fijian dollar in 90 days 49% 596 $0.49 $0.48 $0.47 Assume that Monte Christo Corporation in the U.S. will receive 500,000 Fijian dollars in 180 days. What is value of the receivable if Monte Christo implements a forward hedge? a. $240,000 b. $245,000 c. $235,000 d. None of these choices are correct.

180-day U.S. interest rate 180-day Fijian interest rate 180-day forward rate of Fijian dollar (F$) Spot rate of Fijian dollar Expected spot rate of Fijian dollar in 90 days 49% 596 $0.49 $0.48 $0.47 Assume that Monte Christo Corporation in the U.S. will receive 500,000 Fijian dollars in 180 days. What is value of the receivable if Monte Christo implements a forward hedge? a. $240,000 b. $245,000 c. $235,000 d. None of these choices are correct.

Most questions answered within 3 hours.

-

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 12 seconds from now -

Why are polymers not typically casted into products?

asked 16 minutes ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 33 minutes ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 22 minutes ago -

1.

You need to prepare 10.0 liters of an acid aqueous solution with a

pH of...

asked 25 minutes ago -

Along an aggregate supply curve, if the level of output is less

than the natural level...

asked 25 minutes ago -

By 2025, annual consumption in emerging markets will total $30

trillion and contribute more than ________...

asked 30 minutes ago -

At what point does reformation cease to be a viable option for

those who are oppressed...

asked 34 minutes ago -

Place letters corresponding to amounts in the proper order for

lightest to heaviest samples:

a) 2100...

asked 38 minutes ago -

Consider the multicore processor with 6 heterogeneous cores

labelled C1, C2, C3, C4, C5, and C6....

asked 41 minutes ago -

Document system components according to standards and procedures

(Implement and hand over system components) IT administrative

asked 41 minutes ago -

The college asked 700 students if they wanted a longer spring

break and 600 students said...

asked 41 minutes ago