Antuan Company set the following standard costs for one unit of its product.

| Direct materials (3.0 Ibs. @ $5.00 per Ib.) | $ | 15.00 |

| Direct labor (2.0 hrs. @ $13.00 per hr.) | 26.00 | |

| Overhead (2.0 hrs. @ $18.50 per hr.) | 37.00 | |

| Total standard cost | $ | 78.00 |

The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory’s capacity of 20,000 units per month. Following are the company’s budgeted overhead costs per month at the 75% capacity level.

| Overhead Budget (75% Capacity) | |||||

| Variable overhead costs | |||||

| Indirect materials | $ | 15,000 | |||

| Indirect labor | 75,000 | ||||

| Power |

15,000 |

||||

| Repairs and maintenance | 30,000 | ||||

| Total variable overhead costs | $ | 135,000 | |||

| Fixed overhead costs | |||||

| Depreciation—Building | 25,000 | ||||

| Depreciation—Machinery | 70,000 | ||||

| Taxes and insurance | 17,000 | ||||

| Supervision | 308,000 | ||||

| Total fixed overhead costs | 420,000 | ||||

The company incurred the following actual costs when it operated at 75% of capacity in October.

| Direct materials (46,000 Ibs. @ $5.20 per lb.) | $ | 239,200 | |||

| Direct labor (21,000 hrs. @ $13.40 per hr.) | 281,400 | ||||

| Overhead costs | |||||

| Indirect materials | $ | 41,400 | |||

| Indirect labor | 176,600 | ||||

| Power | 17,250 | ||||

| Repairs and maintenance | 34,500 | ||||

| Depreciation—Building | 25,000 | ||||

| Depreciation—Machinery | 94,500 | ||||

| Taxes and insurance | 15,300 | ||||

| Supervision | 308,000 | 712,550 | |||

| Total costs | $ | 1,233,150 |

Required:

1&2. Prepare flexible overhead budgets for

October showing the amounts of each variable and fixed cost at the

65%, 75%, and 85% capacity levels and classify all items listed in

the fixed budget as variable or fixed.

3. Compute the direct materials cost variance, including its price and quantity variances. (Indicate the effect of each variance by selecting for favorable, unfavorable, and No variance.)

4. Compute the direct labor cost variance,

including its rate and efficiency variances. (Indicate the

effect of each variance by selecting for favorable, unfavorable,

and No variance. Round "Rate per hour" answers to two decimal

places.)

5. Prepare a detailed overhead variance report that shows the variances for individual items of overhead. (Indicate the effect of each variance by selecting for favorable, unfavorable, and No variance.)

Homework Answers

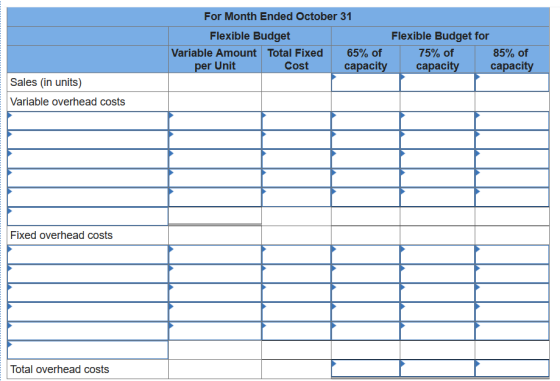

1&2.

| Flexible Budget | Flexible Budget For | ||||

| Variable amount per unit | Total Fixed cost | 65% of capacity | 75% of capacity | 85% of capacity | |

| Sales in units | 13,000 | 15,000 | 17,000 | ||

| Variable overhead cost: | |||||

| Indirect material ($15,000/15,000)=$1 | $1 | $13,000 | $15,000 | $17,000 | |

| Indirect labor (75,000/15,000)=$5 | 5 | 65,000 | 75,000 | 85,000 | |

| Power (15,000/15,000)=$1 | 1 | 13,000 | 15,000 | 17,000 | |

| Repairs and maintenance (30,000/15,000)=$2 | 2 | 26,000 | 30,000 | 34,000 | |

| Total variable overhead cost | 9 | 117,000 | 135,000 | 153,000 | |

| Fixed overhead cost: | |||||

| Depreciation-Building | $25,000 | 25,000 | 25,000 | 25,000 | |

| Depreciation-Machinery | 70,000 | 70,000 | 70,000 | 70,000 | |

| Taxes and insurance | 17,000 | 17,000 | 17,000 | 17,000 | |

| Supervision | 308,000 | 308,000 | 308,000 | 308,000 | |

| Total fixed overhead cost | 420,000 | 420,000 | 420,000 | 420,000 | |

| Total overhead costs | $537,000 | $555,000 | $573,000 | ||

3.

| Actual cost | Standard cost | |||||||||

| Actual quantity | Actual price | Actual quantity | Standard price | Standard quantity | Standard price | |||||

| 46,000 | $5.20 | 46,000 | $5 | 45,000 (15,000*3) | $5 | |||||

| $239,200 | $230,000 | $225,000 | ||||||||

| $9,200 U | $5,000 U | |||||||||

| Direct material price variance = $9,200 Unfavorable | ||||||||||

| Direct material quantity variance = $5,000 Unfavorable | ||||||||||

| Total direct material cost variance = $14,200 Unfavorable | ||||||||||

4.

| Actual cost | Standard cost | |||||||||

| Actual hours | Actual rate | Actual hours | Standard rate | Standard hours | Standard rate | |||||

| 21,000 | $13.40 | 21,000 | $13 | 30,000 (15,000*2) | $13 | |||||

| $281,400 | $273,000 | $390,000 | ||||||||

| $8,400 U | $117,000 F | |||||||||

| Direct labor rate variance = $8,400 Unfavorable | ||||||||||

| Direct labor efficiency variance = $117,000 Favorable | ||||||||||

| Total direct labor cost variance = $108,600 Favorable | ||||||||||

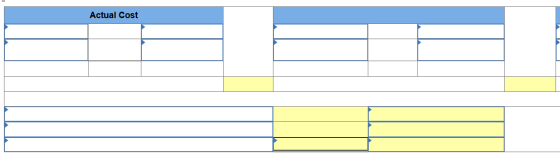

5.

| Overhead Variance Report | ||||

| Expected production volume | 75% of capacity | |||

| Production level achieved | 75% of capacity | |||

| Volume variance | No variance | |||

| Flexible Budget | Actual Results | Variances | Fav./Unfav. | |

| Variable costs: | ||||

| Indirect material | $15,000 | $41,400 | $26,400 | Unfavorable |

| Indirect labor | 75,000 | 176,600 | 101,600 | Unfavorable |

| Power | 15,000 | 17,250 | 2,250 | Unfavorable |

| Repairs and maintenance | 30,000 | 34,500 | 4,500 | Unfavorable |

| Total variable costs | 135,000 | 269,750 | 134,750 | Unfavorable |

| Fixed costs | ||||

| Depreciation-Building | 25,000 | 25,000 | 0 | No variance |

| Depreciation-Machinery | 70,000 | 94,500 | 24,500 | Unfavorable |

| Taxes and insurance | 17,000 | 15,300 | 1,700 | Favorable |

| Supervision | 308,000 | 308,000 | 0 | No variance |

| Total fixed costs | 420,000 | 442,800 | 22,800 | Unfavorable |

| Total overhead cost | $555,000 | $712,550 | $157,550 | Unfavorable |

Add Answer to:

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (3.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (3.0 Ibs. @ $6.00 per Ib.)

$

18.00

Direct labor (1.8 hrs. @ $11.00 per hr.)

19.80

Overhead (1.8 hrs. @ $18.50 per hr.)

33.30

Total standard cost

$

71.10

The predetermined overhead rate ($18.50 per direct labor hour)

is based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (3.0 Ibs. @ $6.00 per Ib.)

$

18.00

Direct labor (1.8 hrs. @ $11.00 per hr.)

19.80

Overhead (1.8 hrs. @ $18.50 per hr.)

33.30

Total standard cost

$

71.10

The predetermined overhead rate ($18.50 per direct labor hour)

is based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (4.0 Ibs. @ $6.00 per Ib.)

$

24.00

Direct labor (1.9 hrs. @ $13.00 per hr.)

24.70

Overhead (1.9 hrs. @ $18.50 per hr.)

35.15

Total standard cost

$

83.85

The predetermined overhead rate ($18.50 per direct labor hour) is

based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (4.0 Ibs. @ $6.00 per Ib.)

$

24.00

Direct labor (1.9 hrs. @ $13.00 per hr.)

24.70

Overhead (1.9 hrs. @ $18.50 per hr.)

35.15

Total standard cost

$

83.85

The predetermined overhead rate ($18.50 per direct labor hour) is

based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib....

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $20.00 19.80 33.30 $73.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $20.00 19.80 33.30 $73.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $5.00 per Ib.) $ 15.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $ 68.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory’s capacity of 20,000 units per month. Following are the company’s budgeted overhead costs per month...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $4.00 per Ib.) Direct labor (1.7 hrs. @ $11.00 per hr.) Overhead (1.7 hrs. @ $18.50 per hr.) Total standard cost $12.00 18.70 31.45 $62.15 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $4.00 per Ib.) Direct labor (1.7 hrs. @ $11.00 per hr.) Overhead (1.7 hrs. @ $18.50 per hr.) Total standard cost $12.00 18.70 31.45 $62.15 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $6.00 per Ib.) $18.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $71.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $6.00 per Ib.) $18.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $71.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $6.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $24.00 19.80 33.30 $77.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $6.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $24.00 19.80 33.30 $77.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $5.00...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $5.00 per Ib.) $ 15.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $ 68.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory’s capacity of 20,000 units per month. Following are the company’s budgeted overhead costs per month...

Antuan Company set the following standard costs for one unit of its product Direct materials (3.0...

Antuan Company set the following standard costs for one unit of its product Direct materials (3.0 Ibs. $5.00 per Ib.) Direct labor (1.6 hrs. e $11.00 per hr.) Overhead (1.6 hrs. e $18.50 per hr.) $15.00 17.60 29.60 Total standard cost $62.20 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the 75%...

Antuan Company set the following standard costs for one unit of its product Direct materials (3.0 Ibs. $5.00 per Ib.) Direct labor (1.6 hrs. e $11.00 per hr.) Overhead (1.6 hrs. e $18.50 per hr.) $15.00 17.60 29.60 Total standard cost $62.20 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the 75%...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.6 hrs. @ $13.00 per hr.) Overhead (1.6 hrs. @ $18.50 per hr.) Total standard cost $20.00 20.80 29.60 $ 70.40 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.6 hrs. @ $13.00 per hr.) Overhead (1.6 hrs. @ $18.50 per hr.) Total standard cost $20.00 20.80 29.60 $ 70.40 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (3.0 Ibs. @ $6.00 per Ib.)

$

18.00

Direct labor (1.8 hrs. @ $11.00 per hr.)

19.80

Overhead (1.8 hrs. @ $18.50 per hr.)

33.30

Total standard cost

$

71.10

The predetermined overhead rate ($18.50 per direct labor hour)

is based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (3.0 Ibs. @ $6.00 per Ib.)

$

18.00

Direct labor (1.8 hrs. @ $11.00 per hr.)

19.80

Overhead (1.8 hrs. @ $18.50 per hr.)

33.30

Total standard cost

$

71.10

The predetermined overhead rate ($18.50 per direct labor hour)

is based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (4.0 Ibs. @ $6.00 per Ib.)

$

24.00

Direct labor (1.9 hrs. @ $13.00 per hr.)

24.70

Overhead (1.9 hrs. @ $18.50 per hr.)

35.15

Total standard cost

$

83.85

The predetermined overhead rate ($18.50 per direct labor hour) is

based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of

its product.

Direct materials (4.0 Ibs. @ $6.00 per Ib.)

$

24.00

Direct labor (1.9 hrs. @ $13.00 per hr.)

24.70

Overhead (1.9 hrs. @ $18.50 per hr.)

35.15

Total standard cost

$

83.85

The predetermined overhead rate ($18.50 per direct labor hour) is

based on an expected volume of 75% of the factory’s capacity of

20,000 units per month. Following are the company’s budgeted

overhead costs per month...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $20.00 19.80 33.30 $73.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $20.00 19.80 33.30 $73.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $4.00 per Ib.) Direct labor (1.7 hrs. @ $11.00 per hr.) Overhead (1.7 hrs. @ $18.50 per hr.) Total standard cost $12.00 18.70 31.45 $62.15 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $4.00 per Ib.) Direct labor (1.7 hrs. @ $11.00 per hr.) Overhead (1.7 hrs. @ $18.50 per hr.) Total standard cost $12.00 18.70 31.45 $62.15 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $6.00 per Ib.) $18.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $71.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (3.0 Ibs. @ $6.00 per Ib.) $18.00 Direct labor (1.8 hrs. @ $11.00 per hr.) 19.80 Overhead (1.8 hrs. @ $18.50 per hr.) 33.30 Total standard cost $71.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $6.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $24.00 19.80 33.30 $77.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $6.00 per Ib.) Direct labor (1.8 hrs. @ $11.00 per hr.) Overhead (1.8 hrs. @ $18.50 per hr.) Total standard cost $24.00 19.80 33.30 $77.10 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the...

Antuan Company set the following standard costs for one unit of its product Direct materials (3.0 Ibs. $5.00 per Ib.) Direct labor (1.6 hrs. e $11.00 per hr.) Overhead (1.6 hrs. e $18.50 per hr.) $15.00 17.60 29.60 Total standard cost $62.20 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the 75%...

Antuan Company set the following standard costs for one unit of its product Direct materials (3.0 Ibs. $5.00 per Ib.) Direct labor (1.6 hrs. e $11.00 per hr.) Overhead (1.6 hrs. e $18.50 per hr.) $15.00 17.60 29.60 Total standard cost $62.20 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at the 75%...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.6 hrs. @ $13.00 per hr.) Overhead (1.6 hrs. @ $18.50 per hr.) Total standard cost $20.00 20.80 29.60 $ 70.40 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at...

Antuan Company set the following standard costs for one unit of its product. Direct materials (4.0 Ibs. @ $5.00 per Ib.) Direct labor (1.6 hrs. @ $13.00 per hr.) Overhead (1.6 hrs. @ $18.50 per hr.) Total standard cost $20.00 20.80 29.60 $ 70.40 The predetermined overhead rate ($18.50 per direct labor hour) is based on an expected volume of 75% of the factory's capacity of 20,000 units per month. Following are the company's budgeted overhead costs per month at...

Most questions answered within 3 hours.

-

A coach uses a new technique to train gymnasts. Seven

gymnasts were randomly selected and their...

asked 1 hour ago -

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 3 hours ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 5 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 5 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 7 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 7 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 7 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 7 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 7 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 7 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 7 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 7 hours ago