ABC Company produces three products in a joint production process. At the split-off point, all three...

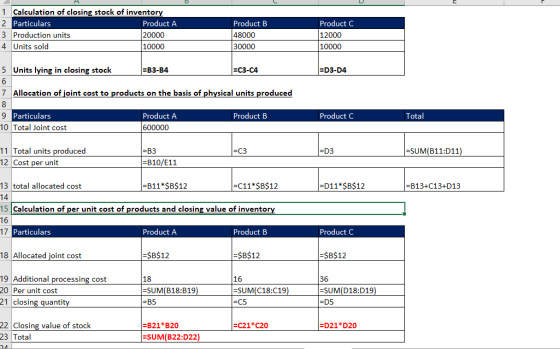

ABC Company produces three products in a joint production process. At the split-off point, all three products are produced further and then sold. Information about these products for 2019, the most recent year, appears below: Product A Product B Product C Units produced ............... 20,000 48,000 12,000 Selling price ................ $41 per unit $50 per unit $65 per unit Additional processing costs .. $18 per unit $16 per unit $36 per unit Joint costs for 2019 totaled $600,000. During 2019, ABC Company sold 10,000 units of Product A; 30,000 units of Product B were sold; and 10,000 units of Product C were sold. Assume there were no beginning inventories of any type in 2019. ABC Company employs the physical units method to allocate joint costs to products.

Calculate the dollar amount of finished goods inventory that ABC Company would report in its December 31, 2019 balance sheet.

Homework Answers

with show formula

Add Answer to:

ABC Company produces three products in a joint production

process. At the split-off point, all three...

XYZ Company makes two products, W and P, in a joint process. At the split-off point,...

XYZ Company makes two products, W and P, in a joint process. At the split-off point, 60,000 units of Product W and 50,000 units of Product P are available each month. Monthly joint production costs total $120,000 and are allocated to the two products equally. Product W can either be sold at the split-off point for $5.60 per unit or it can be processed further and then sold for $8.80 per unit. If Product W is processed further, addi tional...

XYZ Company makes two products, W and P, in a joint process. At the split-off point, 60,000 units of Product W and 50,000 units of Product P are available each month. Monthly joint production costs total $120,000 and are allocated to the two products equally. Product W can either be sold at the split-off point for $5.60 per unit or it can be processed further and then sold for $8.80 per unit. If Product W is processed further, addi tional...

SELL AT SPLIT – OFF POINT OR PROCESS FURTHER & JOINT COST ALLOCATION Lauricella Inc. produces...

SELL AT SPLIT – OFF POINT OR PROCESS FURTHER & JOINT COST ALLOCATION Lauricella Inc. produces three products from a common set of inputs for $95,000. Other sales and cost data follow: Unit Sales Price ____ Costs After At After further Split-off Product Quantity Split-off Processing Point__ Regular 8,000 $ 8 $ 10 $ 10,000 Special 5,000 5 8 15,000 Premium 4,000 6 10 20,000 REQUIRED: Which products should...

A company manufactures three products using the same production process. The costs incurred up to the split-off point ar...

A company manufactures three products using the same production

process. The costs incurred up to the split-off point are $190,500.

These costs are allocated to the products on the basis of their

sales value at the split-off point. The number of units produced,

the selling prices per unit of the three products at the split-off

point and after further processing, and the additional processing

costs are as follows.

Product

Number

of

Units Produced

Selling

Price

at Split-Off

Selling

Price

after...

A company manufactures three products using the same production

process. The costs incurred up to the split-off point are $190,500.

These costs are allocated to the products on the basis of their

sales value at the split-off point. The number of units produced,

the selling prices per unit of the three products at the split-off

point and after further processing, and the additional processing

costs are as follows.

Product

Number

of

Units Produced

Selling

Price

at Split-Off

Selling

Price

after...

Benjamin Company produces products C, J, and R from a joint production process. Each product may...

Benjamin Company produces products C, J, and R from a joint production process. Each product may be sold at the split-off point or processed further. Joint production costs of $95,000 per year are allocated to the products based on the relative number of units produced. Data for Benjamin's operations for last year follow: Units Produced Sales Values at Split-Off Sales Values If Processed Further Costs of Processing Further Product C 6,000 $75,000 $100,000 $20,000 Product J 9,000 $70,000 $115,000 $36,000...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

The Marshall Company has a joint production process that produces two joint products and a by-product....

The Marshall Company has a joint production process that

produces two joint products and a by-product. The joint products

are Ying and Yang, and the by-product is Bit. Marshall accounts for

the costs of its products using the net realizable value method.

The two joint products are processed beyond the split-off point,

incurring separable processing costs. There is a $2,000 disposal

cost for the by-product. A summary of a recent month’s activity at

Marshall is shown below: Ying Yang Bit...

The Marshall Company has a joint production process that

produces two joint products and a by-product. The joint products

are Ying and Yang, and the by-product is Bit. Marshall accounts for

the costs of its products using the net realizable value method.

The two joint products are processed beyond the split-off point,

incurring separable processing costs. There is a $2,000 disposal

cost for the by-product. A summary of a recent month’s activity at

Marshall is shown below: Ying Yang Bit...

Net Realizable Value Method, Decision to Sell at Split-off or Process Further Pacheco, Inc., produces two...

Net Realizable Value Method, Decision to Sell at Split-off or Process Further Pacheco, Inc., produces two products, overs and unders, in a single process. The joint costs of this process were $50,000, and 14,000 units of overs and 35,000 units of unders were produced. Separable processing costs beyond the split-off point were as follows: overs, $18,000; unders, $19,900. Overs sell for $2.00 per unit; unders sell for $3.14 per unit. Required: 1. Allocate the $50,000 joint costs using the estimated...

Net Realizable Value Method, Decision to Sell at Split-off or Process Further Pacheco, Inc., produces two...

Net Realizable Value Method, Decision to Sell at Split-off or Process Further Pacheco, Inc., produces two products, overs and unders, in a single process. The joint costs of this process were $50,000, and 15,000 units of overs and 35,000 units of unders were produced. Separable processing costs beyond the split-off point were as follows: overs, $20,000; unders, $19,900. Overs sell for $2.00 per unit; unders sell for $3.14 per unit. Required: 1. Allocate the $50,000 joint costs using the estimated...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

The Marshall Company has a joint production process that produces two joint products and a by-product....

The Marshall Company has a joint production process that produces two joint products and a by-product. The joint products are Ying and Yang, and the by-product is Bit. Marshall accounts for the costs of its products using the net realizable value method. The two joint products are processed beyond the split-off point, incurring separable processing costs. There is a $300 disposal cost for the by- product. A summary of a recent month's activity at Marshall is shown below: Units sold...

The Marshall Company has a joint production process that produces two joint products and a by-product. The joint products are Ying and Yang, and the by-product is Bit. Marshall accounts for the costs of its products using the net realizable value method. The two joint products are processed beyond the split-off point, incurring separable processing costs. There is a $300 disposal cost for the by- product. A summary of a recent month's activity at Marshall is shown below: Units sold...

XYZ Company makes two products, W and P, in a joint process. At the split-off point, 60,000 units of Product W and 50,000 units of Product P are available each month. Monthly joint production costs total $120,000 and are allocated to the two products equally. Product W can either be sold at the split-off point for $5.60 per unit or it can be processed further and then sold for $8.80 per unit. If Product W is processed further, addi tional...

XYZ Company makes two products, W and P, in a joint process. At the split-off point, 60,000 units of Product W and 50,000 units of Product P are available each month. Monthly joint production costs total $120,000 and are allocated to the two products equally. Product W can either be sold at the split-off point for $5.60 per unit or it can be processed further and then sold for $8.80 per unit. If Product W is processed further, addi tional...

A company manufactures three products using the same production

process. The costs incurred up to the split-off point are $190,500.

These costs are allocated to the products on the basis of their

sales value at the split-off point. The number of units produced,

the selling prices per unit of the three products at the split-off

point and after further processing, and the additional processing

costs are as follows.

Product

Number

of

Units Produced

Selling

Price

at Split-Off

Selling

Price

after...

A company manufactures three products using the same production

process. The costs incurred up to the split-off point are $190,500.

These costs are allocated to the products on the basis of their

sales value at the split-off point. The number of units produced,

the selling prices per unit of the three products at the split-off

point and after further processing, and the additional processing

costs are as follows.

Product

Number

of

Units Produced

Selling

Price

at Split-Off

Selling

Price

after...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

The Marshall Company has a joint production process that

produces two joint products and a by-product. The joint products

are Ying and Yang, and the by-product is Bit. Marshall accounts for

the costs of its products using the net realizable value method.

The two joint products are processed beyond the split-off point,

incurring separable processing costs. There is a $2,000 disposal

cost for the by-product. A summary of a recent month’s activity at

Marshall is shown below: Ying Yang Bit...

The Marshall Company has a joint production process that

produces two joint products and a by-product. The joint products

are Ying and Yang, and the by-product is Bit. Marshall accounts for

the costs of its products using the net realizable value method.

The two joint products are processed beyond the split-off point,

incurring separable processing costs. There is a $2,000 disposal

cost for the by-product. A summary of a recent month’s activity at

Marshall is shown below: Ying Yang Bit...

The Marshall Company has a joint production process that produces two joint products and a by-product. The joint products are Ying and Yang, and the by-product is Bit. Marshall accounts for the costs of its products using the net realizable value method. The two joint products are processed beyond the split-off point, incurring separable processing costs. There is a $300 disposal cost for the by- product. A summary of a recent month's activity at Marshall is shown below: Units sold...

The Marshall Company has a joint production process that produces two joint products and a by-product. The joint products are Ying and Yang, and the by-product is Bit. Marshall accounts for the costs of its products using the net realizable value method. The two joint products are processed beyond the split-off point, incurring separable processing costs. There is a $300 disposal cost for the by- product. A summary of a recent month's activity at Marshall is shown below: Units sold...

Most questions answered within 3 hours.

-

Why is QE a controversial monetary policy tool.

A. It may lead to excessive inflation.B. By...

asked 4 minutes ago -

A finite potential well has depth U0 = 2.78 eV . What is the

penetration distance...

asked 29 minutes ago -

1. The bus bars of a power station are in two sections A and B

separated...

asked 28 minutes ago -

Fiscal policy is the deliberate manipulation of taxes and

government spending to alter GDP, employment, inflation...

asked 1 hour ago -

evaluating an expression using only one digit and + and - as

operators ....3+5-1+7-5+8

-----------------------

stack...

asked 1 hour ago -

Two concentric current loops lie in the same plane. The smaller

loop has a radius of...

asked 1 hour ago -

1)Which of the following is an

important difference between qualified and nonqualified retirement

plans?

a. Qualified...

asked 2 hours ago -

What's the streaming business's problem on the

horizon?

asked 3 hours ago -

I need help with writing the conclusion for this online lab

report

Abstract

By testing the...

asked 3 hours ago -

For the reaction 1N2+3H2-----> 2NH3, would the reaction rate

trend be: delta[NH3]/ delta t = -2...

asked 3 hours ago -

Within your current/past organization, identify a problem/issue

and format a design to address same. You may...

asked 3 hours ago -

A sock stuck to the side of a clothes-dryer barrel has a

centripetal acceleration of 24...

asked 4 hours ago