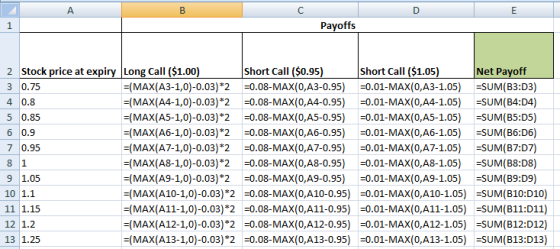

Homework Answers

a]

Payoff of a long call option = Max[S-X, 0] - P

Payoff of a short call option = P - Max[0, S-X]

S = underlying price at expiry,

X = strike price

P = premium paid or received (long options involve paying premium, and short options receive premium)

b]

The position will make maximum profit when the spot price is $0.95 and below or $1.05 and above.

c]

The position will make maximum loss when the spot price is $1.00

d]

An investor taking this position would likely believe the spot rate would stay the same.

Add Answer to:

#1 The following options on American Euro Call options are available. The current spot price of...

Call options on a stock are available with strike prices of $15, $17.5 , and $20...

Call options on a stock are available with strike prices of $15, $17.5 , and $20 and expiration dates in 3 months. Their prices are $4, $2, and $0.5 , respectively. (a) How can those options be used to create a butterfly spread? 2 (b) What is the initial investment? (c) Construct a table showing how payoff and profit varies with ST in 3 month, for the butterfly spread you created. The table should looks like this: Stock Price Payoff...

Suppose that the exchange rate is €1.25 = £1.00.Options (calls and puts) are available on the...

Suppose that the exchange rate is €1.25 = £1.00.Options (calls and puts) are available on the London exchange in units of €10,000 with strike prices of £0.80 = €1.00.Options (calls and puts) are available on the Frankfurt exchange in units of £10,000 with strike prices of €1.25 = £1.00. For a U.K. firm to hedge a €100,000 payable, buy 10 call options on the euro with a strike in pounds sterling and buy 8 put options on the pound with...

6. The following table shows the premiums of European call and put options having the same...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro at a premium of 3.80cents per euro ($0.0380/euro) and with an expiration date three months from now. The option is for euro100 comma 000. Calculate Henrik's profit or loss should he exercise before maturity at a time when the euro is traded spot at strike prices beginning at $1.10/euro, rising to $1.34/euro in increments of $0.04. The profit or loss should Henrik exercise before...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro...

Henrik's Options. Assume Henrik writes a call option on euros with a strike price of $1.2500/euro at a premium of 3.80cents per euro ($0.0380/euro) and with an expiration date three months from now. The option is for euro100 comma 000. Calculate Henrik's profit or loss should he exercise before maturity at a time when the euro is traded spot at strike prices beginning at $1.10/euro, rising to $1.34/euro in increments of $0.04. The profit or loss should Henrik exercise before...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume you buy a call option for £31,250 with a strike price of $1.330/f and a...

Assume you buy a call option for £31,250 with a strike price of $1.330/f and a premium of $.0OSVE Assume you buy a put option for £31,250 with a strike price of S1.310/s and a premium of s.ovE. 1. Turn in a spreadsheet (Use Excel) (50 points) Examine the payoffs from possible ending spot rates of $1.270/E to $1.370/E with increments of $.005. (i.e, 1.270, 1.275, 1.280,.... ..365, 1.370) Build a spreadsheet exactly as we did in class to show...

Assume you buy a call option for £31,250 with a strike price of $1.330/f and a premium of $.0OSVE Assume you buy a put option for £31,250 with a strike price of S1.310/s and a premium of s.ovE. 1. Turn in a spreadsheet (Use Excel) (50 points) Examine the payoffs from possible ending spot rates of $1.270/E to $1.370/E with increments of $.005. (i.e, 1.270, 1.275, 1.280,.... ..365, 1.370) Build a spreadsheet exactly as we did in class to show...

Strike Price Call Price Put Price 95 7.05 1.81 100 4.11 3.86 105 2.14 6.88 2....

Strike Price Call Price Put Price 95 7.05 1.81 100 4.11 3.86 105 2.14 6.88 2. Start with $0 in your account. a) Short XYZ at $100 and use some of the cash to buy a 95 strike call, investing the rest in zero coupon bonds. b) Construct profit and payoff graphs for this position (ignoring stock borrow fees). c) Instead, borrow enough cash to buy the 95 strike put. d) Construct profit and payoff graphs for this position....

XYZ stock is trading at $100. The effective 3 month interest rate r 190.3 month options...

XYZ stock is trading at $100. The effective 3 month interest rate r 190.3 month options on XYZ are trading at the following prices: Strike Price Call Price Put Price 95 100 105 7.05 4.11 2.14 6.88 1.81 3.86 1. Buy XYZ for S100 and buy a 95 strike put a) What is the cost for this position? b) Construct the payoff and profit graphs for this position c) Take the same amount of cash as in a) and instead...

XYZ stock is trading at $100. The effective 3 month interest rate r 190.3 month options on XYZ are trading at the following prices: Strike Price Call Price Put Price 95 100 105 7.05 4.11 2.14 6.88 1.81 3.86 1. Buy XYZ for S100 and buy a 95 strike put a) What is the cost for this position? b) Construct the payoff and profit graphs for this position c) Take the same amount of cash as in a) and instead...

can someone explain to me why this is a call? And why I wouldn’t buy a...

can

someone explain to me why this is a call? And why I wouldn’t buy a

put?

Option exercise Paulo is a currency speculator for Allianz (Germany). His latest speculative position is to profit from his expectations that the US Dollar will fall significantly against the Euro. The current spot rate is USD 1.09663/EUR. He must choose between the following 90-day options on the Euro: OPTION STRIKE PRICE PREMIUM Put USD 1.1250/EUR USD 0.00005/EUR Call USD 1.1250/EUR USD 0.00062/EUR Should...

can

someone explain to me why this is a call? And why I wouldn’t buy a

put?

Option exercise Paulo is a currency speculator for Allianz (Germany). His latest speculative position is to profit from his expectations that the US Dollar will fall significantly against the Euro. The current spot rate is USD 1.09663/EUR. He must choose between the following 90-day options on the Euro: OPTION STRIKE PRICE PREMIUM Put USD 1.1250/EUR USD 0.00005/EUR Call USD 1.1250/EUR USD 0.00062/EUR Should...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume you buy a call option for £31,250 with a strike price of $1.330/f and a premium of $.0OSVE Assume you buy a put option for £31,250 with a strike price of S1.310/s and a premium of s.ovE. 1. Turn in a spreadsheet (Use Excel) (50 points) Examine the payoffs from possible ending spot rates of $1.270/E to $1.370/E with increments of $.005. (i.e, 1.270, 1.275, 1.280,.... ..365, 1.370) Build a spreadsheet exactly as we did in class to show...

Assume you buy a call option for £31,250 with a strike price of $1.330/f and a premium of $.0OSVE Assume you buy a put option for £31,250 with a strike price of S1.310/s and a premium of s.ovE. 1. Turn in a spreadsheet (Use Excel) (50 points) Examine the payoffs from possible ending spot rates of $1.270/E to $1.370/E with increments of $.005. (i.e, 1.270, 1.275, 1.280,.... ..365, 1.370) Build a spreadsheet exactly as we did in class to show...

XYZ stock is trading at $100. The effective 3 month interest rate r 190.3 month options on XYZ are trading at the following prices: Strike Price Call Price Put Price 95 100 105 7.05 4.11 2.14 6.88 1.81 3.86 1. Buy XYZ for S100 and buy a 95 strike put a) What is the cost for this position? b) Construct the payoff and profit graphs for this position c) Take the same amount of cash as in a) and instead...

XYZ stock is trading at $100. The effective 3 month interest rate r 190.3 month options on XYZ are trading at the following prices: Strike Price Call Price Put Price 95 100 105 7.05 4.11 2.14 6.88 1.81 3.86 1. Buy XYZ for S100 and buy a 95 strike put a) What is the cost for this position? b) Construct the payoff and profit graphs for this position c) Take the same amount of cash as in a) and instead...

can

someone explain to me why this is a call? And why I wouldn’t buy a

put?

Option exercise Paulo is a currency speculator for Allianz (Germany). His latest speculative position is to profit from his expectations that the US Dollar will fall significantly against the Euro. The current spot rate is USD 1.09663/EUR. He must choose between the following 90-day options on the Euro: OPTION STRIKE PRICE PREMIUM Put USD 1.1250/EUR USD 0.00005/EUR Call USD 1.1250/EUR USD 0.00062/EUR Should...

can

someone explain to me why this is a call? And why I wouldn’t buy a

put?

Option exercise Paulo is a currency speculator for Allianz (Germany). His latest speculative position is to profit from his expectations that the US Dollar will fall significantly against the Euro. The current spot rate is USD 1.09663/EUR. He must choose between the following 90-day options on the Euro: OPTION STRIKE PRICE PREMIUM Put USD 1.1250/EUR USD 0.00005/EUR Call USD 1.1250/EUR USD 0.00062/EUR Should...

Most questions answered within 3 hours.

-

Assume that in a hydrogen atom, the electron circles the nucleus

in a circle of radius...

asked 33 seconds ago -

Describe two obstacles that makes fixing atmospheric nitrogen

difficult.

asked 5 minutes ago -

T

F 53) Most differences

between human groups are the result of biology rather than

culture....

asked 10 minutes ago -

A 5.20 mW helium neon laser emits a visible laser beam with a

wavelength of 633...

asked 13 minutes ago -

Assignment:

Your

organization has made a strategic decision

to

outsourcework

currently performed in house. You have...

asked 11 minutes ago -

A hospital performs 100 surgeries per week. The probability that

complications after surgery occur is 10%....

asked 12 minutes ago -

In preparing its cash flow statement for the year ended December

31, 2018, Green Co. gathered...

asked 14 minutes ago -

Donna is 18 years old and full time accounting student.She is

saving for an overseas holiday...

asked 14 minutes ago -

Service-oriented architectures (SOA) provide

object-oriented architectures for web platforms that represent a

collection of services. SOA...

asked 15 minutes ago -

Le Terroir Winery is considering an expansion project to produce

fine wines. The trial expansion will...

asked 24 minutes ago -

The Bahraini public budget experiences deficit in the last

seven years, what are procedures are taken...

asked 31 minutes ago -

You invested $30,000 in a mutual fund at the beginning of the

year when the NAV...

asked 35 minutes ago