Homework Answers

(1)

| Sl.No | Year | Cashflow | Discounting@4% | Discounted Cash Flow |

| 1 | Jan1,2013 | $720000 | 1 | $720000 |

| 2 | Dec31,2013 | ($27650) | 0.9615 | ($26585.475) |

| 3 | Dec31,2014 | ($27650) | 0.9245 | ($25562.425) |

| 4 | Dec31,2015 | ($817650) | 0.8889 | ($726809.085) |

Here the discounting rate is taken as 4% as it is given that the present rate of interest provided to the bond holders is 4%.So the required rate of return to the bond holder will be 4% as he would expect atleast 4% return on his investment.

The Total of Sl.No. 2 to 5 is $77897, which shows a difference of $84.015 due to rounding off error of Discounting Factor.To remove this round off error it is advisable to not round off the decimal places, then the value would be $779041

(2)

| Date | Particulars | LFno. | Debit | Credit |

| Jan1,2013 |

*Cash A/c Dr **Discount on 3.5% Bonds Dr To 3.5% Bonds (Being Bonds issued) |

$779041 $10959 |

$720000 |

*As the Interest rate is 4% prevailing in the market after issuing bonds it will not fetch the entity its face value.

** $720000-$779041=$10959 will be the discount offered.

(3)

| Date | Particulars | LFno. | Debit | Credit |

| Dec31,2013 |

*Interest Expense a/c Dr To Bank A/c To 3.5% Bonds a/c (Being Interest expense recognised) |

$31600 |

$27650 $3950 |

* As the Entity follows Effective Interest Bond Amortization Method

Interest as on Dec, is $790000*4%=$31600

3.5% Bond Value = $790000+31600-27650=$793950

Actual Interest Payment is $790000*3.5%=$27650

| Date | Particulars | LFno. | Debit | Credit |

| Dec31,2014 |

*Interest Expense a/c Dr To Bank A/c To 3.5% Bonds a/c (Being Interest expense recognised) |

$31758 |

$27650 $4108 |

* As the Entity follows Effective Interest Bond Amortization Method

Interest as on Dec, is $793950*4%=$31758

3.5% Bond Value = $793950+31758-27650=$798058

Actual Interest Payment is $790000*3.5%=$27650

(4)

| Date | Particulars | LFno. | Debit | Credit |

| Dec31,2015 |

*Interest Expense a/c Dr To Bank A/c To 3.5% Bonds a/c (Being Interest expense recognised) |

$31922 |

$27650 $4272 |

* As the Entity follows Effective Interest Bond Amortization Method

Interest as on Dec, is $798058*4%=$31922

3.5% Bond Value = $798058+31922-27650=$802330

Actual Interest Payment is $790000*3.5%=$27650

| Date | Particulars | LFno. | Debit | Credit |

| Dec31,2015 |

3.5% Bonds A/c Dr To Cash a/c To Discount on Bonds a/c To loss on redemption a/c (Being redemption made) |

$802330 |

$790000 $10959 $1371 |

It is assumed that the redemption is made at Face value of the Bonds.

Alternatively Discount on Bonds could be written off on the life of the bond.

Add Answer to:

Hi could someone help me do what is wrong and explain me the

debits and credits...

On January 1, 2013, Surreal Manufacturing issued 780 bonds, each with a face value of $1,000,...

On January 1, 2013, Surreal Manufacturing issued 780 bonds, each with a face value of $1,000, a stated interest rate of 3.75 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $774,591. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

On January 1, 2013, Surreal Manufacturing issued 780 bonds, each with a face value of $1,000, a stated interest rate of 3.75 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $774,591. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

10.00 points On January 1, 2013, Surreal Manufacturing issued 790 bonds, each with a face value...

10.00 points On January 1, 2013, Surreal Manufacturing issued 790 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $779,041. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest...

10.00 points On January 1, 2013, Surreal Manufacturing issued 790 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $779,041. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest...

On January 1, 2013, Surreal Manufacturing issued 630 bonds, each with a face value of $1,000,...

On January 1, 2013, Surreal Manufacturing issued 630 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $670,567. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

On January 1, 2013, Surreal Manufacturing issued 630 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $670,567. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

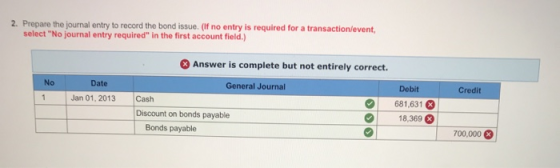

On January 1, 2013, Loop de Loop Raceway issued 700 bonds, each with a face value...

On January 1, 2013, Loop de Loop Raceway issued 700 bonds, each with a face value of $1,000, a stated interest rate of 6 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 7 percent, so the total proceeds from the bond issue were $681,631. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 700 bonds, each with a face value of $1,000, a stated interest rate of 6 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 7 percent, so the total proceeds from the bond issue were $681,631. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 550 bonds, each with a face value...

On January 1, 2013, Loop de Loop Raceway issued 550 bonds, each with a face value of $1,000, a stated interest rate of 5 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 6 percent, so the total proceeds from the bond issue were $535,288. Loop de Loop uses the straight-line bond amortization method Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 550 bonds, each with a face value of $1,000, a stated interest rate of 5 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 6 percent, so the total proceeds from the bond issue were $535,288. Loop de Loop uses the straight-line bond amortization method Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 680 bonds, each with a face value...

On January 1, 2013, Loop de Loop Raceway issued 680 bonds, each with a face value of $1,000, a stated interest rate of 7 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 8 percent, so the total proceeds from the bond issue were $662,454. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 680 bonds, each with a face value of $1,000, a stated interest rate of 7 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 8 percent, so the total proceeds from the bond issue were $662,454. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

What would be the journal entries along with debits/credits for -bond issue on January 01, 2021...

What would be the journal entries along with debits/credits

for

-bond issue on January 01, 2021

-the first semiannual interest payment on June 30, 2021

-the second semiannual interest payment on December 31, 2021

Required information [The following information applies to the questions displayed below.] On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $480,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each...

What would be the journal entries along with debits/credits

for

-bond issue on January 01, 2021

-the first semiannual interest payment on June 30, 2021

-the second semiannual interest payment on December 31, 2021

Required information [The following information applies to the questions displayed below.] On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $480,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each...

Serotta Corporation is planning to issue bonds with a face value of $340,000 and a coupon rate of...

Serotta Corporation is planning to issue bonds with a face value of $340,000 and a coupon rate of 8 percent. The bonds mature in two years and pay interest quarterly every March 31, June 30, September 30, and December 31. All of the bonds were sold on January 1 of this year. Serotta uses the effective-interest amortization method and also uses a premium account. Assume an annual market rate of interest of 4 percent (FV of $1, PV of S1,...

Serotta Corporation is planning to issue bonds with a face value of $340,000 and a coupon rate of 8 percent. The bonds mature in two years and pay interest quarterly every March 31, June 30, September 30, and December 31. All of the bonds were sold on January 1 of this year. Serotta uses the effective-interest amortization method and also uses a premium account. Assume an annual market rate of interest of 4 percent (FV of $1, PV of S1,...

Can anyone help me? I can't figure this out or the next problem. Please show work...

Can anyone help me? I can't figure this out or the next

problem. Please show work :)

On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $590,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each year. 2. If the market interest rate is 9%, the bonds will issue at $541,948. Record the bond issue on January 1, 2021, and the first two semiannual...

Can anyone help me? I can't figure this out or the next

problem. Please show work :)

On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $590,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each year. 2. If the market interest rate is 9%, the bonds will issue at $541,948. Record the bond issue on January 1, 2021, and the first two semiannual...

Pretzelmania, Inc., issues 5%, 20-year bonds with a face amount of $53,000 for $46,875 on January...

Pretzelmania, Inc., issues 5%, 20-year bonds with a face amount of $53,000 for $46,875 on January 1, 2021. The market interest rate for bonds of similar risk and maturity is 6%. Interest is paid semiannually on June 30 and December 31. Required: 1. & 2. Record the bond issue and first interest payment on June 30, 2021. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Round your intermediate computations...

Pretzelmania, Inc., issues 5%, 20-year bonds with a face amount of $53,000 for $46,875 on January 1, 2021. The market interest rate for bonds of similar risk and maturity is 6%. Interest is paid semiannually on June 30 and December 31. Required: 1. & 2. Record the bond issue and first interest payment on June 30, 2021. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Round your intermediate computations...

On January 1, 2013, Surreal Manufacturing issued 780 bonds, each with a face value of $1,000, a stated interest rate of 3.75 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $774,591. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

On January 1, 2013, Surreal Manufacturing issued 780 bonds, each with a face value of $1,000, a stated interest rate of 3.75 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $774,591. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

10.00 points On January 1, 2013, Surreal Manufacturing issued 790 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $779,041. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest...

10.00 points On January 1, 2013, Surreal Manufacturing issued 790 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $779,041. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest...

On January 1, 2013, Surreal Manufacturing issued 630 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $670,567. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

On January 1, 2013, Surreal Manufacturing issued 630 bonds, each with a face value of $1,000, a stated interest rate of 3.50 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 4.00 percent, so the total proceeds from the bond issue were $670,567. Surreal uses the effective-interest bond amortization method. Required: 1. Prepare a bond amortization schedule. (Round your final answers to the nearest whole dollar.)...

On January 1, 2013, Loop de Loop Raceway issued 700 bonds, each with a face value of $1,000, a stated interest rate of 6 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 7 percent, so the total proceeds from the bond issue were $681,631. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 700 bonds, each with a face value of $1,000, a stated interest rate of 6 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 7 percent, so the total proceeds from the bond issue were $681,631. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 550 bonds, each with a face value of $1,000, a stated interest rate of 5 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 6 percent, so the total proceeds from the bond issue were $535,288. Loop de Loop uses the straight-line bond amortization method Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 550 bonds, each with a face value of $1,000, a stated interest rate of 5 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 6 percent, so the total proceeds from the bond issue were $535,288. Loop de Loop uses the straight-line bond amortization method Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 680 bonds, each with a face value of $1,000, a stated interest rate of 7 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 8 percent, so the total proceeds from the bond issue were $662,454. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

On January 1, 2013, Loop de Loop Raceway issued 680 bonds, each with a face value of $1,000, a stated interest rate of 7 percent paid annually on December 31, and a maturity date of December 31, 2015. On the issue date, the market interest rate was 8 percent, so the total proceeds from the bond issue were $662,454. Loop de Loop uses the straight-line bond amortization method. Required: 1. Prepare a bond amortization schedule. Changes During the Period Period...

What would be the journal entries along with debits/credits

for

-bond issue on January 01, 2021

-the first semiannual interest payment on June 30, 2021

-the second semiannual interest payment on December 31, 2021

Required information [The following information applies to the questions displayed below.] On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $480,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each...

What would be the journal entries along with debits/credits

for

-bond issue on January 01, 2021

-the first semiannual interest payment on June 30, 2021

-the second semiannual interest payment on December 31, 2021

Required information [The following information applies to the questions displayed below.] On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $480,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each...

Serotta Corporation is planning to issue bonds with a face value of $340,000 and a coupon rate of 8 percent. The bonds mature in two years and pay interest quarterly every March 31, June 30, September 30, and December 31. All of the bonds were sold on January 1 of this year. Serotta uses the effective-interest amortization method and also uses a premium account. Assume an annual market rate of interest of 4 percent (FV of $1, PV of S1,...

Serotta Corporation is planning to issue bonds with a face value of $340,000 and a coupon rate of 8 percent. The bonds mature in two years and pay interest quarterly every March 31, June 30, September 30, and December 31. All of the bonds were sold on January 1 of this year. Serotta uses the effective-interest amortization method and also uses a premium account. Assume an annual market rate of interest of 4 percent (FV of $1, PV of S1,...

Can anyone help me? I can't figure this out or the next

problem. Please show work :)

On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $590,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each year. 2. If the market interest rate is 9%, the bonds will issue at $541,948. Record the bond issue on January 1, 2021, and the first two semiannual...

Can anyone help me? I can't figure this out or the next

problem. Please show work :)

On January 1, 2021, Twister Enterprises, a manufacturer of a variety of transportable spin rides, issues $590,000 of 8% bonds, due in 15 years, with interest payable semiannually on June 30 and December 31 each year. 2. If the market interest rate is 9%, the bonds will issue at $541,948. Record the bond issue on January 1, 2021, and the first two semiannual...

Pretzelmania, Inc., issues 5%, 20-year bonds with a face amount of $53,000 for $46,875 on January 1, 2021. The market interest rate for bonds of similar risk and maturity is 6%. Interest is paid semiannually on June 30 and December 31. Required: 1. & 2. Record the bond issue and first interest payment on June 30, 2021. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Round your intermediate computations...

Pretzelmania, Inc., issues 5%, 20-year bonds with a face amount of $53,000 for $46,875 on January 1, 2021. The market interest rate for bonds of similar risk and maturity is 6%. Interest is paid semiannually on June 30 and December 31. Required: 1. & 2. Record the bond issue and first interest payment on June 30, 2021. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Round your intermediate computations...

Most questions answered within 3 hours.

-

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 37 minutes ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 28 minutes ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 34 minutes ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 1 hour ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 1 hour ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 1 hour ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 1 hour ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 1 hour ago -

Why are polymers not typically casted into products?

asked 2 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 2 hours ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 2 hours ago -

1.

You need to prepare 10.0 liters of an acid aqueous solution with a

pH of...

asked 2 hours ago